Download

1 / 109

1.1k likes | 1.31k Views

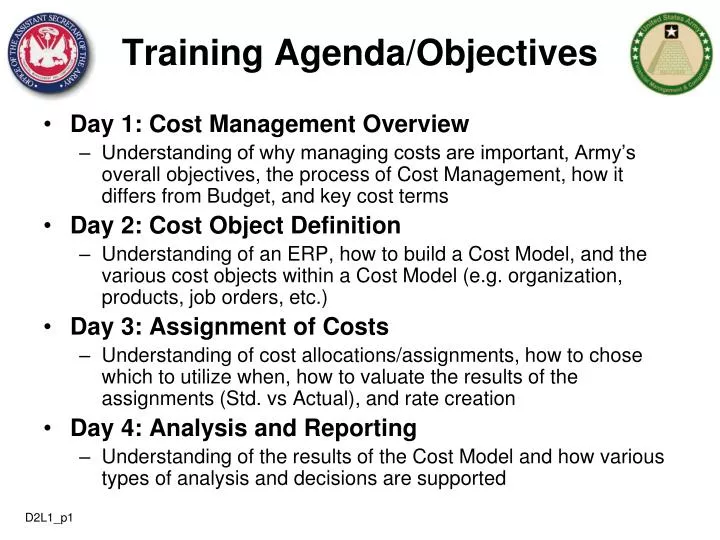

Day 1: Cost Management Overview Understanding of why managing costs are important, Army’s overall objectives, the process of Cost Management, how it differs from Budget, and key cost terms Day 2: Cost Object Definition

E N D

Day 1: Cost Management Overview Understanding of why managing costs are important, Army’s overall objectives, the process of Cost Management, how it differs from Budget, and key cost terms Day 2: Cost Object Definition Understanding of an ERP, how to build a Cost Model, and the various cost objects within a Cost Model (e.g. organization, products, job orders, etc.) Day 3: Assignment of Costs Understanding of cost allocations/assignments, how to chose which to utilize when, how to valuate the results of the assignments (Std. vs Actual), and rate creation Day 4: Analysis and Reporting Understanding of the results of the Cost Model and how various types of analysis and decisions are supported Training Agenda/Objectives D2L1_p1

Day 2: Cost Object Definition Understanding of an ERP, how to create a cost model and each of the cost objects supported within the cost model Day 2 Objective & Agenda • Lesson 1: ERP Enabler • Lesson 2: Costing Conceptual Design • Lesson 3: Cost Centers • Lesson 4: Activity Types • Lesson 5:Cost Elements • Lesson 6: WBS Elements • Lesson 7: Orders • Lesson 8: Business Processes • Lesson 9: Statistical Key Figures • Lesson 10:Capturing Costs D2L1_p2

THE $10,000 WOULD COME OUT OF MY BUDGET BUT THE SAVING WOULD GO INTO SOMEONE ELSE’S BUDGET. IT’S NOT THE CHIEF OF STAFF MIGHT NOT AGREE. I FOUND A WAY TO SAVE A MILLION DOLLARS BY SPENDING ONLY $10,000. THAT’S WHY HE IS NOT INVITED TO THE MEETINGS. FEASIBLE. (Modified) D2L1_p3

Objective(s): To understand what “ERP” stands for and how it can support the Army’s Cost Management culture Lesson 1: ERP Enabler D2L1_p4

Enhanced Ability to Capture Cost Organizational Real Property / Special Event or Cost Objects Program / Project Task / Activity Entities Equipment Initiative GFEBS (SAP) Assets / Real Cost Centers Project / WBS Business Process Internal Order Estate Objects Cost Collectors • BRAC • Installation • Acquisition • Service Support • Building • Training Event • Brigade • RDTE Project Program (SSP) • Training Range • Mandatory Army Examples • School • MILCON Project • Instructional Course • Weapon System Training • Directorate • System Test • Repair Process • Support to • Lab • Test Run Olympics Cost assigned Directly or Indirectly • Customer / Product • Brigade • Tenant • Command • Weapon System • PEO / PM • Course D2L1_p5

Many ways to Measure CostMethodology vs System • Army’s Purpose is to Provide Operational Managers with Relevant “True” Cost Information to Make Sound Economic Decisions • Methodologies to Measure Cost (FASAB #4) • Activity Based Costing • Job Order (Event) costing • Project (with WBS) costing • Std. (Product) costing • Others • Requires a System to Gather Cost Data and Provide Analytical Information Army Ad Hoc Financial Reports Independent Cost Models Integrated Cost Management D2L1_p6

Enterprise Resource Planning (ERP) ERP Benefits • ERPs Help to Streamline & Integrate the Processes & Systems Providing the Following Benefits: • Increases Productivity Across Organizations • Improves Standardization & Efficiency of Processes • Increases Access, Consistency & Transparency of Data • Provides Collaboration Across Business Domains • Provides IT Economies of Scale • Enhances Analytics & Improves Accuracy of Data D2L1_p7

GFEBS Enterprise Resource Planning (ERP) Commercial Off the Self System that Integrates All Facets of the Business End User Presentation Layer Data Warehousing Analytics D2L1_p8

Cost Management Integrated with Finance & Budget Accounting End User Presentation Layer Public Sector Budget Accounting Enterprise Resource Planning (ERP) • ERP Functionality Integrates Management Accounting (Cost Management) with the Financial & Budget Accounting End User Presentation Layer Data Warehousing Analytics D2L1_p9

Cost Management Integrated with Finance & Budget Accounting Public Sector Budget Accounting Enterprise Resource Planning (ERP) ERPs (e.g. GFEBS) Enable The Cost Management Process Cost Accounting Cost Planning Cost Analysis Cost Management Process Cost Controlling End User Presentation Layer D2L1_p10

ECC – Enterprise Central Component BI – Business Intelligence FI – Financial Acct. & Mgmt. Cost By Report FM – Funds Acct. & Mgmt. Unit Cost Report CO – Cost Acct. & Mgmt. MM – Materials Mgmt. and Procurement Detailed Labor Report PPE – Property, Plant & Equipment [PM, PS, RE, AA] SD – Sales & Reimbursables • Optimized for Data Input • Transaction Processing • Real-time; recon analysis • Structured reporting • Optimized for Data Extraction • Analytical Processing • Near real-time; trending analysis • Slice-n-dice reporting (pivot) GFEBS System Components D2L1_p11

FI - None • FM - Commitment • CO - None • FI - None • FM - Obligation • CO - None PR PO Pay GR • FI - AP/Cash • FM - Disbursement • CO - None • FI - Expense/AP • FM - Expenditure • CO - Expense Simultaneous Update ECC – Enterprise Central Component FI – Financial Acct. & Mgmt. FM – Funds Acct. & Mgmt. CO – Cost Acct. & Mgmt. MM – Materials Mgmt. and Procurement PPE – Property, Plant & Equipment [PM, PS, RE, AA] SD – Sales & Reimbursables • Optimized for Data Input • Transaction Processing • Real-time; recon analysis • Structured reporting D2L1_p12

An ERP is an enabler to Cost Management “Culture” by providing the technology necessary The Army Cost Model is being designed into GFEBS which utilizes the SAP ERP application The ERP application has a transactional component and an analytical component The transactional component has real-time integration for the various value streams/modules Lesson 1: Wrap-Up D2L1_p13

Objective(s): To understand the approach to developing the costing conceptual design to support the Cost Management Process using the GFEBS ERP application. Lesson 2: Costing Conceptual Design D2L2_p1

Full Cost Organizations Full Cost Product/Services Full Cost Customers Director of Logistics) SSPA: Manage OCIE Inventory Brigade XXX Cost Accounting SSPB:Issue OCIE to Soldier Military Labor Central Issue facility What/Why information is entered, stored, used, and presented TRADOC YYY SSPC:Issue Clothing to Initial Training Soldier Depreciation SSPD:Accept OCI Turn-Ins Civilian Employees Brigade ZZZ Contractors SSPE:Receive & Process Shipments Military Labor Cost Planning Cost Analysis Cost Management Process SSPF:Manage Chemical Defense Equipment . . Etc. MILHR CNTHR CIVHR Cost Controlling How the information is entered, stored, used, and presented End User Presentation Layer Where the information is entered, stored, used, and presented Public Sector Budget Accounting Costing Conceptual Design D2L2_p2

The translation of the business objectives, needs, and requirements into a management decision support model (Cost Model) A monetary valuation of the economic goods and services of the organization – full burden cost flows “The Continuum” – maturation over years (ex. from Ft. Jackson go-live through all roll-outs and beyond, increased accuracy of cost flows through better data) What is the Costing Conceptual Design? The CCD influences/defines the set-up of tools providing cost management information, e.g. GFEBS, GCSS, Data Warehouses, etc. D2L2_p3

Management information requirements – What type of decisions to support, when, for who, etc. (e.g. Insource/Outsource, Contract/OT, etc.) Cost objectives necessary to support the informational needs (SSP Focused, Brigade, etc.) The Cost Objects – What does it cost to/for/if….? Cost Object Relationships – flows of goods and services from/to/between Various Techniques for reflecting the relationships - % based, quantity (Plan/Actual, such as ATAAPS Hrs), variances, etc. What Influences the CCD Developed? D2L2_p4

Full Cost Customers Full Cost Product/Services Cost Center SSPs Provided Brigade XXX SSPA: Manage OCIE Inventory MIL HR CNT HR CIV HR SSPB:Issue OCIE to Soldier TRADOC YYY SSPC:Issue Clothing to Initial Training Soldier SSPD:Accept OCI Turn-Ins Brigade ZZZ SSPE:Receive & Process Shipments . . Etc. SSPF:Manage Chemical Defense Equipment CCD – Cost Model Full Cost Organizations Director of Logistics) The translation of the business objectives, needs, and requirements into a management decision support model (Cost Model) Cost Center/Resource Pool Military Labor Central Issue facility Depreciation Civilian Employees Contractors Military D2L2_p5

Full Cost Customers Full Cost Product/Services Cost Center SSPs Provided Brigade XXX SSPA: Manage OCIE Inventory MIL HR CNT HR CIV HR SSPB:Issue OCIE to Soldier TRADOC YYY SSPC:Issue Clothing to Initial Training Soldier SSPD:Accept OCI Turn-Ins Brigade ZZZ SSPE:Receive & Process Shipments . . Etc. SSPF:Manage Chemical Defense Equipment maturation over years CCD – Cost Model Full Cost Organizations Director of Logistics) A monetary valuation of the economic goods and services of the organization – full burden cost flows Cost Center/Resource Pool Military Labor Central Issue facility Depreciation Civilian Employees Contractors Military D2L2_p6

Army Cost Model Concept Cost Center Asset / Equipment Project / Program Internal Order WBS / Work Order Organization - Labor, Materials, Supplies Resources Plant, Property & Equipment Building Project, Weapon System Outputs Services, Events (SSP, Course) Job (Set of Tasks) – Maint & Repair D2L2_p7

Resource Centric Cost Centers [Orgs] Resource Pools/Activity Types [Types of Labor, Machine, SQFT] Cost Elements [Labor, Travel, Etc. Business Process [Services] Cost Object Types • Product/Service Centric • Projects/Events (ex. Minor Construction…) • Orders (ex. Work, Maintenance, Service, Production, Customers….) • Results Centric • Results Segments (Customers of your products/services) P&L PROJ PROD CC (ex. Dir/Div…) SERV RP IO CE BPR D2L2_p8

Identification of Subject Matter Experts from each of the core business providers Schedule meetings with each area’s key stakeholder(s) and SME representatives Conduct Analysis workshops Gather Results and Evaluate Translate the business objectives, needs, and requirements into a management decision support model, i.e. the CCD Feed information to system supporting management model (e.g. GFEBS) How is the CCD Developed? D2L2_p8

Review of IMCOM stated objectives on web site and already identified products/services (CLS) IMCOM HQ Interviews of CLS representatives Select and visit bases and conduct analysis workshops [Ft. Jackson, Ft. Lewis, Ft. Polk, Aberdeen Proving Grounds] Gather and review org charts, TDA, etc. Work with Installation RM representative to collect information required Recognize all installations are different How is the CCD Developed for IMCOM? D2L2_p9

Inputs into the Analysis Organizational Structure List of Locations List of Data Feeds and Input List of Operational Systems Current Cost Reports Analysis Outputs Organization Revamp Org Structure Conceptual Design Process Organizational Business Process Management Accounting Processes Technology Interface Inventory Reports and Forms Customizations Analysis Workshops D2L2_p10

Full Cost Customers Full Cost Product/Services Cost Center SSPs Provided Brigade XXX SSPA: Manage OCIE Inventory MIL HR CNT HR CIV HR SSPB:Issue OCIE to Soldier TRADOC YYY SSPC:Issue Clothing to Initial Training Soldier SSPD:Accept OCI Turn-Ins Brigade ZZZ SSPE:Receive & Process Shipments . . Etc. SSPF:Manage Chemical Defense Equipment CCD – Cost Model Full Cost Organizations Director of Logistics) Cost Center/Resource Pool Military Labor Central Issue facility Depreciation Civilian Employees Results of the Analysis Workshops are aggregated and utilized to generate the Cost Model Contractors Military D2L2_p11

GFEBs is the technology to support Cost Management and where the information is captured, stored, used, and displayed. The Cost Management Process defines how Cost Management is supported. The CCD (Cost Model) is what cost Management information will be provided to support management decisions The CCD is the translation of management objectives, with the valuation of the goods and services, and matures in scope and accuracy over time. The output of the CCD and Analysis Workshop findings is a Cost Model to be built into GFEBS Lesson 2: Wrap-Up D2L2_p12

What are some of the benefits of an ERP? Question # 1 • ERPs Help to Streamline & Integrate the Processes & Systems Providing the Following Benefits: • Increases Productivity Across Organizations • Improves Standardization & Efficiency of Processes • Increases Access, Consistency & Transparency of Data • Provides Collaboration Across Business Domains • Provides IT Economies of Scale • Enhances Analytics & Improves Accuracy of Data D2L2_p13

Full Cost Product/Services Full Cost Organizations Full Cost Customers Director of Logistics) SSPA: Manage OCIE Inventory Brigade XXX Cost Accounting SSPB:Issue OCIE to Soldier Military Labor Central Issue facility What/Why information is entered, stored, used, and presented TRADOC YYY SSPC:Issue Clothing to Initial Training Soldier Depreciation SSPD:Accept OCI Turn-Ins Civilian Employees Brigade ZZZ Contractors SSPE:Receive & Process Shipments Military Labor Cost Planning Cost Analysis SSPF:Manage Chemical Defense Equipment Cost Management Process . . Etc. MILHR CIVHR CNTHR Cost Controlling How the information is entered, stored, used, and presented End User Presentation Layer Where the information is entered, stored, used, and presented Public Sector Budget Accounting Question #2: What are the three Components of a Costing Conceptual Design D2L2_p14

Objective(s): To understand what the Cost Center cost object represents, key definition criteria (guiding principles), uses, and how defined for the Cost Model Lesson 3: Cost Centers D2L3_p1

Fund Center = ASN Performs Funds Management Cost Centers Cost Center Groups Costing Starts with Cost Centers Special Staff Cmdr. Ofs. Ch, MWR Ch, DOL Ch, DPW Ch, RM D2L3_p2

SAFM-CE Army Cost Model Cost Center Definition • This definition lends itself to multiple varied utilizations of the cost center object to reflect the costs of an organization • Further criteria/principles along with the Cost Center’s purpose must be utilized to better indicate when a Cost Center is appropriate • The purpose of the Cost Center object is to serve as the base for the management optimization model – the model utilized to reflect the business, it’s inputs, conversions, and outputs in order to support management decisions • The Cost Center is the first cost object to be defined for the Cost Model • To support the appropriate definition of a Cost Center within an entity, Guiding Principles should be considered D2L3_p3

SAFM-CE Army Cost Model Guiding Principles for Cost Centers D2L3_p4

People Related: e.g. RMO office Facilities Related: e.g. Warehouses, Hospitals, Office Space Equipment Related: e.g. Citrix farm accessing GFEBS, Cranes/Trucks Blended: e.g. mix of resources within a organization, e.g. Vehicles and Mechanics Motor Pool SAFM-CE Army Cost Model Cost Centers Uses RMO Building 1 Hospital 1 Network Admin Equipment D2L3_p5

SGO used as start for defining Cost Centers per Installation Review of TDA and interviews at each base reveal branches and sections that are also added to the list of Cost Centers Tenant organizations and RPAs (e.g. buildings) are also defined as Cost Centers to develop the final Cost Center list to be loaded to GFEBS Building 1….N from ASCIPS Cost Center Creation D2L3_p6

Cost Center Information D2L3_p7

SAFM-CE Army Cost Model Cost Center Hierarchy • In addition to defining the Cost Centers and the attribute information for each individual Cost Center, the Cost Centers need to be identified on a standard hierarchy • There is a single standard hierarchy which every Cost Center will reside on to ensure that all costs can be reported from a single hierarchy • Alternative hierarchies can be defined as needed to meet management objectives D2L3_p8

Start with SGO structure Expand to accommodate lower levels identified specific to the installation Cost Center Hierarchy Creation D2L3_p9

Complete lower level hierarchy and generate into GFEBS load sheet Cost Center Hierarchy D2L3_p10

Cost Center Hierarchy D2L3_p11

Cost Center Hierarchy D2L3_p12

A cost center is a responsibility center that incurs costs and has a manager who is accountable for those costs Costs of the cost center are material in nature (worth capturing vs the cost of capturing) A cost center has a long life span of more than 1 year (typically years) and has a manager responsible for the resources consumed and the outputs produced by the cost center Every cost center resides on the standard cost center hierarchy Alternative cost center hierarchies can exist as well Lesson 3: Wrap-Up D2L3_p13

A cost center is a cost object used to capture any costs? True False Questions: X • A cost center is utilized to capture the revenues generated by the outputs of an organization • True • False X D2L3_p14

A cost center can be assigned to more than 1 standard hierarchy? True False Questions: X • There is a cost center for every fund center (ASN) • True • False X D2L3_p15

Objective(s): To understand what the Activity Type cost object represents, key definition criteria (guiding principles), uses, and how defined for the Cost Model Lesson 4: Activity Types D2L4_p1

SAFM-CE Army Cost Model Activity Type Definition • The term activity type is often confused with an activity, of the Activity-Based Costing approach – however it does not represent an activity. Activities are generally identified with a verb, e.g. Pick Items, Pack Box, Ship Pallet • A more appropriate translation is Resource Pool, e.g. groups of like kind resources within an organization that perform an activity such as TECH HR, SUPV HR, MACHR • Activity Types have a rate/output associated are the utilization of capacity to perform “work” to generate a product/service, e.g. TECH HR @ $10/Hr D2L4_p2

People e.g. RMO Manager & Analyst MECH HR ANLY HR VEHC HR MGR HR SAFM-CE Army Cost Model Activity Type Uses Cost Center Activity Type RMO Motor Pool • Blended e.g. Motor Pool • Mechanic & Vehicle D2L4_p3

SAFM-CE Army Cost Model Guiding Principles for Activity Types D2L4_p4

Capture Capacity or Planned Output, e.g. grandma works 2088 Hrs or machine runs 3500 Hrs (10 Hrs/Day for 350 days) Holds the rate for the output of the resource pool, e.g. $2 Hr, $5 Hr, $20 Hr Assigns capacity consumed by products/ services, e.g. Hrs/min worked per dress, which then valuates based on the rate SAFM-CE Army Cost Model Activity Type Uses $20/Dress • Interchangeable • Not Similar Technology • Not Homogenous – needs resources (input cost structure) of food versus laborer versus electricity D2L4_p5

Activity Types facilitate capacity management and there are various types of capacity (e.g. Productive, Non-Productive, Idle/Excess, etc.) Activity Types provide the capacity information required to optimize the conversion of inputs to generate the most outputs – meeting the “Efficiently” portion of the Cost Management definition Activity Types are defined as master data, however they exist only in conjunction with a Cost Center Activity Type = MACHR is assigned to Cost Center 1 and Cost Center 2 resulting in CC1/MACHR and CC2/MACHR each of which holds their own rate, their planned output, captures actuals, etc. Capacity Management D2L4_p6

SAFM-CE Army Cost Model How Activity Types are Defined • The project and production related areas are familiar with the concepts of labor and equipment rates and often have std. rates for charging level of effort for like kind resources to work on an order, e.g. IFS • IFS shop rates are reviewed and then grouped/expanded upon into like kind resources • Equipment Activity Types are defined based on a review and grouping of equipment, e.g. Dump Truck 6T • Vehicle Activity Types are defined based on GSA classification into groupings D2L4_p7