Download

1 / 12

130 likes | 274 Views

Jumps in High Volatility Environments and Extreme Value Theory. Abhinay Sawant March 4, 2009 Economics 201FS. Overview. Jumps in High Volatility Last Environment: Updated method from previous time

E N D

Jumps in High Volatility Environments and Extreme Value Theory Abhinay Sawant March 4, 2009 Economics 201FS

Overview • Jumps in High Volatility Last Environment: Updated method from previous time • Extreme Value Theory: Read current literature on topic but haven’t decided how to apply it to data

Set-Up of Test • Pre-Lehman Period: All data through September 12, 2008 • Post-Lehman Period: September 15, 2008 – January 4, 2009 (78 days) • Difference of Sample Means t Test: • Assumption: t distribution is approximately normal for high sample size

Jumps in High Volatility Environments • Regression of Realized Volatility on Z-Scores • Comparisons across Industries

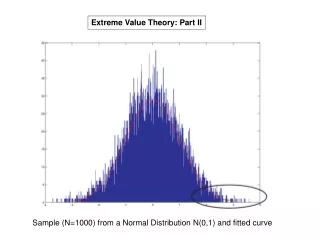

Extreme Value Theory: Background Theory • General Pareto Distribution (GPD) describes values of x above the threshold u: • ξ and β are to be estimated using Maximum Likelihood Estimation • Hill’s Estimator:

Extreme Value Theory: Background Theory • Extreme Value Theory allows for the estimation of risk metrics:

Extreme Value Theory: Current Literature • High-frequency tail estimation has efficiency benefits since intraday data allows for observable extremes (Cotter and Longin, 2004) • Margin setting based on closing prices alone underestimates the risk, when compared with intraday data (Cotter and Longin, 2004) • High-frequency volatility estimator based on EVT provides superior forecasting abilities when compared to GARCH discrete time models (Bali and Weinbaum, 2006)

Further Direction • Does the financial crisis period offer extreme values of returns and can GPD model adequately estimate these values of returns? • At high frequency, do the extreme intraday returns represent jumps or rapid movement in prices?