Download

1 / 15

150 likes | 297 Views

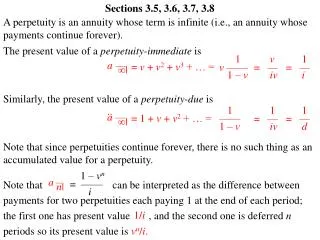

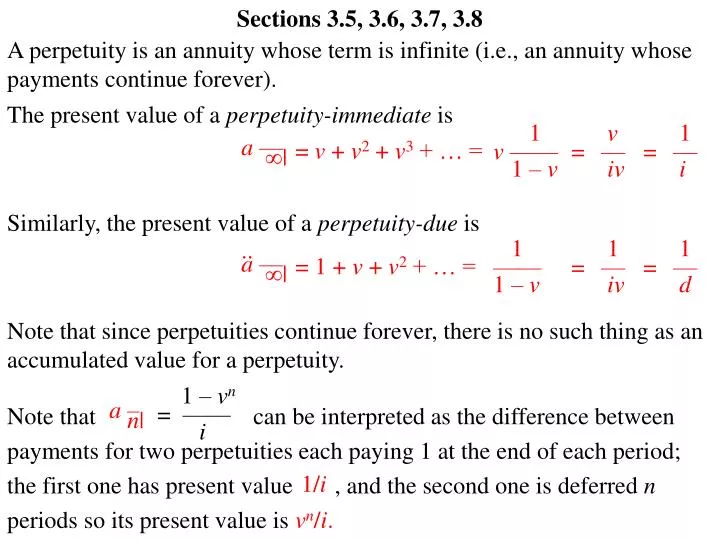

Sections 3.5, 3.6, 3.7, 3.8. A perpetuity is an annuity whose term is infinite (i.e., an annuity whose payments continue forever). The present value of a perpetuity-immediate is. 1 v —— = 1 – v. v — = i v. 1 — i. = v + v 2 + v 3 + … =. a –– |.

E N D

Sections 3.5, 3.6, 3.7, 3.8 A perpetuity is an annuity whose term is infinite (i.e., an annuity whose payments continue forever). The present value of a perpetuity-immediate is 1 v—— = 1 – v v — = iv 1 — i = v + v2 + v3 + … = a –– | Similarly, the present value of a perpetuity-due is 1 —— = 1 – v 1 — = iv 1 — d .. a –– | = 1 + v + v2 + … = Note that since perpetuities continue forever, there is no such thing as an accumulated value for a perpetuity. 1 – vn = —— i Note that can be interpreted as the difference between payments for two perpetuities each paying 1 at the end of each period; the first one has present value , and the second one is deferred n periods so its present value is a – n| 1/i vn/i.

An investment of $1,000,000 is to be made where a 5% effective interest rate is assumed. Payments of $50000 each year will begin in exactly one year. The first 10 payments go to Abernathy, the next 20 payments go to Barnabas, and continuing payments thereafter go to Charity. Find the lump sums (adding to $1,000,000 of course) that could be immediately paid to Abernathy, Barnabas, and Charity, which would be equivalent to the perpetuity. The present value of the payments to Abernathy is 50000 = 50000(7.7217349) = $386,087 a –– 10 | 0.05 The present value of the payments to Barnabas is 50000 = (1.05–10) 50000(1.05–10)(12.4622103) = $382,536 a –– 20 | 0.05 The present value of the payments to Charity is 50000 = (1.05–30) 50000(1.05–30)(1/0.05) = $231,377 a –– | 0.05

1 – vn —— i If is an annuity under which = v + v2 + … + vn = a – n| payments of 1 are made at the end of each of period for n periods, then for 0 < k < 1, how can we interpret ? a—— n + k| Payments 1 1 1 1 Payment Possibilities Periods 0 1 2 … n– 1 n There are three possible interpretations. The “mathematical” interpretation: Although n must be an integer in the derivation of the final formula for , a non-integer value can be used in that final formula. Consequently, we can say a – n| 1 – vn+k = ——— = i 1 – vn + vn – vn+k ——————– = i 1 – vn —— i v–k– 1 + vn+k ——– = i a—— n + k|

Payments 1 1 1 1 Payment Possibilities M Periods 0 1 2 … n– 1 n n+ 1 n+k 1 – vn+k = ——— = i 1 – vn + vn – vn+k ——————– = i 1 – vn —— i v–k– 1 + vn+k ——– = i a—— n + k| 1 – vn —— i (1 + i)k– 1 + vn+k ————– i This final payment is made at time n + k and can be shown to be close to the value k (by using a Taylor series expansion about i = 0). We can label this final payment as M.

Payments 1 1 1 1 Payment Possibilities B M Periods 0 1 2 … n– 1 n n+ 1 n+k The “balloon payment” interpretation: A smaller additional payment is added to the last regular payment. If we label this smaller additional payment as B, then we can say 1 – vn+k = ——— = i 1 – vn —— i 1 –vk + vn ——– i a—— n + k| B

Payments 1 1 1 1 Payment Possibilities B M D Periods 0 1 2 … n– 1 n n+ 1 n+k The “drop payment” interpretation: A smaller additional payment is made one period after the last regular payment. If we label this smaller additional payment as D, then we can say 1 – vn+k = ——— = i 1 – vn —— i v–1–vk–1 + vn+1 ———– i a—— n + k| D The “mathematical” interpretation is rarely used in practice, and the other two methods are very often used.

An investment of $3000 is to be used to make payments of $250 at the end of every year for as long as possible. If the fund earns an annual effective rate of interest of 7%, find how many regular payments can be made, and then find each of the following: (a) (b) (c) the time for, and the amount of, the smaller additional payment according to the “mathematical” interpretation. the smaller additional balloon payment added to the last regular payment. the smaller additional drop payment made one period after the last regular payment. The equation of value is = 3000 250 a—— n + k| 0.07 1 – 1.07–(n+k) ————— = 12 0.07 n + k = 27.0857 n = 27 and k = 0.0857

The equation of value is = 3000 250 a—— n + k| 0.07 1 – 1.07–(n+k) ————— = 12 0.07 n + k = 27.0857 n = 27 and k = 0.0857 (1 + i)k– 1 250 ————– = i For part (a), the last payment at time 27.0857 is 1.070.0857– 1 250 —————– = 0.07 $20.77 For part (b), the additional (balloon) payment added to the last regular payment at time 27 is 1 –vk 250 ——– = i 1 – (1.07)–0.0857 250 ——–———– = 0.07 $20.65 For part (c), the additional (drop) payment at time 28 is v–1–vk–1 250 ———– = i 1.07 – (1.07)–0.0857+1 250 ——–—————— = 0.07 $22.09

An investment of $4000 is intended to be used to make payments of $250 at the end of every year for as long as possible, and the fund earns an annual effective rate of interest of 7%. Explain why the payments will go on forever. The present value of a perpetuity with payments of $250 at the end of each year earning an annual effective rate of interest of 7% is 1 250 —— = 0.07 $3571.43 which is less than $4000.

Look at Example 3.8. Note how the calculations can be done with a TI calculator as follows: Press the APPS button, and selecting the Finance option. Select the TVM Solver option. Set N = 20, PV = 16, PMT = 1 Press the ALPHA button followed by the SOLVE button. These results should match the results in the example. Then, look at Example 3.9 where formula (3.21) is used to compute the answer to Example 3.8: 2(20 16)/[(16)(21)] = 0.0238095. Look at Example 3.10.

We shall next consider situations in which interest can vary each period, but compound interest is still in effect. Let ik denote the rate of interest applicable from time k– 1 to time k. If ik is applicable only for period k with payment #k made at time k, then = (1 + i1)–1 + (1 + i1)–1(1 + i2)–1 + … + (1 + i1)–1(1 + i2)–1…(1 + in)–1 a – n| This is called the portfolio rate method. If ik is applicable for the payment made at time k over all k periods, then = (1 + i1)–1 + (1 + i2)–2 + … + (1 + in)–n a – n| This is called the yield curve method. If ik is applicable only for period k with payment #k made at time k, then .. s – n| = (1 + i1)(1 + i2)…(1 + in) + (1 + i2)(1 + i3)…(1 + in) + … + (1 + in) This is called the portfolio rate method. If ik is applicable for the payment made at time k over all k periods, then .. s – n| = (1 + i1)n + (1 + i2)n–1 + … + (1 + in) This is called the yield curve method.

Find the accumulated value of a 12-year annuity-immediate of $500 per year, if the effective rate of interest (for all money) is 8% for the first 3 years, 6% for the following 5 years, and 4% for the last 4 years. The accumulated value of the first 3 payments to the end of year 3 is 500 = 500(3.2464) = $1623.20 s – 3 | 0.08 The accumulated value of the first 3 payments to the end of year 8 at 6% and then to the end of year 12 at 4% is 1623.20(1.06)5(1.04)4 = $2423.55 The accumulated value of payments 4, 5, 6, 7, and 8 to the end of year 8 is 500 = 500(5.6371) = $2818.55 s – 5 | 0.06 The accumulated value of payments 4, 5, 6, 7, and 8 to the end of year 12 at 4% is 2818.55(1.04)4 = $3297.30

Find the accumulated value of a 12-year annuity-immediate of $500 per year, if the effective rate of interest (for all money) is 8% for the first 3 years, 6% for the following 5 years, and 4% for the last 4 years. The accumulated value of payments 9, 10, 11, and 12 to the end of year 12 is 500 = 500(4.2465) = $2123.23 s – 4 | 0.04 The accumulated value of the 12-year annuity immediate is $2423.55 + $3297.30 + $2123.23 = $7844.08

Find the accumulated value of a 12-year annuity-immediate of $500 per year, where the first 3 payments are invested at an effective rate of interest of 8%, the following 5 payments are invested at an effective rate of interest of 6%, and the last 4 payments are invested at an effective rate of interest of 4%. The accumulated value of the first 3 payments to the end of 3 years is 500 = 500(3.2464) = $1623.20 s – 3 | 0.08 The accumulated value of the first 3 payments to the end of year 12 at 8% is 1623.20(1.08)9 = $3244.78 The accumulated value of payments 4, 5, 6, 7, and 8 to the end of year 8 is 500 = 500(5.6371) = $2818.55 s – 5 | 0.06 The accumulated value of payments 4, 5, 6, 7, and 8 to the end of year 12 at 6% is 2818.55(1.06)4 = $3558.35

Find the accumulated value of a 12-year annuity-immediate of $500 per year, where the first 3 payments are invested at an effective rate of interest of 8%, the following 5 payments are invested at an effective rate of interest of 6%, and the last 4 payments are invested at an effective rate of interest of 4%. The accumulated value of payments 9, 10, 11, and 12 to the end of year 12 is 500 = 500(4.2465) = $2123.23 s – 4 | 0.04 The accumulated value of the 12-year annuity immediate is $3244.78 + $3558.35 + $2123.23 = $8926.36