Download

1 / 29

290 likes | 307 Views

CORPORATE GOVERNANCE: THE OECD PRINCIPLES AND THEIR RELEVANCE TO SOUTHEAST EUROPE. 16 April 2003, Podgorica David.Robinett@OECD.org. Corporate Governance and its Relevance to SEE . OECD Principles for Corporate Governance SEE Corporate Governance Roundtable Future Work.

E N D

CORPORATE GOVERNANCE:THE OECD PRINCIPLES AND THEIR RELEVANCE TO SOUTHEAST EUROPE 16 April 2003, Podgorica David.Robinett@OECD.org

Corporate Governance and its Relevance to SEE • OECD Principles for Corporate Governance • SEE Corporate Governance Roundtable • Future Work

What is corporate governance? • The relationships between the managers, the board, the shareholders, and other stakeholders. • The structure for setting objectives and monitoring performance • Main responsibility lies with private sector • But governments shape legal and regulatory framework

Why should policy makers care? • Financial crises and recent corporate failures demonstrated the dangers of weak governance • Distorted governance structures lead to inefficient decision-making and misallocation of capital • Mobilisation of both domestic and international capital by corporations

Decision to Develop Core Principles • Governance systems vary widely • No single model of good corporate governance: but need for a global language • Detailed codes, best practices should be established at national and regional levels • The objective: to identify common elements or core principles underlying good corporate governance across the different systems: a multilateral policy framework

Intended Uses of the Principles • Primarily aimed at governments • Guidance also for stock exchanges, investors, corporations, commissions: • View primarily listed companies

I. Rights of Shareholders: Protection of shareholders’ rights and the capability of shareholders to influence behaviour of the corporation are pillars of good corporate governance • Secure ownership and registration, • Participation in basic decisions (pre-emption and appraisal), • general shareholder meetings: accountability procedures, in absentia voting, proxy rules: the IT impact • disclosure of capital and control structures: corporate groups and block-holders • fair and transparent transfers of control: transparency and fair treatment of all • Institutional voting: pointing to the trend

II. Equitable Treatment of Shareholders All shareholders - including foreign shareholders - should be treated fairly by controlling shareholders, boards and management • Insider trading prohibition: a cornerstone of market integrity in developed economies • Self -dealing and the disclosure of potential conflicting interests: the curse of emerging markets • Effective redress: the possibility to seek remedies in courts for all shareholder: a key implementation aspect • Ex ante transparency with respect to distribution of voting rights and ways voting rights exercised • Beneficial ownership and the role of custodians: OECD trends and ADR issue

III. The Role of Stakeholders • most stakeholders’ rights are protected by other laws (labour law, environmental law, etc.) • In some countries, the Board is also accountable to some stakeholders, particularly the employees (but not only) • The Principles are agnostic on formal stakeholder participation, • The Principles urge transparency, including to stakeholders • They urge incentives for stakeholder participation as a value enhancing mechanism driven by the corporations themselves: i.e. encourage firm specific- investment.

IV. Disclosure and Transparency A strong financial and non financial disclosure regime is the heart of corporate governance • Financial and operating results • Company objectives • Ownership and control structure • Board and executive information and recommendation • Foreseeable risk factors • Stakeholder information • Governance information • Independent audit and high quality dissemination channels

V. The Role of the Board The Board is the main mechanism for monitoring management and developing strategy • The key issue:independence from management • Target : non -executive participation (but “the boards should consider..”) with specific tasks: audit , remuneration, nomination • Act fairly with respect to various groups of shareholders, deal fairly with stakeholders, assure compliance with laws • Review strategy and planning, manage potential conflicts of interest, assure integrity of accounting, reporting and communications • Board members need to spend time and have good information

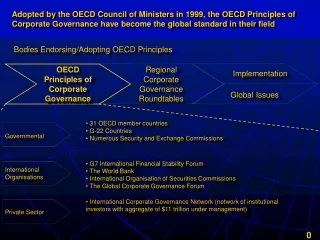

OECD Principles of Corporate Governance as a global benchmark for policy dialogue Governmental • 30 OECD member countries • Numerous Security and Exchange Commissions • G7 International Financial Stability Forum/principles • The World Bank/ROSC assessment • International Organisation of Securities Commissions • The Global Corporate Governance Forum International Organisations Private Sector • International Corporate Governance Network (network of institutional investors with aggregate of $11 trillion under management)

Promoting Reform • OECD-World Bank Co-operation, together with IFC, EU, bilateral donors such as the USAID and the government of Japan, as well as regional development banks • Regional Corporate Governance Roundtables for Russia, Asia, Latin America, Southeast European, Eurasian and African Roundtables are operational

SEE CG Roundtable • OECD / WORLD BANK corporate governance co-operation framework: Global Corporate Governance Forum • Stability Pact Investment Compact

The Global Corporate Governance Forum • The GCGF was officially launched in Monterrey, Mexico at the UN meeting on Finance for Development on April 20, 2002. • To support developing and emerging economies to promote corporate governance reform.

Who is GCGF? • Founders : WBG - OECD • Donors: Luxembourg, Netherlands,Norway, Sweden, Switzerland ,United Kingdom, United States • Staff: Secretariat & IFC support • Volunteers: Private Sector Advisory Group • Partners: CERES, ICFTU, TI, Commonwealth, etc

Objectives of the SEE Corporate Governance Roundtable Enhance CG in SEE • Assist policy design • Promote dialogue between public and private sectors • Assess and monitor CG trends • Identify needs for technical assistance

Policy Meetings • Agendas reflecting the main chapters of the OECD principles • Discussion of empirical studies and policy papers • Conclusions and recommendations • International expertise

Participants & Partners From SEE • Partners: securities commissions, self-regulatory and shareholders associations • Participants: officials and experts from securities commissions, stock exchanges, other securities markets institutions, corporate sector and stakeholders

Participants & Partners International Partners • OECD, WB, IFC, EU, USAID and other multilateral and bilateral institutions • WB/OECD Private Sector Advisory Group provides leaders and experts from the private sector

White Paper A basis for policy dialogue where the OECD and its SEE partners identify concrete steps for improving their corporate-governance framework • Identify gaps • Provide recommendations • Help focus reform efforts • Build consensus • Channel technical assistance

Examples of SEE White Paper Recommendations* White Papers on Corporate Governance OECD Principles of Corporate Governance Regional Corporate Governance Roundtables • Tighten the rules governing related-party transactions • Adopt international financial reporting standards Law reforms • Improve enforcement • Improve disclosure regulations Changes in Administrative Practice • Improve training of directors • Companies should communicate with employees and stakeholders Private Sector * Information on the SEE Roundtable is available on line at: www.oecd.org/daf/corporate-affairs

FUTURE OF THE ROUNDTABLES: Moving from awareness raising to policy design, implementation and enforcement of reform priorities • Russia, Eurasia, Asia, South-eastern Europe, Latin America Regions • Provide Regional policy-makers, regulators and practitioners with a forum for international dialogue on current corporate governance developments. Objective • Workshops on specific issues for exchange of experience and in-depth analysis • The topics should be tied to ongoing or planned initiatives. Format • Proceedings and conclusions from the workshops will provide both background analysis and options for viable policy solutions. • A review of corporate governance developments, with participation of OECD member countries. Outputs

Improving corporate governance remains a priority for OECD member countries • Need for policy response to issues arising after spectacular corporate scandals • Governments are being either (i) reactive to systemic weaknesses, (ii) pro-active to prevent failures, or (3) just realise that standards are rising. • Governments not only expect recovery from the depressed financial markets but improved growth and stability.

Review of the OECD Principles To remain relevant to new developments • 30 countries agree that the integrity of corporations, financial institutions and markets is essential to maintain confidence. • They agree to implement best practices, introduce incentives with a mix of regulation and self-regulation backed by enforcement • The OECD Steering Group on Corporate Governance will survey developments and assess the Principles by 2004

Priorities of the review Balance between regulation and incentives • Resist restricting entrepreneurial activity and competitiveness • Stay away from box-ticking and artificial compliance • Introduce strong principles-based element

For More Information www.oecd.org/daf/corporate-affairs www.gcgf.org www.worldbank.org/html/fpd/privatesector/cg

Conclusions • Assume there are no borders • Public and corporate governance go hand in hand