Download

1 / 16

160 likes | 165 Views

This article explains how to calculate and account for notes receivable, provides examples of accounting entries, and discusses the analysis of accounts receivable turnover.

E N D

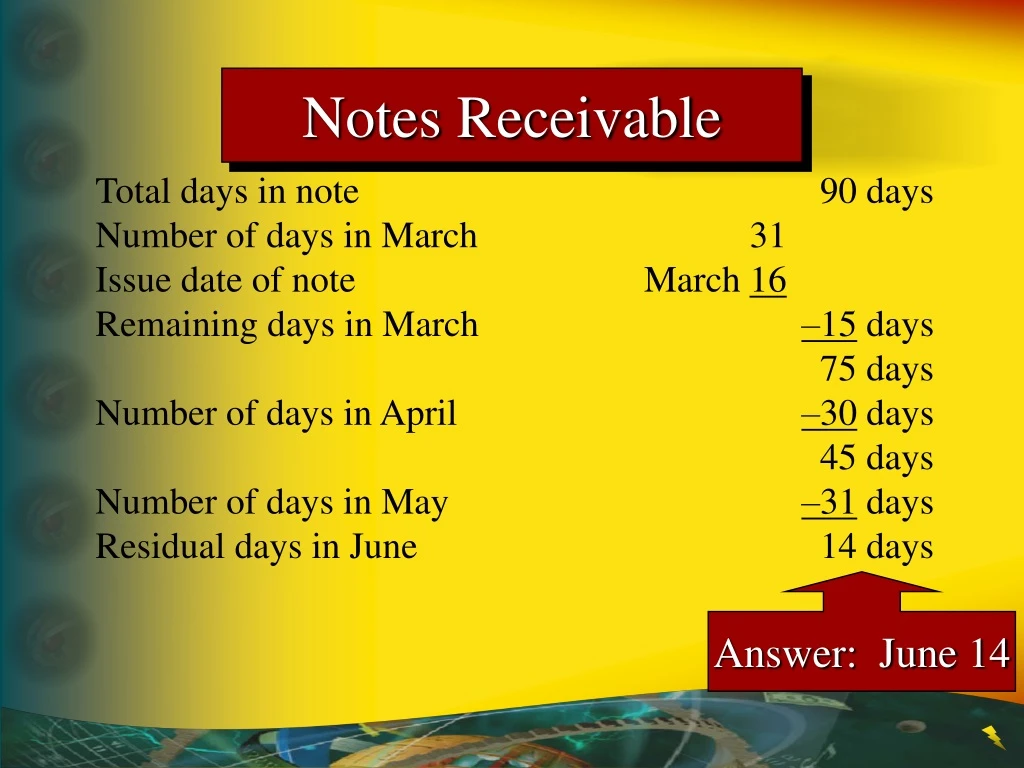

Notes Receivable Total days in note 90 days Number of days in March 31 Issue date of note March 16 Remaining days in March –15 days 75 days Number of days in April –30 days 45 days Number of days in May –31 days Residual days in June 14 days Answer: June 14

Notes Receivable The amount that is due at the maturity or due date is called the maturity value.

Notes Receivable Received a $6,000, 12%, 30-day note dated November 21, 2006 in settlement of the account of W. A Bunn Co.

Principal + Interest = Maturity Value $6,000 + $60.00 = $6,060.00 Notes Receivable Interest Calculation Principal x Rate x Time = Interest $6,000 x 12% x 30/360 = $60.00 Maturity Value Calculation

Accounting for Notes Receivable Nov. 21 Notes Receivable 6 000 00 Sales 6 000 00 Received 30-day, 12% note dated November 21, 2006. A $6,000 30-day, 12% note dated November 21 is received from W. A Bunn Company in exchange for merchandise.

Accounting for Notes Receivable Dec. 21 Cash 6 060 00 Notes Receivable 6 000 00 Interest Revenue 60 00 Received principal and interest on matured note. On December 21, when the note matures, the firm receives $6060 from W. A. Bunn Company ($6,000 plus $60 interest).

Accounting for Notes Receivable Dec. 21 Accounts Receivable—Bunn Co. 6 060 00 Notes Receivable 6 000 00 Interest Revenue 60 00 To record dishonored note and interest. If W. A. Bunn Company fails to pay the note on the due date, it is considered a dishonored note receivable. The note and interest are transferred to the customer’s account.

Accounting for Notes Receivable Dec. 1 Notes Receivable 4 000 00 Accounts Receivable—Crawford Company 4 000 00 Received note in settlement of account. A 90-day, 12% note dated December 1, 2006, is received from Crawford Company to settle its account, which has a balance of $4,000.

Accounting for Notes Receivable Dec. 31 Interest Receivable 40 00 Interest Revenue 40 00 Adjusting entry for accrued interest. Assuming that the accounting period ends on December 31, an adjusting entry is required to record the accrued interest of $40 ($4,000 x 0.12 x 30/360).

Accounting for Notes Receivable Mar. 1 Cash 4 120 00 Notes Receivable 4 000 00 Interest Receivable 40 00 Interest Revenue 80 00 $4,000 x 0.12 x 60/360 Received payment on note and interest. On March 1, 2004, $4,120 is received for the note ($4,000) and interest ($120).

Crabtree Co. Balance SheetDecember 31, 2006 Assets Current assets: Cash $119,500 Notes receivable 250,000 Accounts receivable $445,000 Less allowance for doubtful accounts 15,000 430,000 Interest receivable 14,500 Merchandise inventory 714,000 Highlighted items are receivables

Net sales Average accounts receivable Financial Analysis and Interpretation Accounts Receivable Turnover

$36,000,000 $1,150,000 $32,500,000 $1,115,000 Accounts Receivable Turnover 2006 2005 Net sales on account $36,000,000 $32,500,000 Accounts receivable (net): Beginning of year $ 1,080,000 $1,050,000 End of year 1,220,000 1,080,000 Total $2,300,000 $2,130,000 Average $1,150,000 $1,115,000 Accounts receivable turnover 31.3 times 29.1 times Use: To assess the efficiency in collecting receivables and in the management of credit.

Accounts receivable, end of year Average daily sales on account =12.4 days $1,220,000 ($36,000,000 ÷ 365 days) Accounts receivable, end of year Average daily sales Number of Days’ Sales in Receivables Use: To assess the efficiency in collecting receivables and in the management of credit.

Chapter 8 The End