Download

1 / 26

280 likes | 602 Views

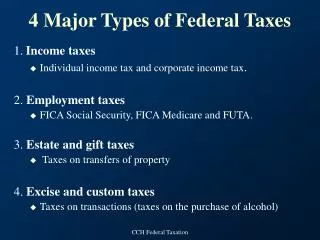

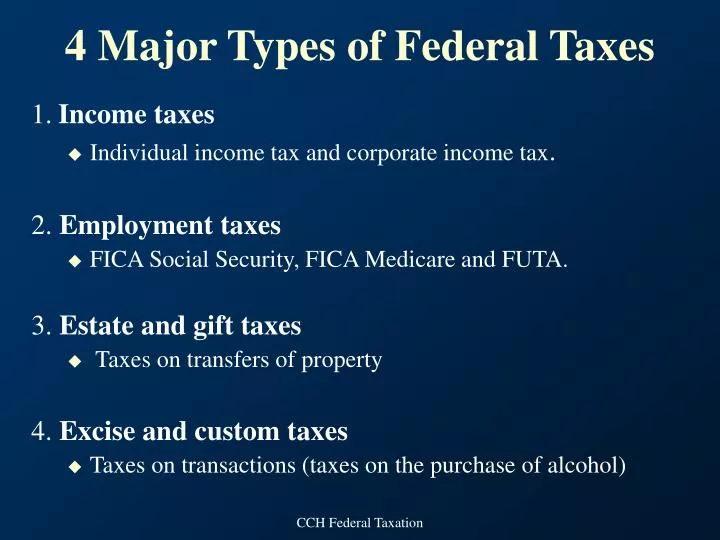

4 Major Types of Federal Taxes. 1. Income taxes Individual income tax and corporate income tax . 2. Employment taxes FICA Social Security, FICA Medicare and FUTA. 3. Estate and gift taxes Taxes on transfers of property 4. Excise and custom taxes

E N D

4 Major Types of Federal Taxes 1. Income taxes • Individual income tax and corporate income tax. 2. Employment taxes • FICA Social Security, FICA Medicare and FUTA. 3. Estate and gift taxes • Taxes on transfers of property 4. Excise and custom taxes • Taxes on transactions (taxes on the purchase of alcohol) CCH Federal Taxation

Tax Avoidance v. Tax Evasion • Tax avoidance—Saving tax dollars through specific actions to avoid the tax liability prior to the time it would have occurred according to the law. • Tax evasion—The taxpayer does not properly report income and expenses even though the taxpayer already has a tax liability and all actions are definitely complete. CCH Federal Taxation

Tax Avoidance v. Tax Evasion What frequently distinguishes avoidance from evasion is the intent of the taxpayer. Some indications of taxpayer fraud are: • Understatement of income • Claiming of fictitious or improper deductions • Accounting irregularities • Allocation of income • Acts and conduct of the taxpayer CCH Federal Taxation

Tax Legislative Process 1. The Constitution requires that all revenue legislation start in the House Ways and Means Committee. 2. The tax bill is sent to the House of Representatives for approval. • The House debates the bill under a “closed rule” procedure (all amendments must be approved by the House Ways and Means Committee). 3. If approved by the House of Representatives, the bill is sent to the Senate Finance Committee. • The Finance Committee may make amendments to the House bill. Exhibit 1 page 1-18 CCH Federal Taxation

Tax Legislative Process Cont… 4. The bill is sent to the Senate for approval. • Any senator may offer amendments from the floor of the Senate. • Bill may be sent to a Joint Conference Committee if the House and Senate differ. The bill would then be sent back to House and Senate for consideration. At this point, no further amendments can be made. 5. Approved or vetoed by the President 6. Incorporated into the Code if approved by President or if veto is overridden. Exhibit 1 page 1-18 CCH Federal Taxation

Classification of Materials • Primary or “authoritative” • Internal Revenue Code (statutory authority) • Treasury Regulations (administrative authority) • Internal Revenue Service Rulings (administrative authority) • Judicial Authority • Secondary or “reference” • Looseleaf tax reference services • Periodicals • Textbooks • Treatises • Published papers from tax institutes • Symposia • Newsletters CCH Federal Taxation Chapter 2, Exhibit 1

Judicial Authority The three courts of original jurisdiction are: • U.S. Tax Court • U.S. District Court • U.S. Court of Federal Claims CCH Federal Taxation Chapter 2, Exhibit 2a

Judicial Authority The appellate courts are: • U.S. Circuit Courts of Appeals • U.S. Court of Appeals for the Federal Circuit • U.S. Supreme Court CCH Federal Taxation Chapter 2, Exhibit 2b

Five-Step Research Method CCH Federal Taxation Chapter 2, Exhibit 3

Research Sources for Legislative Authority CCH Federal Taxation Chapter 2, Exhibit 4a

Research Sources for Legislative Authority CCH Federal Taxation Chapter 2, Exhibit 4b

Research Sources for Legislative Authority CCH Federal Taxation Chapter 2, Exhibit 4c

Research Sources for Administrative Authority CCH Federal Taxation Chapter 2, Exhibit 5a

Research Sources for Administrative Authority CCH Federal Taxation Chapter 2, Exhibit 5b

Research Sources for Administrative Authority CCH Federal Taxation Chapter 2, Exhibit 5c

Research Sources for Judicial Authority CCH Federal Taxation Chapter 2, Exhibit 6a

Authority Research Source Binding Persuasive U.S. Court of Appeal decisions(hears appeals from any of the three lower courts; the Federal Circuit Appellate Court hears all appeals from the Court of Federal Claims) • USTC (CCH) • AFTR (RIA) • Federal 3d (West) (binding to lower courts in same circuit) U.S. Tax Court decisions – regular (deals with novel issues not previously resolved by TC; advance payment of tax not allowed) • CCH services • RIA services • U.S. Government Printing Office (binding to other tax courts in same circuit) Research Sources for Judicial Authority CCH Federal Taxation Chapter 2, Exhibit 6b

Authority Research Source Binding Persuasive U.S. Tax Court decisions— Memorandum (deals with factual issues necessitating application of established principles of tax law; advance payment of tax not allowed) • TCM (CCH) • T.C. Memo (RIA) (binding to other tax courts in same circuit) Small Cases Division of Tax Court (informal hearing for disputes of $50,000 or less; appeals process not available) Not published No precedent authority Research Sources for Judicial Authority CCH Federal Taxation Chapter 2, Exhibit 6c

Research Sources for Judicial Authority CCH Federal Taxation Chapter 2, Exhibit 6d

Commercial Publishers of Comprehensive Services CCH Federal Taxation Chapter 2, Exhibit 7a

Commercial Publishers of Comprehensive Services CCH Federal Taxation Chapter 2, Exhibit 7b

Commercial Publishers of Comprehensive Services CCH Federal Taxation Chapter 2, Exhibit 7c

Commercial Publishers of Judicial Decisions CCH Federal Taxation Chapter 2, Exhibit 8a

Commercial Publishers of Judicial Decisions CCH Federal Taxation Chapter 2, Exhibit 8b

Commercial Publishers of Judicial Decisions CCH Federal Taxation Chapter 2, Exhibit 8c

Delinquency penalties Accuracy-related and fraud penalties Negligence penalty Substantial understatement of tax liability Substantial valuation misstatement penalty Substantial overstatement of pension liabilities Estate of gift tax valuation understatements Penalty for aiding understatement of tax liability Civil fraud penalty Criminal fraud penalty Estimated taxes and underpayment penalties Failure to make deposits of taxes Tax preparer penalties Penalties CCH Federal Taxation Chapter 2, Exhibit 16