Download

1 / 35

350 likes | 520 Views

Overview of Petroleum & Natural Gas Sector & Regulatory Perspective in India. Top Primary Energy Consuming Countries 2005. Total World Energy Consumption: 10537 mtoe. 5 th largest energy consumer (Share 3.7% of global energy) Per capita energy consumption - about one third of world average

E N D

Overview of Petroleum & Natural Gas Sector & Regulatory Perspective in India

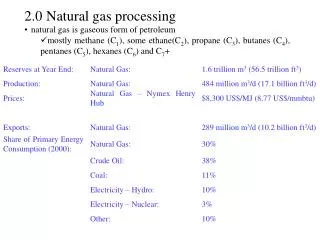

Top Primary Energy Consuming Countries 2005 Total World Energy Consumption: 10537 mtoe • 5th largest energy consumer (Share 3.7% of global energy) • Per capita energy consumption - about one third of world average • Energy consumption projection(2031-32) • to grow at 5 % CAGR (8% GDP growth) as per Integrated Energy Policy • 3.4% CAGR upto 2025 (GDP: 5%) • Energy import dependence is 30% (26% on account of oil & 4% for Coal + Power) and is likely to climb to 40-45% by 2025 • Oil import dependence is around 72% currently. Likely to go upto 90% level Fig. in MTOE Per-capita Energy Consumption Source – Energy Information Administration (EIA)

Primary Commercial Energy Mix World World 2003 2030 10517 mtoe 18040 mtoe CAGR: 2% • Oil & Gas continue to play major role India India 2003-04 2031-32 327 mtoe 1651 mtoe CAGR: 6.2% Coal & Oil continue to play major role; Gas is emerging Source – World: EIA-2006; India: IEP 2006

POL - Imports & Exports Crude Oil Import US$ Billion • Gross crude and petroleum products • Crude/product Imports : ~ 28% of total imports • Product Exports : ~ 8% of total exports Product Export Product Import India - A Net Exporter of Products

Refineries & Product Pipelines Refining Refining Capacity: 178 MMT Product Pipelines Product Pipelines Length: 12017 KM Capacity: 68.17 MMT Capacity Utilisation: 77%

Refineries in India(1.4.08) Bhatinda (9.0) Existing Ongoing/Planned Panipat (6.0), (9.0) Digboi (0.7) Bongaigaon (2.4) Mathura (8.0) Numaligarh (3.0) Guwahati (1.0) Barauni (6.0) BINA (6.0) Baroda (13.7) Haldia (6.0), (1.5) Jamnagar (33.0, 29.0,10.5 Paradip (15.0) Mumbai (5.5) (2.4) Visakh (7.5, 7.5) (12) Nos MMTPA IndianOil 10 60.2 BPC 3 22.5 HPC 2 13.0 ONGC / MRPL 2 9.8 Reliance (Pvt.) 2 62.0 Essar(Pvt.) 1 10.5 Total 20 178.0 Tatipaka (0.1, 0.1) Mangalore (9.7, 5.3) Chennai (9.5, 1.7) Cochin (7.5, 2.0) Narimanam (1.0) Expected Refining Capacity by 2011-12: 200-235 MMTPA

India’s product demand & refining capacity Gap between Refining Capacity & Demand 142 68 21 Surplus refining capacity is expected to increase further by 2030 Source: XI Plan Demand India will continue to be product surplus Import/Export requirement for crude/products to be quite substantial

Petroleum Products Pipelines in India Jalandhar Ambala Bhatinda Roorkee Sangrur Najibabad Panipat Meerut Tinsukia Nahorkatiya Delhi Rewari Loni Shahjahanpur Sanganer Mathura Bongaigaon Siliguri Digboi Ajmer Jodhpur Tundla Numaligarh Chaksu Lucknow Kanpur Guwahati Jagdishpur Kot Chittaurgarh Barauni Sidhpur Ahmedabad Rajbandh Kandla Ratlam Navagam BudgeBudge Mundra Jamnagar Maurigram Koyali Indore Vadinar Ankleshwar Dahej Haldia Hazira Manmad Mumbai High Paradip Mumbai Vizag Pune Existing Secunderabad Uran Product Crude Oil Pakni Hazarwadi Vijayawada Products 9893 KM; 64 MMTPA LPG 2124 KM; 4.5 MMTPA Capacity Utilization Prods. - 78%; LPG - 62% Mangalore Bangalore On-going Chennai Product Crude Oil Sankari Asanur Karur Existing Coimbatore Trichy Kochi LPG Madurai

Distribution & Marketing Infrastructure Marketing Infrastructure

Gas Pipelines in India • Length- ~ 11000 kms • Gas Consumption- 39 bcm • LNG Import - 8-9 MMT, 1 mmtpa spot) • Players- GAIL, GSPCL, • GGCL, RGTIL • Pipeline length is likely to double in next 4-5 years Total infrastructure inadequate to meet the country’s requirements

Government of India Policies • Administered Pricing Mechanism (APM) dismantling effective 1.4.2002 • Gas Pricing • NELP • Policy on Refining • Auto Fuel Policy • Policy on Marketing of Petroleum Products • Gas Pipeline Policy • Petroleum Product Pipeline Policy • FDI Policy

Key Decisions Taken on APM dismantling APM Dismantling – Key decisions • Crude oil producers/Refineries to be paid on import parity basis from Apr’02 • Market determined prices for all products except LPG & Kerosene from Apr’02 • Subsidies for LPG/Kerosene from fiscal budget on flat rate basis since Apr’02. Free float thereafter

Key Decisions Taken on APM dismantling Gas Pricing – July 2005 Govt. order • Consumer price of APM gas increased from Rs. 2,050/mscm to Rs. 3,200/mscm linked to calorific value of 10,000 kcal/scm pending Tariff Comm. recommendations • All APM gas to be supplied to only power & fertiliser sector consumers against existing allocation as well as for specific end consumers under court orders/small consumers having allocation upto 0.05 mmscmd • Rest of consumers to be supplied at market related price • APM gas price for other than power & fertiliser sectors further increased from Rs 3,200/mscm to Rs 3,840/mscm wef June 2006 • As against APM gas price of around $ 1.8/mmbtu, free market gas price varies e.g., RLNG @ $ 3.86/mmbtu, PMT gas @ $ 4.75/mmbtu, spot LNG purchases @ $ 7-8/mmbtu, etc.

New Exploration & Licensing Policy (NELP) • NELP introduced in 1999; so far VIII rounds held • Internationally competitive fiscal regime • Transparent Process, International competitive bidding • Contractual Fiscal Stability • Excellent Tax Incentives • Special deepwater concessions • Freedom to market production domestically

Policy on Refining • Administered Pricing Mechanism (APM) dismantled for refineries in April 1998 • Setting up of refineries de-licensed in June 1998 • Refineries may be set up subject to meeting statutory requirements • Private refineries by RIL and Essar set up in India • Others JV refineries are under implementation

Auto Fuel Policy - Road map for Fuel Quality improvement in India Sulphur content in ppm (max) FuelBS-IIBS-III/Euro-IIIBS-IV/Euro-IV Petrol 500 150 50 Diesel 500 350 50 Source: Auto Fuel Policy, GoI

Policy on Marketing of Petroleum Products • Marketing of petroleum products except subsidized products allowed to private companies • Marketing of Transportation Fuels authorised: • Subject to entities making investment or proposing to invest Rs. 20 billion in exploration / refining / pipelines / terminals /infrastructure etc.

Exploration Up to 100% FDI: Automatic route through Competitive bidding Refining Up to 100% FDI Up to 49% FDI: if project taken up along with Public Sector Undertakings Marketing Up to 100% FDI permitted in petroleum products marketing Petroleum Pipelines Up to 100% FDI: Under automatic route Natural Gas Pipelines Up to 100% FDI: Under automatic route FDI Policy

PNGRB Act, 2006 • Enacted by Parliament in March’06 • All provisions (except Section 16) of the Act notified w.e.f. 1.10.2007 • PNGRB formally established w.e.f. 1.10.2007 • One Chairperson and four full time Members • Basic Objectives – • To protect the interest of consumers and entities • To ensure uninterrupted and adequate supply in all parts of the country • To provide level playing field • To promote competitive markets

Bidding Criteria - (weightage) - Least PV of overall unit network tariff over economic life of project - (40%) - Least PV of compression charge for CNG over economic life of project - (10%) - Highest PV of “inch-kilometer” of steel pipeline during exclusivity period - (20%) - Highest PV of PNG domestic connections during exclusivity period - (30%)

Exclusivity Criteria for CGD Networks • Two periods of exclusivity provided to promote flow of investments – • Exclusivity of infrastructure over its economic life of 25 years • Marketing exclusivity of 5 years after which 3rd party access to the network for marketing of natural gas would be available on payment of network tariff • Network Tariff to be generally decided on bid basis

Bidding Criteria - (weightage) - LeastPV of unit tariff for 1st tariff zone over economic life of project - (40% & 70% for pipelines < 300 KM) - Least percentage increase for determining incremental tariff for 2nd tariff zone - (20%; nil for pipelines < 300 KM & 30% for pipelines > 300 KM < 600 KM) - Least percentage increase for determining incremental tariff for 3rd and subsequent tariff zones - (10% & nil for pipelines < 600 KM) - Highest PV of natural gas volumes - (30%)

Process for Grant of Authorization 15 days 15 days 30 days 60 days (extendable by 30 days) 30 days 90 days 30 days

City Gas and CNG Present Scenario Total Number of CNG vehicles - 7 lakh Number of entities - 19 Number of GAs - 25 Future Scenario (next three years) Total Number of GAs - 86 Expected CNG vehicles - 25 lakh Future Scenario (next five years) Number of GAs - 125 Expected CNG vehicles - 33 lakh Future Scenario (next ten years) Number of GAs - 250 Expected CNG vehicles - 58 lakh

PNGRB - Major Tasks on Hand Notification of Regulations Declaring/Authorizing petroleum products & natural gas pipelines and city gas distribution networks on common carrier basis Specifying market service and retail service obligations to protect consumers’ interests Fostering Fair Trade and Competition Laying down Standards and Safety Norms