Download

1 / 8

80 likes | 176 Views

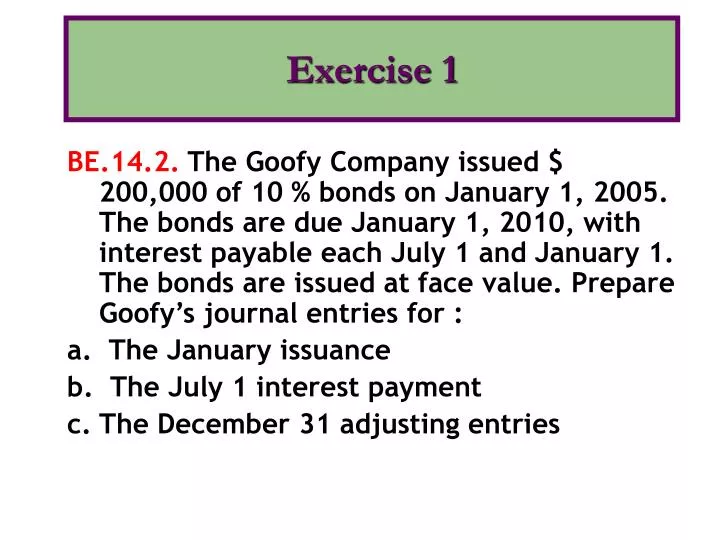

Exercise 1. BE.14.2. The Goofy Company issued $ 200,000 of 10 % bonds on January 1, 2005. The bonds are due January 1, 2010, with interest payable each July 1 and January 1. The bonds are issued at face value. Prepare Goofy’s journal entries for : a. The January issuance

E N D

Exercise 1 BE.14.2. The Goofy Company issued $ 200,000 of 10 % bonds on January 1, 2005. The bonds are due January 1, 2010, with interest payable each July 1 and January 1. The bonds are issued at face value. Prepare Goofy’s journal entries for : a. The January issuance b. The July 1 interest payment • The December 31 adjusting entries

Answer of Exercise 1 (a) Cash 200,000 Bonds Payable 200,000 (b) Interest Expense 10,000 Cash 10,000 ($ 200,000 X 10 % X 6/12 = 10,000) • Interest Expense 10,000 Interest Payable 10,000

Exercise 2, 3 BE.14.3. Assume the bonds in BE.14.2. Were issued at 98. Prepare the journal entries for : • January 1 • July 1 • December 31, assume the Goofy Co records straight line amortization annually on December 31. BE.14.4. Assume the bonds in BE.14.2. Were issued at 103. Prepare the journal entries for : • January 1 • July 1 • December 31, assume the Goofy Co records straight line amortization annually on December 31.

Answer of Exercise 2 (a) Cash 196,000 Discount on Bonds Payable 4,000 Bonds Payable 200,000 (b) Interest Expense 10,000 Cash 10,000 ($ 200,000 X 10 % X 6/12 = 10,000) • Interest Expense 10,000 Interest Payable 10,000 Interest Expense 800 Discount on Bonds Payable 800 ($ 4,000 X 1/5 = $ 800)

Answer of Exercise 3 (a) Cash 206,000 Premium on Bonds Payable 6,000 Bonds Payable 200,000 (b) Interest Expense 10,000 Cash 10,000 ($ 200,000 X 10 % X 6/12 = 10,000) • Interest Expense 10,000 Interest Payable 10,000 Premium on Bonds Payable 1,200 Interest Expense 1,200 ($ 6,000 X 1/5 = $ 1,200)

Exercise 4 P.14.8. On December 31, 2004, Jose Luis Co acquired a computer from Cuevas Co by issuing a $ 400,000 non interest bearing note, payable in full on December 31, 2008. Jose Luis Co’s credit rating permits it to borrow funds from its several lines of credit at 10 %. The computer is expected to have a 5 year life and a $ 50,000 salvage value. Instructions • Prepare the journal entry for the purchase on December 31, 2004. • Prepare any necessary adjusting entries relative to depreciation (use straight line) and amortization (use effective interest method) on December 31, 2005. c. Prepare any necessary adjusting entries relative to depreciation and amortization on December 31, 2006.

Answer of Exercise 4 • December 31, 2004 Computer Equipment (PV 400,000 x 0.68301) 273, 204 Discount on Notes Payable 126,796 Notes Payable 400,000 (b) December 31, 2005 Depreciation Expense 44,640.80 Acc Depr Computer Equipment ((273,204 – 50,000):5) 44,640.80 Interest Expense 27,320.40 Discount on Notes Payable 27,320.40 (c) December 31, 2006 Depreciation Expense 44,640.80 Acc Depr Computer Equipment 44,640.80 Interest Expense 30,052.44 Discount on Notes Payable 30,052.44

Answer of Exercise 4 (b) December 31, 2005 Schedule of Note Discount Amortization