Download

1 / 27

290 likes | 749 Views

Short-Term Financial Management. Dr. Del Hawley MBA 622. 1,400. 1,200. 1,000. Quarterly Sales ($ in millions). 800. 600. 400. 200. Quarterly Sales. 0. 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002. Year.

E N D

Short-Term Financial Management Dr. Del Hawley MBA 622

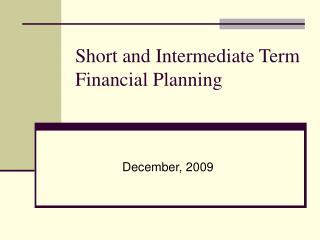

1,400 1,200 1,000 Quarterly Sales ($ in millions) 800 600 400 200 Quarterly Sales 0 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 Year Quarterly Sales for Hershey Foods (1992 – 2002)

1,800 1,600 1,400 1,200 1,000 Total Assets($ in millions) 800 600 Hershey’s Current Assets Matching Strategy Conservative Strategy Aggressive Strategy 400 200 0 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 Quarters (1992-2002) Financing Strategies Available to Hershey

Conservative strategy • Use long-term financing to cover both permanent assets and temporary assets. Aggressive strategy • Use short-term financing to fund both seasonal peaks and part of long-term growth in sales and assets. Matching strategy • Finance permanent assets with long-term funding sources and temporary asset requirement with short-term financing. Short-Term Financing Strategies Companies can adopt the following strategies to fund long-term needs and seasonal fluctuations of sales:

Time from the beginning of the production to the time when cash is collected from sale • Financing the operating cycle is costly, so firms have an incentive to shrink it. Operating cycle Cash conversion cycle • Operating cycle less the average payment period on accounts payable time = 0 Operating cycle Sell finished goodson account Purchase rawmaterials on account Collect accountsreceivable Average Age of Inventory Average Collection Period Average paymentperiod Payment mailed Cash Conversion Cycle Time The Cash Conversion Cycle

Cost 1 (holding cost) Cost 2 * (cost of holding too little of operating asset) Operating Assets Cash and marketable securities Opportunity cost of funds Illiquidity and solvency costs Accounts receivable Cost of investment in accounts receivable and bad debts Opportunity cost of lost sales due to overly restrictive credit policy and/or terms Inventory Carrying cost of inventory, including financing, ware housing, obsolescence costs, etc. Order and setup costs associated with replenishment and production of finished goods Short-Term Financing Accounts payable, accruals, and notes payable Cost of reduced liquidity caused by increasing current liabilities Financing costs resulting from the use of less expensive short-term financing rather than more expensive long-term debt and equity financing Cost Tradeoffs in Working Capital Accounts

Determine its credit standards. • Set the credit terms. • Develop collection policy. • Monitor its A/R on both individual and aggregate basis. If a company decides to offer trade credit, it must: • Apply techniques to determine which customers should receive credit. • Use internal and external sources to gather information relevant to the decision to extend credit to specific customers. • Take into account variable costs of the products sold on credit. Credit standards Credit selection techniques Five C’s of Credit Credit scoring Accounts Receivable Management

Character: The applicant’s record of meeting past obligations; desire to repay debt if able to do so • Capacity: The applicant’s ability to repay the requested credit • Capital: The financial strength of the applicant as reflected by its ownership position • Collateral: The amount of assets the applicant has available for use in securing the credit • Conditions: Refers to current general and industry-specific economic conditions Five C’s of Credit Framework for in-depth credit analysis that is typically used for high-dollar credit requests:

An example… • WEG Oil uses credit scoring to make credit decisions. WEG Oil decision rule is: • Credit Score > 75: extend standard credit terms • 65 < Credit Score < 75: extend limited credit (convert to standard credit terms after 1 year if account is properly maintained) • Credit Score < 65: reject application Credit Scoring Uses statistically-derived weights for key credit characteristics to predict whether a credit applicant will pay the requested credit in a timely fashion. • Used with high volume/small dollar credit requests • Most commonly used by large credit card operations, such as banks, oil companies, and department stores.

Financialand Credit Characteristics Score(0 to 100)(1) Predetermined Weight(2) Weighted Score[(1) X (2)](3) Credit references 80 0.15 12.00 Home ownership 100 0.15 15.00 Income range 75 0.25 18.75 Payment history 80 0.25 20.00 Years at address 90 0.10 9.00 Years on job 85 0.10 8.50 1.00 83.25 Credit Scoring of a Consumer Credit Application by WEG Oil

Increase in sales and profits (if positive contribution margin), but higher costs from additional A/R and additional bad debt expense. Credit standards relaxed Credit standards tightened • Reduced investment in A/R and lower bad debt, but lower sales and profit. • An example…YMC wants to evaluate the effects of a relaxation of its credit standards: • YMC sells CD organizers for $12/unit. All sales are on credit. YMC expects to sell 140,000 units next year. • Variable costs are $8/unit and fixed costs are $200,000 per year. • The change in credit standards will result in: • 5% increase in sales; average collection period will increase from 30 to 45 days; increase in bad debt from 1% to 2%. Changing Credit Standards

Marginal profit from increased sales Cost of marginal investment in A/R Average investment inaccounts receivable (AIAR) Effects of Changes in Credit Standards for YMC Additional profit contribution from sales Cost of the marginal investment in accounts receivables • To compute additional investment, use the following equations:

Total variable cost of annual sales (TVC) Turnover of account receivable (TOAR) Cost of the marginal investment in accounts receivables

Cost of marginalinvestment in A/R Cost of the marginal investment in accounts receivables Compute additional investment and, assuming a required return of 12%, compute cost of marginal investment in A/R.

Cost of marginal bad debt expense Marginal profit from increased sales Cost of marginalbad debts Net profit for the credit decision Cost of marginalinvestment in A/R = - - = $28,000 - $6,406 - $18,480 = $3,114 Cost of Marginal Bad Debt Expense 3. Cost of marginal bad debt expense Subtract the current level of bad debt expense (BDECURRENT) from the expected level of bad debt expense (BDEPROPOSED). 4. Net profit for the credit decision

The ongoing review of a firm’s accounts receivable to determine if customers are paying according to stated credit terms Credit monitoring Techniques for credit monitoring • Average collection period • Aging of accounts receivable • Payment pattern monitoring Average collection period: the average number of days credit sales are outstanding Credit Monitoring Aging of accounts receivable: schedule that indicates the portions of total A/R balance outstanding

Payment pattern: the normal timing within which a firm’s customers pay their accounts • Percentage of monthly sales collected the following month • Should be constant over time; if payment pattern changes, the firm should review its credit policies • An example… • DJM Manufacturing determined that: • 20% of sales collected in the month of sales, 50% in the next month and 30% two months after the sale. • Can use payment pattern to construct cash receipts from the cash budget: • If January sales are $400,000, DJM expects to collect $80,000 in January, $200,000 in February, and $120,000 in March. Credit Monitoring

Cash management • Financial relationships with banks • Cash flow forecasting • Investing and borrowing • Development and maintenance of information systems for cash management Cash manager responsible for Time Processing float Availability float Clearing float Mail float Cash Management Cash management: the collection, concentration, and disbursement of funds Float: funds that have been sent by the payer but not yet usable funds to the company

Bank provides report to its customers to show recent activity in firms’ accounts. • Banks cannot pay interest on corporate checking account balances. • Firms use earnings credit for balances to offset charges. Bank account analysis statement Cash Position Management Cash position management: collection, concentration, and disbursement of funds on a daily basis • Management of short-term investing if the company has a surplus of funds and borrowing arrangements if company has a temporary deficit of funds Smaller companies set target cash balance for their checking accounts.

Field-banking system • Collections are made over the counter (retail) or at a collection office (utilities). Mail-based system • Mail payments are processed at companies’ collection centers. Electronic payments • Becoming increasingly popular because they offer advantages to both parties. Collections Primary objective: speeding up collections Collection systems: function of the nature of the business

Speeds up collections because it affects all components of float. • Customers mail payments to a post office box. • Firm’s bank empties the box and processes each payment and deposits the payments in the firm’s account. • Lockboxes reduce mail and clearing time. Lockbox system • FVR = float value reduction in dollars • ra = cost of capital • LC = annual operating cost of the lockbox system Collections Perform cost-benefit analysis to determine if lockbox system worth using

Depository transfer checks • Unsigned check drawn on one of the firm’s bank accounts and deposited in another of the firm’s bank accounts • Preauthorized electronic withdrawal from the payer’s account • Settle accounts among participating banks. Individual accounts are settled by respective bank balance adjustments. • Transfers clear in one day. Automated clearinghouse debit transfers • Electronic communication that, via bookkeeping entries, removes funds from the payer’s bank and deposits the funds in the payee’s bank. • Expensive: used only for high-dollar payments • Fedwire: primary wire transfer system in US Wire transfers Funds Transfer Mechanisms

Examine all incoming invoices and determine the amount to be paid. • Control function: cash manager verifies that invoice information matches purchase order and receiving information. Accounts payable functions Accounts Payable Management Management of time from purchase of raw materials until payment is placed in the mail Decide between centralized or decentralized payables and payments systems If supplier offers cash discounts, analyze the best alternative between paying at the end of credit period and taking the discount.

Disbursements Products and Methods • Zero-balance accounts (ZBAs): disbursements accounts that always have end-of-day balance of zero • Allows the firm to maximize the use of float on each check, without altering the float time of its suppliers • Keeps all cash in interest-bearing accounts • Controlled disbursement: Bank provides early notification of checks presented against a company’s account every day. • Federal Reserve Bank makes two presentments of checks to be cleared each day for most large cash management banks. • Positive pay: Company transmits to the bank a check-issued file to the bank when checks are issued. • Check-issued file includes check number and amount of each item. • Used for fraud prevention

Developments in Accounts Payable and Disbursements • Integrated (comprehensive) accounts payable: outsourcing of accounts payable or disbursements operations • Purchasing/procurement cards: increased use of credit cards for low-dollar indirect purchases • Imaging services: Both sides of the check, as well as remittance information, is converted into digital images. • Useful when incorporated with positive pay services • Fraud prevention in disbursements: fraud prevention measures: • Written policies and procedures for creating and disbursing checks; separating duties (approval, signing, reconciliation) • Using safety features on checks; setting maximum dollar limits and/or requiring multiple signatures

Short-Term Financial Management Length of cash conversion cycle determines the amount of resources the firm must invest in its operations. Cost trade-offs apply to managing cash and marketable securities, account receivable, inventory and account payable. Objective for account receivable: collect accounts as quickly as possible without losing sales. Objective for accounts payable: pay accounts as slowly as possible without damaging firm’s credit.