Download

1 / 31

350 likes | 478 Views

CHAPTER 10 The Cost of Capital. Sources of capital Component costs WACC Adjusting for flotation costs. What sources of long-term capital do firms use?. Calculating the weighted average cost of capital. WACC = w d r d (1-T) + w p r p + w c r s

E N D

CHAPTER 10The Cost of Capital Sources of capital Component costs WACC Adjusting for flotation costs

Calculating the weighted average cost of capital WACC = wdrd(1-T) + wprp + wcrs • The w’s refer to the firm’s capital structure weights. • The r’s refer to the cost of each component.

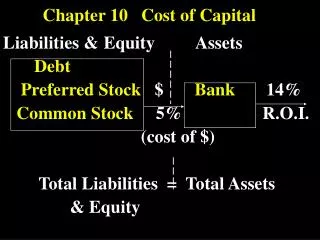

The Weighted Average Cost of Capital WACC = wdrd(1-T) + wprp + wcrs • Capital Structure Weights The weights in the above equation are intended to represent a specific financing mix (where wi = % of debt, wp = % of preferred, and ws= % of common). Specifically, these weights are the target percentages of debt and equity that will minimize the firm’s overall cost of Using or raising new funds.

Firm Capital Structure Weight • Assume the capital structure weight of the firm is 30% debt, 10% preferred stock and 60% equity • WACC = 0.3rdd(1-T) + 0.1rp + 0.6rs

Component cost of debt WACC = wdrd(1-T) + wprp + wcrs • rd is the cost of debt capital. • The yield to maturity on outstanding L-T debt is often used as a measure of rd.

Borrowing firm Cost of debt (rd) = Yield to maturity Coupon interest Par value “Tax deductible” - Partially subsidized rd (1-T)

A 15-year, 12% semiannual coupon bond sells for $1,153.72. What is the cost of debt (rd)? • The bond pays a semiannual coupon, so rd = 5.0% x 2 = 10%. INPUTS 30 I/YR -1153.72 60 1000 OUTPUT N 5 PV PMT FV

Component cost of debt • Why tax-adjust, i.e. why rd(1-T)? WACC = wdrd(1-T) + wprp + wcrs • Interest is tax deductible • Assume Corp tax is 40% • Interest is tax deductible, so A-T rd = B-T rd (1-T) = 10% (1 - 0.40) = 6%

Borrowing firm Cost of debt (rd)=6% = Yield to maturity = 10% Coupon interest Par value “Tax deductible” - Partially subsidized rd (1-T) = 10% (1 - 0.40) = 6%

Component cost of preferred stock WACC = wdrd(1-T) + wprp + wcrs • rp is the cost of preferred stock, which is the return investors require on a firm’s preferred stock. • Preferred dividends are not tax-deductible, so no tax adjustments necessary. Just use nominal rp.

What is the cost of preferred stock? • The cost of preferred stock can be solved by using this formula: rp = Dp / Pp = $10 / $111.10 = 9%

Is preferred stock more or less risky to borrowing firm? • More risky; although the firm has the option not to pay preferred dividend under certain circumstances. • However, under company law, if preferred dividend is not paid (1) firm cannot pay common dividend, & (2) difficult to raise additional external funds.

Component cost of equity WACC = wdrd(1-T) + wprp + wcrs • rs is the cost of common equity using retained earnings.

Why is there a cost for retained earnings? • Earnings can be reinvested or paid out as dividends. • Investors could buy other securities, earn a higher return. • If earnings are retained, there is an opportunity cost (the return that stockholders could earn on alternative investments).

To determine the cost of common equity, rs • CAPM: rs = rRF + (rM – rRF) b

If the rRF = 7%, rM = 13%, and the firm’s beta is 1.2, what’s the cost of common equity based upon the CAPM? rs = rRF + (rM – rRF) b = 7.0% + (6.0%)1.2 = 14.2% ~14%

Cost of issuing new common stock? • When a company issues new common stock they also have to pay flotation costs to the underwriter.

Cost of issuing new common stock WACC = wdrd(1-T) + wprp + wcre re is the cost of common equity of issuing new common stock

If issuing new common stock incurs a flotation cost of 15% of the proceeds, what is re? ≈ Flotation cost factor

Flotation costs • Flotation costs are highest for common equity. However, since most firms issue equity infrequently, • We will frequently ignore flotation costs when calculating the WACC.

Ignoring flotation costs, what is the firm’s WACC? WACC = wdrd(1-T) + wprp + wcrs = 0.3(10%)(0.6) + 0.1(9%) + 0.6(14%) = 1.8% + 0.9% + 8.4% = 11.1%

The Marginal Cost & Investment Decisions The Weighted Marginal Cost of Capital (WMCC) The WACC typically increases as the volume of new capital raised within a given period increases. This is true because companies need to raise the return to investors in order to entice them to invest more in the company ( ie. to compensate them for the increased risk introduced by larger volumes of capital raised.

The Marginal Cost & Investment Decisions WMCC 11.76% 11.75% 11.66% 11.50% 11.25% 11.13% Total Financing (millions) $2.5 $4.0

The Marginal Cost & Investment Decisions • The Weighted Marginal Cost of Capital (WMCC) • In addition, the cost will eventually increase when the firm runs out of cheaper retained equity and is forced to raise new, more expensive equity capital.

The Weighted Average Cost of Capital WACC = ka = wiki + wpkp + wskr or n • Capital Structure Weights For example, assume the market value of the firm’s debt is $40 million, the market value of the firm’s preferred stock is $10 million, and the market value of the firm’s equity is $50 million. Dividing each component by the total of $100 million gives us market value weights of 40% debt, 10% preferred, and 50% common.

The Marginal Cost & Investment Decisions (cont.) • The Weighted Marginal Cost of Capital (WMCC) • Finding Break Points Finding the break points in the WMCC schedule will allow us to determine at what level of new financing the WACC will increase due to the factors listed above. BPj = AFj/wj where: BPj = breaking point form financing source j AFj = amount of funds available at a given cost wj = target capital structure weight for source j

The Marginal Cost & Investment Decisions (cont.) • The Weighted Marginal Cost of Capital (WMCC) • Finding Break Points Assume that the firm has $2 million of retained earnings available. When it is exhausted, the firm must issue new (more expensive) equity. Furthermore, the company believes it can raise $1 million of cheap debt after which it will cost 7% (after-tax) to raise additional debt. Given this information, the firm can determine its break points as follows:

The Marginal Cost & Investment Decisions (cont.) • The Weighted Marginal Cost of Capital (WMCC) • Finding Break Points BPequity = $2,000,000/.50 = $4,000,000 BPdebt = $1,000,000/.40 = $2,500,000 This implies that the firm can fund up to $4 million of new investment before it is forced to issue new equity and $2.5 million of new investment before it is forced to raise more expensive debt. Given this information, we may calculate the WMCC as follows:

WMCC 11.76% 11.75% 11.66% 11.50% 11.25% 11.13% Total Financing (millions) $2.5 $4.0 The Marginal Cost & Investment Decisions (cont.) New Equity was issued New Debt was issued