Download

1 / 29

290 likes | 294 Views

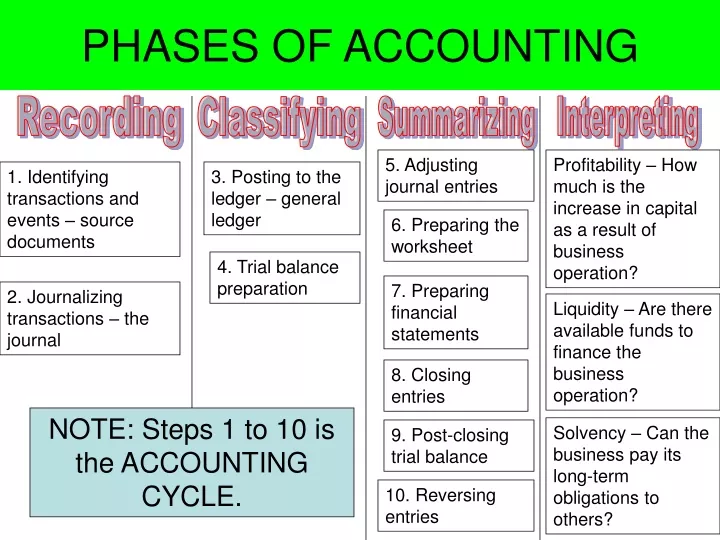

PHASES OF ACCOUNTING. Recording. Classifying. Summarizing. Interpreting. 5. Adjusting journal entries. Profitability – How much is the increase in capital as a result of business operation?. 1. Identifying transactions and events – source documents.

E N D

PHASES OF ACCOUNTING Recording Classifying Summarizing Interpreting 5. Adjusting journal entries Profitability – How much is the increase in capital as a result of business operation? 1. Identifying transactions and events – source documents 3. Posting to the ledger – general ledger 6. Preparing the worksheet 4. Trial balance preparation 7. Preparing financial statements 2. Journalizing transactions – the journal Liquidity – Are there available funds to finance the business operation? 8. Closing entries NOTE: Steps 1 to 10 is the ACCOUNTING CYCLE. Solvency – Can the business pay its long-term obligations to others? 9. Post-closing trial balance 10. Reversing entries

Adjusting Entries – 5th Step What are adjusting entries? When are adjusting entries made? Adjusting entries are journal entries which are to be recorded in the general journal and are usually prepared at the end of the accounting period of one year following the preparation of a trial balance. Adjusting entries are usually prepared at the end of the accounting period of one year following the preparation of a trial balance. What are the effects of adjusting entries? Each adjusting entry affects a balance sheet account (an asset or a liability account) and an income statement account (income or expense account).

Adjusting Entries – 5th Step What are the purposes of the adjusting entries? • Generally, adjusting entries are prepared for the following reasons: • To bring records or balances of accounts updated (or to bring the assets, liabilities, revenues & expenses up-to-date at the end of the accounting period) • To properly match revenues against expense during the period (Revenues to be recognized within the period they are earned and Expenses to be recognized within the period they are incurred.) Specifically, Accounting utilizes “adjusting entries” at the end of an accounting period to split mixed accounts. Mixed accounts are accounts that have components of asset and expense, or liability and income at the end of the accounting period.

Basic Adjusting Entries Items which usually require adjusting journal entries: • Accruals – Accrued Expense & Accrued Income • Deferrals – Prepayment of expense & Precollection of income • Depreciation • Estimated uncollectible accounts or estimated doubtful accounts (bad debts) • Correction of erroneous journal entries

Adjustments for Accruals What is the meaning of ACCRUAL? Accrual means to recognize revenue earned regardless of when it was collected, and to record expenses incurred whether paid or not. This accounting practice is based on the basic principles of ACCRUAL ACCOUNTING. • Accrued Revenue or Accrued Income • Accrued Expenses – Salaries, interest, utilities (electricity, telecommunications and water) and taxes are examples of expenses that are incurred before payment is made. What are the two kinds of accruals?

Adjustments for Accruals What is the meaning of accrued income or acrrued revenue? Accrual Income is an income already earned by the business but not yet collected when the accounting period ends. Accrual Income means bringing into existence an income that is already earned but not yet received. What are the examples of accrued income or accrued revenue? Examples of accrued revenues are: 1. Services performed but not yet billed or collected 2. Accumulating income due to passage of time, as in the case of rent income and interest income

Adjustments for Accruals What is the adjusting entry of Accrued Income or Accrued Revenue? The purpose of the adjusting entry is to record the income earned and recognize the corresponding asset (collectible or receivables) account. The adjusting entries for Accrued Income or Accrued Revenue: Accrued ____________ Income xxx ___________ Income xxx To record income earned but not yet collected. To illustrate: The business received a P100,000 6%, 60 day note from a customer dated Dec. 2, 2008.

Adjustments for Accruals What are the other account names used for accrued income or accrued revenue? Accrued income is reported as a current asset such as accrued receivables, accrued revenues, or part of accounts receivable. The accounts Accrued Rent Income, Accrued Interest Income, etc. are similar to Rent Receivable, Interest Receivable, etc. The term “accrued” when associated with income account connotes “receivables” which means an asset.

Adjustments for Accruals What is the meaning of Accrued Expense? Accrued expense is an expense that is already incurred by the business but not yet paid when the accounting period ends. Accrued expense means recognizing an incurred and unrecorded expense that remains unpaid because payment is not yet due. What are the examples of accrued expense? Examples of Accrued Expense: Accrued Rent Expense, Accrued Salaries Expense, Accrued Interest Expense

Adjustments for Accruals What is the adjusting entry of Accrued expense? The purpose of the adjusting entry is to record the expense and recognize the corresponding liability. The adjusting entry for Accrued Expense: ____________ Expense xxx Accrued ________Expense xxx To record unpaid expense. To illustrate: The business is renting a space of the building for P5000 per month payable every 1st day of the following month. The rental for the month of December 2008 was not paid when the accounting period ended on Dec. 31, 2008. the business intends to pay the rental on Jan. 1, 2009.

Adjustments for Accruals What are the other account names used for accrued expense? The accounts Accrued Rent Expense, Accrued Salaries Expense, Accrued Interest Expense, etc. are similar to Rent Payable, Salaries Payable, Interest Payable, etc. The term “accrued” when associated with an expense account connotes “payable” which means a liability.

Adjustments for Deferrals Deferral is the postponement of the recognition of “an expense already paid but not yet incurred,” or of “a revenue already collected but not yet earned”. • Prepayment of expenses • Precollection of income Prepayments are advanced payments of business expenses or supplies to be used in a business operation. Precollections (also known as Deferred Revenues or Unearned Revenues) are advanced collections of business revenues from customers.

Adjustments for Deferrals Prepayments of Expenses • These items may be recorded initially as prepaid assets or prepaid expenses, which expire either: • The passage of time (e.g. insurance and rent) or • Through use or consumption (e.g. supplies). • Prepaid expense is an expense that is already paid but not yet incurred. • Expense method – an expense is debited upon payment of the prepaid expense. This method is called nominal approach. • Asset method – an asset account is debited upon payment of the prepaid expense. This method is called real approach.

Adjustments for Deferrals Prepayments of Expenses There are 2 methods or approaches that can be used in recording prepayments, namely: Expense Method an expense is debited upon payment of the prepaid expense. This method is called nominal approach. Asset Method an asset account is debited upon payment of the prepaid expense. This method is called real approach.

Adjustments for Deferrals Prepayments of Expenses To illustrate: On Sept. 1, 2009, the business paid an insurance premium covering the period from Sept. 1, 2009 to Sept. 1, 2010 in the amount of P3,600. The accounting period ends on Dec. 31, 2009.

Adjustments for Deferrals Precollections of Income • Income method an Income account is credited upon collection or receipt of cash. This method is also called “nominal approach” because an income is a nominal account. • Liability method a liability account is credited upon collection or receipt of cash. This method is also called “real approach” because a liability is a real account. Precollected income is an income that is already collected but not yet earned. There are 2 methods or approaches that can be used in recording precollections, namely:

Adjustments for Deferrals Precollections of Income On Oct. 1, 2009, the business collected P12,000 from a tenant representing an advance collection from building rental for one year. The accounting period ends on Dec. 31, 2009.

Adjustments for Depreciation Property & equipment are tangible assets which are held by an enterprise for use in the production or supply of goods and services for rental to others, or for administrative purposes, and are expected to be used during more than one year period. These include building, machinery, ships, aircrafts, motor vehicles, furniture and fixture, equipment and improvement to leased facilities. They are called depreciable assets which are all subject to depreciation. Land is not a depreciable assets because it is expected to be useful to the business enterprise for an indefinite period of time.

Adjustments for Depreciation The cost of the property and equipment is not being treated as an EXPENSE but rather an ASSET and generally carried at cost less accumulated depreciation equals Net Book Value. The portion of the cost of property and equipment that have been allocated over the number of years and charged to expense during the period is called DEPRECIATION EXPENSE.

Adjustments for Depreciation METHODS OF COMPUTING DEPRECIATION: There are various methods of computing depreciation but we’ll discuss only the STRAIGHT LINE METHOD. There are 3 factors involved in computing depreciation expense. Acquisition cost is the amount an entity paid to acquire the depreciable asset. It is the amount paid or liability incurred when the asset is bought. Scrap value or salvage value or residual value the estimated value of the asset at the end of its economic or useful life. It is the amount that the asset can probably be sold for at the end of its estimated useful life. Estimated useful life the estimated length of time usually stated in years that the asset can be of use. It is the estimated number of periods that an entity can make use of the asset. Useful life is an estimate, not an exact measurement.

Adjustments for Depreciation THE FORMULA FOR DEPRECIATION OF A STRAIGHT-LINE METHOD: To illustrate: On July 1, 2009, the business acquired an Office Equipment costing P60,000 with an estimated life of 5 years.

Adjustments for Estimated Uncollectible Accounts (or Estimated for doubtful accounts or Estimated for bad debts) Accounts Receivable represents the amount collectible arising from rendering of services to clients or customers and sale of merchandise to customers on account. When accounts receivables are already long overdue, some portion should be recorded as “uncollectible accounts,” otherwise known as “bad debts” or “doubtful accounts.”

Adjustments for Estimated Uncollectible Accounts (or Estimated for doubtful accounts or Estimated for bad debts) To illustrate: Assume that an entity made credit sales of P100,000 to customer A in 2009 and prior experience indicates an expected 1% average uncollectible accounts rate based on credit sales.

Adjustments for Estimated Uncollectible Accounts (or Estimated for doubtful accounts or Estimated for bad debts) When an account of a certain customer is already “hopeless” for collection, it is considered as worthless account or when there is positive evidence that a specific account is definitely uncollectible, the appropriate amount is written off against the contra account.

Adjustments or Corrections of Erroneous Entries • Wrong charging of account. • Correct charging of accounts but amounts are in error.

Quiz • The building was acquired costing P1,000,000 with an estimated life of 10 years. What is the annual depreciation? • The building was acquired on April 1, 2009, and the accounting period ends on Dec. 31, 2009. What is the depreciation expense for year ended Dec. 31, 2009? Give the adjusting entries. • The building was acquired on Oct. 1, 2009 and the accounting period ends on Dec. 31, 2009. what is the depreciation expense for the accounting period ends Dec. 31, 2009. Give the adjusting entries.

Quiz 4. The business has an outstanding Accounts Receivable from various customers in the amount of P20,000. At the end of its accounting period, it is estimated that 5% of this is doubtful of collection. Give the adjusting entry at the year –end Dec. 31, 2009. 5. Advertising expense has been incurred already on Dec. 27, 2009 but still unpaid, P30,000 and plan to pay it on Jan. 5, 2010. Give the adjusting entries.