Download

1 / 7

70 likes | 168 Views

Foreign exchange volatility is likely to pick up over the coming weeks as we approach the Federal Open Market Committee meeting on December 16th.

E N D

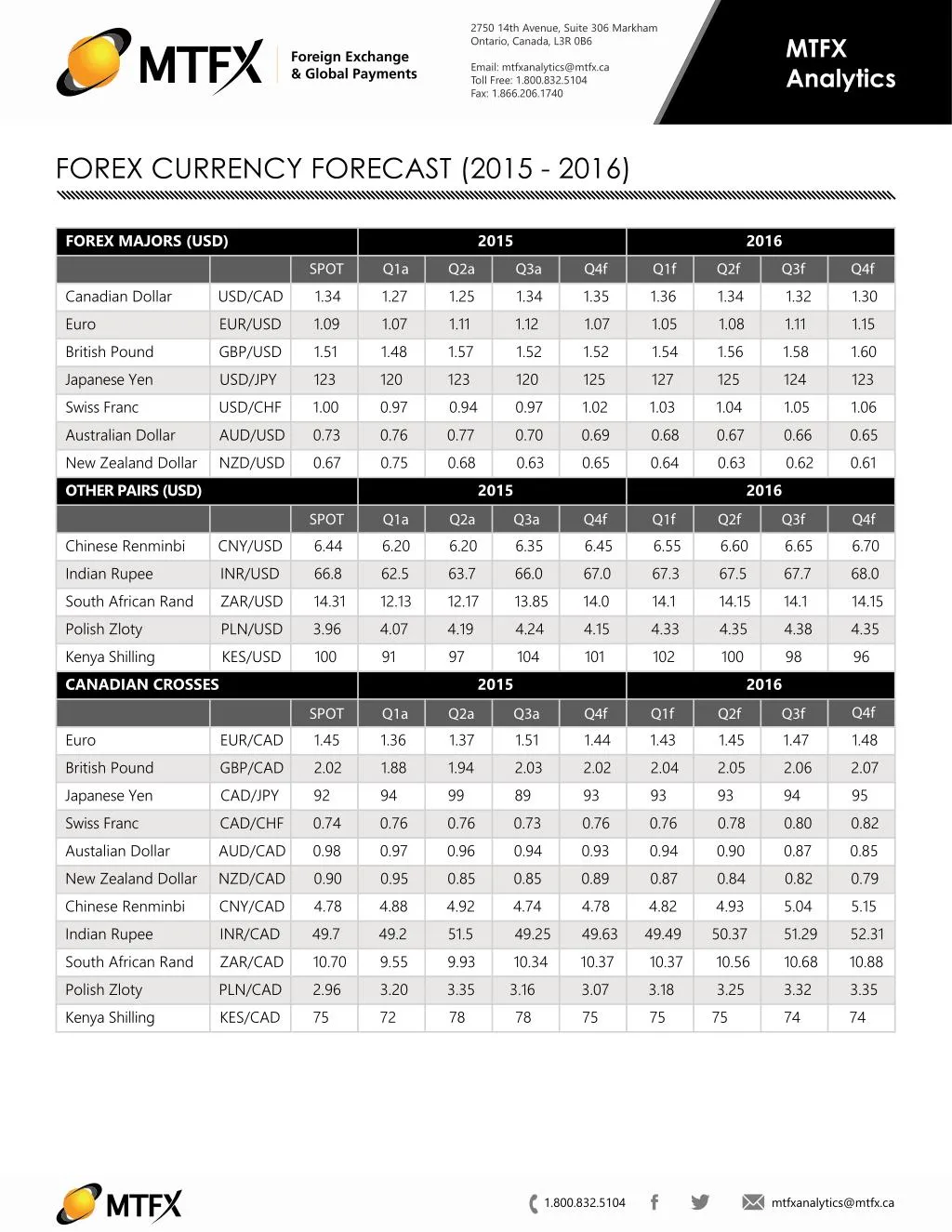

2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 Email: mtfxanalytics@mtfx.ca Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 MTFX Analytics Section 6 FOREX CURRENCY FORECAST (2015 - 2016) FOREX MAJORS (USD) 2015 2016 SPOT 1.34 1.09 1.51 123 1.00 0.73 0.67 Q1a 1.27 1.07 1.48 120 0.97 0.76 0.75 Q2a 1.25 1.11 1.57 123 0.94 0.77 0.68 Q3a 1.34 1.12 1.52 120 0.97 0.70 0.63 Q4f 1.35 1.07 1.52 125 1.02 0.69 0.65 Q1f 1.36 1.05 1.54 127 1.03 0.68 0.64 Q2f 1.34 1.08 1.56 125 1.04 0.67 0.63 Q3f 1.32 1.11 1.58 124 1.05 0.66 0.62 Q4f 1.30 1.15 1.60 123 1.06 0.65 0.61 Canadian Dollar Euro British Pound Japanese Yen Swiss Franc Australian Dollar New Zealand Dollar OTHER PAIRS (USD) USD/CAD EUR/USD GBP/USD USD/JPY USD/CHF AUD/USD NZD/USD 2015 2016 SPOT Q1a Q2a Q3a Q4f Q1f Q2f Q3f Q4f Chinese Renminbi Indian Rupee South African Rand Polish Zloty Kenya Shilling CANADIAN CROSSES CNY/USD INR/USD ZAR/USD PLN/USD KES/USD 6.44 66.8 14.31 3.96 100 6.20 62.5 12.13 4.07 91 6.20 63.7 12.17 4.19 97 6.35 66.0 13.85 4.24 104 6.45 67.0 14.0 4.15 101 6.55 67.3 14.1 4.33 102 6.60 67.5 14.15 4.35 100 6.65 67.7 14.1 4.38 98 6.70 68.0 14.15 4.35 96 2015 2016 Q4f SPOT Q1a Q2a Q3a Q4f Q1f Q2f Q3f Euro British Pound Japanese Yen Swiss Franc Austalian Dollar New Zealand Dollar Chinese Renminbi Indian Rupee South African Rand Polish Zloty Kenya Shilling EUR/CAD GBP/CAD CAD/JPY CAD/CHF AUD/CAD NZD/CAD CNY/CAD INR/CAD ZAR/CAD PLN/CAD KES/CAD 1.45 2.02 92 0.74 0.98 0.90 4.78 49.7 10.70 2.96 75 1.36 1.88 94 0.76 0.97 0.95 4.88 49.2 9.55 3.20 72 1.37 1.94 99 0.76 0.96 0.85 4.92 51.5 9.93 3.35 78 1.51 2.03 89 0.73 0.94 0.85 4.74 49.25 10.34 3.16 78 1.44 2.02 93 0.76 0.93 0.89 4.78 49.63 10.37 3.07 75 1.43 2.04 93 0.76 0.94 0.87 4.82 49.49 10.37 3.18 75 1.45 2.05 93 0.78 0.90 0.84 4.93 50.37 10.56 3.25 75 1.47 2.06 94 0.80 0.87 0.82 5.04 51.29 10.68 3.32 74 1.48 2.07 95 0.82 0.85 0.79 5.15 52.31 10.88 3.35 74 1.800.832.5104 mtfxanalytics@mtfx.ca

2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 Email: mtfxanalytics@mtfx.ca Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 MTFX Analytics Section 6 DECEMBER 2015 - CURRENCY HIGHLIGHTS The US dollar bull trend remains intact and will regain a renewed vigor in the weeks ahead. Last week’s non-farm payrolls report and Yellen’s congressional testimony all point to the Fed taking its first step toward higher interest rates on December 16th. Most of the market is already heavily invested in the US dollar suggesting a potential for significant volatility ahead of December 16th. Bias – bullish (stronger USD) USD The loonie continues to show signs of vulnerability with further weakness expected against the US dollar in early 2016. Recent fundamentals have been disappointing despite the economy rebounding from a technical recession. With commodity prices continuing to remain soft and a pronounced policy divergence between the Fed and the BoC, there remains significant risk for further loonie weakness. Bias – bearish (weaker CAD) CAD All the hype that surrounded Mario Draghi and significant further stimulus by the ECB did not live up to expectations. The ECB did cut deposit rates further into negative territory and committed to extending QE purchases well into 2017, however, failed to increase the amount of purchases expected by most of the market. The gains enjoyed by the euro may be short lived as the market turns its attention to fundamentals which continue to remain weak. Bias – bearish (weaker EUR) EUR The British pound had an awful month of November and is expected to track a lower flight plan in the near term. Fundamentals across the UK continue to remain strong compared to its peers and despite concerns over low inflation, the Bank of England is likely to follow the Fed’s lead and begin policy normalization in H1 2016 which should be pound supportive. Bias – Bullish (stronger GBP) GBP 1.800.832.5104 mtfxanalytics@mtfx.ca

2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 Email: mtfxanalytics@mtfx.ca Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 MTFX Analytics Section 6 DECEMBER 2015 - US DOLLAR HIGHLIGHTS December 2015 2015f 2016f Spot Q1a Q2a Q3a Q4f Q1f Q2f Q3f Q4f 1.27 1.24 1.34 1.35 1.36 1.07 1.05 1.52 1.51 1.36 1.37 1.05 1.04 1.57 1.51 1.34 1.38 1.08 1.05 1.58 1.49 1.32 1.39 1.11 1.04 1.59 1.45 1.30 1.39 1.15 1.03 1.60 1.44 USD/CAD MTFX 1.34 Consensus Forecast 1.07 1.11 1.12 EUR/USD MTFX 1.09 Consensus Forecast 1.48 1.57 1.51 GBP/USD MTFX 1.51 Consensus Forecast U.S. DOLLAR COMMENT: Foreign exchange volatility is likely to pick up dramatically as we move toward the Fed meeting where it is expected that the Fed will take its first initial step towards policy normalization. The US dollar bull trend continues to remain well entrenched and the currency should continue to remain supported fuelled by growth and interest rate differentials. NOVEMBER 2015 CURRENCY RETURNS 0.0% CAD EUR GBP -0.5% -1.0% -1.5% -2.0% Fundamentally the US economy is showing moderate growth averaging 2.25% heading into the year-end. While recent reports have been mixed, consumer spending and housing activity continue to remain well supported by low borrowing costs, cheap oil prices, a robust job market and rising income gains. Recent hiring gains have pushed the unemployment rate to a seven-year low of 5.0% while measures of underutilization continue to improve. Consum- er confidence has softened in recent months but continues remain well above consensus. Industrial activity remains soft as a result of sluggish export sales being weighed by a strong US dollar. However, domestic sales continue to maintain an expansionary tone led by manufacturing production and consumer goods. Business investment continues to increase while service activity is reporting broad-based gains. Core inflation is holding steady at just under 2% and appears to have bottomed out. Taken together, fundamentals suggest that Yellen and the Fed should have more than enough ammunition to begin interest rate liftoff on December 16th. -2.5% -3.0% -3.5% -4.0% -4.5% EVENTS TO WATCH DECEMBER 2015 ECONOMIC EVENT USD Retail Sales USD Producer Price Inflation (PPI) USD Consumer Price Inflation (CPI) USD FOMC Statement & Interest Rate Decision USD Philadelphia Manufacturing Index DATE DEC 11 DEC 11 DEC 15 DEC 16 DEC 17 As the Fed moves on rate hikes, monetary policy divergence between the US and other G7 countries will become more pronounced with most countries continuing to remain entrenched in ongoing easing policies. The US continues to remain insulated to external pressures given its large and healthy domestic market. As a result, market analysts expect significant dollar strength against most majors through the month of December and well into 2016. 1.800.832.5104 mtfxanalytics@mtfx.ca

2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 Email: mtfxanalytics@mtfx.ca Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 MTFX Analytics Section 6 USD/CAD DECEMBER 2015 HIGHLIGHTS December 2015 2015f 2016f USD/CAD Spot Q1a 1.27 Q2a 1.24 Q3a 1.34 Q4f 1.35 1.36 Q1f 1.36 1.37 Q2f 1.34 1.38 Q3f 1.32 1.39 Q4f 1.30 1.39 MTFX Forecast 1.34 Consensus Forecast USD/CAD CURRENCY TREND - NOVEMEBR 2015 HIGHLIGHTS: Despite the sideways trading range since peaking to 1.3450 in October, the underlying US dollar strength is likely to assert itself in the weeks ahead. Domestic risks continue to be skewed to the downside as a result of ongoing weakness in commodity prices coupled with weak employment, inflation and growth. 1.34 1.335 1.33 1.325 1.32 1.315 1.31 Markets expect no significant pick-up in commodity prices in the medium term which will provide additional head- winds for domestic growth prospects. Any further deterioration in economic fundamentals is likely to be met with a dovish BoC that may increase mone- tary easing to kick-start the economy. 1.305 1.3 As the Fed raises interest rates, further loonie weakness is likely in the near term. However, the current elevated levels of weakness are unlikely to persist as we enter H2 of 2016. Oil should recover somewhat and the Fed is likely to take a very measured approach to rate hikes, allowing the loonie to stabilize toward the latter part of 2016 and gain against the green- back. EVENTS TO WATCH DECEMBER 2015 ECONOMIC EVENT CAD BoC Governor Poloz Speech DATE DEC 08 USD FOMC Statement & Interest Rate Decision CAD Consumer Price Inflation (CPI) CAD Retail Sales DEC 16 DEC 18 DEC 23 CAD Gross Domestic Product DEC 23 MARKET SENTIMENT: Bearish Bullish 1.800.832.5104 mtfxanalytics@mtfx.ca

2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 Email: mtfxanalytics@mtfx.ca Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 MTFX Analytics Section 6 EUR/USD DECEMBER 2015 HIGHLIGHTS December 2015 2015f 2016f EUR/USD Spot Q1a 1.07 Q2a 1.11 Q3a 1.12 Q4f 1.07 1.05 Q1f 1.05 1.04 Q2f 1.08 1.05 Q3f 1.11 1.04 Q4f 1.15 1.03 MTFX Forecast 1.09 Consensus Forecast EUR/USD CURRENCY TREND - NOVEMBER 2015 HIGHLIGHTS: The hype that began in October when Mario Draghi hinted of further stimulus did not live up to expectations last week and resulted in a violent move higher for the euro against all other currencies. The euro gains enjoyed will be short lived as markets turn their attention back to fundamentals and the upcoming Fed meeting. 1.11 1.1 1.09 1.08 1.07 The ECB cut its deposit rate further into negative territory and extended its QE purchases through to March 2017. The goal of the ECB seems to remain a further depreciation of the currency, which will not only increase inflation across the Eurozone but also make the Eurozone more competitive on the global stage. 1.06 1.05 In the longer term, as stimulus makes its way through the economy, there are signs of “green shoots” that could see the euro rebound. Fundamentally, inflation readings are higher and growth appears to be continuing at a moderate pace. Stabilization of funda- mentals should allow the single curren- cy to recover and stabilize in the mid-teens by end of 2016. EVENTS TO WATCH DECEMBER 2015 ECONOMIC EVENT EUR German ZEW Sentiment DATE DEC 15 EUR German Manufacturing PMI EUR Consumer Price Inflation USD FOMC Statement & Interest Rate Decision DEC 16 DEC 16 DEC 16 EUR German IFO Business Climate DEC 17 MARKET SENTIMENT: Bearish Bullish 1.800.832.5104 mtfxanalytics@mtfx.ca

2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 Email: mtfxanalytics@mtfx.ca Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 MTFX Analytics Section 6 GBP/USD DECEMBER 2015 HIGHLIGHTS December 2015 2015f 2016f GBP/USD Spot Q1a 1.48 Q2a 1.57 Q3a 1.51 Q4f 1.52 1.51 Q1f 1.57 1.51 Q2f 1.58 1.49 Q3f 1.59 1.45 Q4f 1.60 1.44 MTFX Forecast 1.51 Consensus Forecast HIGHLIGHTS: GBP/USD CURRENCY TREND - NOVEMBER 2015 The British Pound is likely to have a lower flight plan in the short term. The confidence in the timing of rate increases by the Bank of England have weakened as investors have expressed disappointment with the softer domes- tic data and a dovish BoE. The GBP/USD traded below 1.50 for the first time since April suggesting heightened volatility in the currency. 1.545 1.535 1.525 1.515 1.505 Fundamentally, the UK continues to outperform most of its peers driven by a combination of high levels of employment and a dramatic rise in real earnings. GDP growth continues to lead the G7 with both consumption and confidence at multi-year highs, allowing for a relatively strong economic outlook. 1.495 EVENTS TO WATCH DECEMBER 2015 ECONOMIC EVENT GBP BoE Interest Rate Decision & Minutes DATE Despite the recent dovish sentiment by the BoE, most expect the bank to take further steps in the direction of rate hikes in H1 2016. As the BoE flexes its wings, the pound should get a boost, outperform on crosses, and hold its own against the US dollar over the coming months. We hold 2016 year-end target of 1.57. DEC 10 GBP Consumer Price Inflation GBP Employment Data GBP FOMC Statement & Interest Rate Decision DEC 11 DEC 16 DEC 16 DEC 17 GBP Retail Sales MARKET SENTIMENT: Bearish Bullish 1.800.832.5104 mtfxanalytics@mtfx.ca

2750 14th Avenue, Suite 306 Markham Ontario, Canada, L3R 0B6 Email: mtfxanalytics@mtfx.ca Toll Free: 1.800.832.5104 Fax: 1.866.206.1740 MTFX Analytics Section 6 FOREIGN EXCHANGE DISCLAIMER This publication has been prepared by MTFX Inc. for informational and marketing purposes only. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable, but no representation or warranty, express or implied, is made as to their accuracy or completeness and neither the information nor the forecast shall be taken as a representation for which MTFX Inc., its affiliates or any of their employees incur any responsibility. Neither MTFX Inc. nor its affiliates accept any liability whatsoever for any loss arising from any use of this information. - MTFX Analytics 2750 14th Avenue, Suite 306 Markham, Ontario Canada L3R 0B6 Toll Free: 1.800.832.5104 Fax: 1.866.832.5104 Email: mtfxanalytics@mtfx.ca This report has been prepared by MTFX Inc. as a resource for its clients. The opinions, projections and estimates contained herein are our own and subject to change without notice. 1.800.832.5104 mtfxanalytics@mtfx.ca