Download

1 / 10

130 likes | 385 Views

COST OF CAPITAL CHAPTER 10. Weighted Average Cost of Capital Cost of Capital Components. Types of Capital. SOURCES OF LONG-TERM CAPITAL . From Most to Least Used Sources Retained Earnings Sale of Corporate Bonds Sale of Common Stock Sale of Preferred Stock

E N D

COST OF CAPITALCHAPTER 10 Weighted Average Cost of Capital Cost of Capital Components

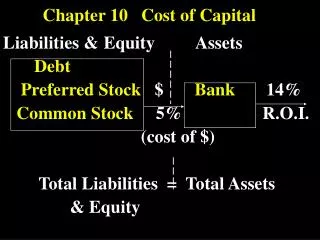

SOURCES OF LONG-TERM CAPITAL • From Most to Least Used Sources • Retained Earnings • Sale of Corporate Bonds • Sale of Common Stock • Sale of Preferred Stock • Cost of capital determined by firm's capital structure (RHS of B/S). Capital consists of: • Debt (bonds) • Equity (preferred and common stocks) • Retained Earnings

SOURCES OF LONG-TERM CAPITAL • Market-based weighted-average of these costs (WACC) is also termed the hurdle rate. WACC = Wd Kd (1-t) + Wp Kp + We Ke • How are the weights Wi determined? • Use accounting numbers (easiest – uses book values) • Use market value of issued securities (preferred method) • Firm’s cost of capital is set by market forces via investor pricing activity [implied risk assessment] • High risk: lower prices (low P/E ratios) • Low risk: higher prices (high P/E ratios)

HURDLE RATE [WACC or ka] • Some Observations: • Approximately 80% of all investment projects are financed internally (from retained earnings and tax-shielded cash flows such as depreciation). • Approximately 15% are financed by selling debt. • Approximately 5% are financed by selling stock.

COST OF NEW CAPITAL • The Cost of New Debt: Kd • Kd = [YTM / (1 - F)] (1 - T) • Where: • YTM = current market yields to maturity for seasoned bonds. • F = flotation costs as a decimal (percentage). • T = the marginal tax rate of the firm

COST OF NEW CAPITAL B. The cost of Preferred Stock; Kpfd • Kpfd = Dpfd / [Ppfd * (1 - F)] • Where: • Dp = the dividend (to be) paid on the preferred stock. • Pp = the (current) market price of preferred. • F = Flotation costs as a percentage.

COST OF NEW CAPITAL C. Cost of Equity (common & ret’d earns); Ke Ke = D1 / (Po - F) + g • Where: • D1 = the expected dividend at the end of year 1. • Po = the current price of common. • F = Flotation cost in dollars per share. • g = the anticipated rate of growth in dividends.

HURDLE RATE [WACC or ka] • Hurdle rate; minimum rate of return a project must earn. Ceteris paribus…. • If just the hurdle rate is earned, then value of firm is maintained. • If less that the hurdle rate is earned, then value of firm declines. • If more that the hurdle rate is earned, then value of firm increases.

HOMEWORK CHAPTER 10 • Questions You Should Be Able To Answer • Why is the hurdle rate an important concept in capital budgeting? • What important considerations must we make when computing the cost of capital? • What factors should managers consider when planning a capital structure strategy? • Homework Assignment • Self-test: ST-1, parts b, e, f • Questions: 10-1, parts a, b, h, i • Problems: 10-1, 10-3, 10-11