Download

1 / 4

50 likes | 83 Views

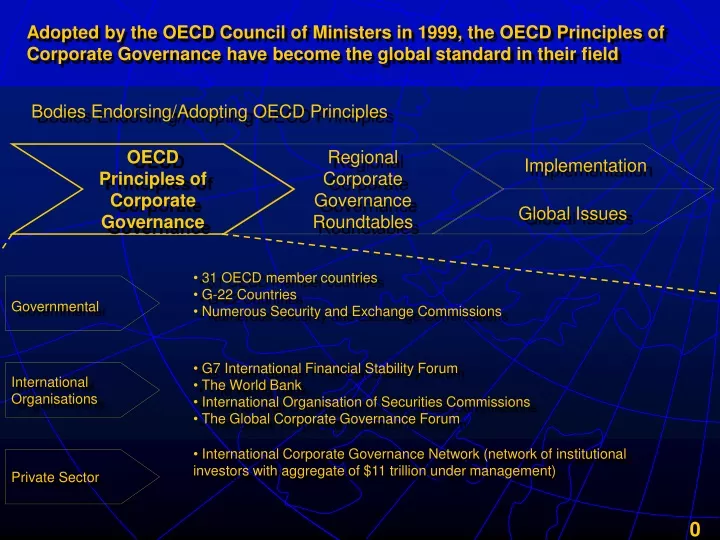

Adopted by the OECD Council of Ministers in 1999, the OECD Principles of Corporate Governance have become the global standard in their field. Bodies Endorsing/Adopting OECD Principles. Implementation. OECD Principles of Corporate Governance. Regional Corporate Governance Roundtables.

E N D

Adopted by the OECD Council of Ministers in 1999, the OECD Principles of Corporate Governance have become the global standard in their field Bodies Endorsing/Adopting OECD Principles Implementation OECD Principles of Corporate Governance Regional Corporate Governance Roundtables Global Issues • 31 OECD member countries • G-22 Countries • Numerous Security and Exchange Commissions Governmental • G7 International Financial Stability Forum • The World Bank • International Organisation of Securities Commissions • The Global Corporate Governance Forum International Organisations • International Corporate Governance Network (network of institutional investors with aggregate of $11 trillion under management) Private Sector

This global standard provides a common reference point for international policy dialogue and exchange of experience Framework of Corporate Governance Debate Implementation OECD Principles of Corporate Governance Regional Corporate Governance Roundtables Global Issues • That blend of law, regulation and appropriate voluntary private-sector practices which enables the corporation to attract financial and human capital, perform efficiently, and thereby perpetuate itself by generating long-term economic value for its shareholders, while respecting the interests of stakeholders and society as a whole* Corporate Governance Defined Chapters of OECD Principles • Shareholders’ Rights • Equitable Treatment of Shareholders • Role of Stakeholders • Disclosure and Transparency • Responsibility of Board of Directors * Millstein report

Pursuant to a G-7 mandate to the OECD and the World Bank, the OECD organizes and leads five regional roundtables to raise awareness of corporate governance and to develop a regional self-assessment of corporate-governance successes and areas for further reform Regional Corporate Governance Roundtables Implementation OECD Principles of Corporate Governance Regional Corporate Governance Roundtables Global Issues • Asia, Russia, Latin America, Eurasia, South-eastern Europe Regions • Peer discussion among senior policy makers, academics and businessmen using the OECD Principles of Corporate Governance as a conceptual framework Format • Policy dialogue on realising the OECD Principles in the context of each country of the region • Self assessment and regional comparison of successes and areas requiring further effort • Knowledge sharing and networking among key regional decision makers Goals • White Paper describing state of corporate governance in region and identifying areas for further reform • Consensus document adopted by representatives from the region • Blueprint for future policy work and technical assistance Output

The Asian Roundtable has recently issued a White Paper on Corporate Governance in Asia putting forth six key recommendations for corporate-governance reform Asian White Paper Priority Recommendations • Training and education • Codes of conduct • Technical assistance Raise awareness • Focus on public-service integrity and even-handedness • Increase regulatory and judicial resources and specialization • Use simpler and easier to enforce rules, as well as tools to augment resources (e.g., shareholder suits, whistleblowers) Improve enforcement • International Accounting Standards (IASB) • International Standards for Audit (IFAC) • International Organisation of Securities Commissions Principles Adopt International Standards and Practices • Institute training and codes of conduct • Tighten rules for “independent” directors and fiduciary duties for all directors • Promote director-accountability mechanisms (e.g., lawsuits, cumulative voting) Improve Board Performance • Strengthen ownership disclosure rules and enforcement • Explore categorical prohibitions on related-party transactions • Provide shareholders with private and collective rights of action Protect Minority Shareholders • Strengthen disclosure of ownership and financial interests • “Fit and proper” test for bank directors • Improve insolvency and creditor rights systems • Tighten regulatory oversight Improve Bank Governance