Download

1 / 19

200 likes | 363 Views

Building Good Credit & Improving Your Credit Score. Some statistics to consider. Average credit card debt per household - $15,788 (May 2010) College loans alone now total almost $830 billion (said another way, $830,000,000,000!) Credit card penalties estimated at $20.5 billion in 2009

E N D

Some statistics to consider Average credit card debt per household - $15,788 (May 2010) College loans alone now total almost $830 billion (said another way, $830,000,000,000!) Credit card penalties estimated at $20.5 billion in 2009 National default rate on credit cards almost 28 percent Home foreclosure rate worse since Great Depression eSlide - P4065 - LifeCare

Objectives What is credit and why do we need it? Understand how to use debt Discuss your credit report Understand your credit score Improving your credit score Managing your cash flow better eSlide - P4065 - LifeCare

What is credit and why do we need it? Allows us to make purchases that we cannot afford today Used by governments and businesses Used by individuals our credit worthiness determines our cost and access to credit could impact ability to rent housing, get insurance, or even being hired eSlide - P4065 - LifeCare

Understanding how to use credit Good debt low interest rates manageable payments long term benefits (examples: home, education, car) • Bad debt • high interest rates (typically unsecured) • doesn’t fit into your budget • short-term benefits/long pay off period! consider the repayment period posted on your credit card statement eSlide - P4065 - LifeCare

So should you use debt? Ask yourself how long it will take you to pay off the amount you borrow with the interest charges added Ask yourself whether this spending provides a long-term benefit or a short-term benefit If you expect a benefit, what is the return eSlide - P4065 - LifeCare

Your credit report Late payments Outstanding debt Total amount of credit currently available to you Personal judgments, bankruptcies, liens eSlide - P4065 - LifeCare

The Power of Your Credit Reports and Score Will determine if you will get a loan Will determine what interest rate you will pay Can determine if you can rent an apartment or house Can impact your job prospects Can impact insurance rates eSlide - P4065 - LifeCare

How is a Credit Score Graded? eSlide - P4065 - LifeCare

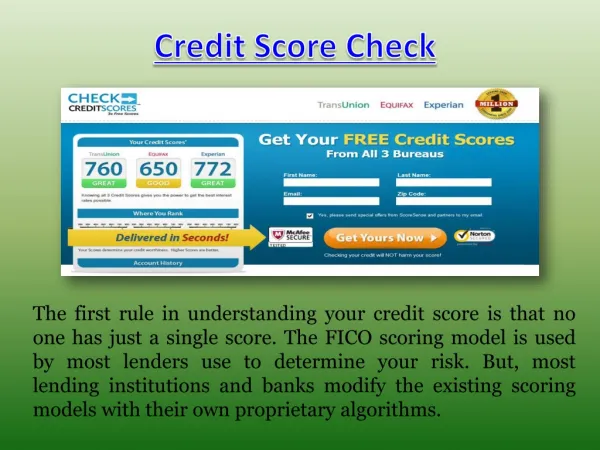

Improving Your Credit Score Experian, TransUnion, and Equifax will provide a copy of your credit report for free (1 per year) www.experian.comwww.transunion.comwww.equifax.com Stagger your requests (1 company report every 4 months) Review all entries for errors Contact both credit bureau and company providing the incorrect information ASAP in writing Explain that you are disputing the information provided to the bureau. Provide supporting documentation (cancelled checks) Your dispute may not get immediate results Have a statement of your dispute included on your current credit report Request a new report showing your disputed statement for any inquiries into your credit report provided within the last 6 months eSlide - P4065 - LifeCare

Make Smart Moves! Pay on Time! Get current and stay current Keep your balances below 30% of your credit limit Pay down debt Keep old credit relationships Contact your creditor first Be prepared Suggest a payment plan you can handle Send letter to creditor detailing agreement Enclose copy of letter with each payment Improving Your Credit Score (con’t) eSlide - P4065 - LifeCare

Working with Collection Agencies Know your rights! (Fair Debt Collection Practices Act) Small possibility to negotiate with the collection agency to remove account from credit report If agreed upon, document this fact in Settlement Offer sent to collection agency Make payment after offer accepted eSlide - P4065 - LifeCare

Credit Counseling Agencies and Debt Management Programs (DMPs) • DMPs are available through credit counseling agencies. • Can help with budgeting • Can negotiate plans with creditors • You pay CC with one check, they pay creditors • Keeps you organized, current, out of bankruptcy eSlide - P4065 - LifeCare

Credit Counseling Agencies Buyer Beware! US Federal Trade Commission www.ftc.gov/org US Federal Trade Commission www.ftc.gov/credit National Federation for Credit Counseling www.nfcc.org eSlide - P4065 - LifeCare

Rebuilding Credit Use secured credit cards Consider store cards Use cards, but keep spending low Pay on time! Be patient! This could take time - Chapter 7 (10 years) Chapter 13 (7 – 10 years) - Late payments 2 years - settlements/repos/foreclosures (7 years) eSlide - P4065 - LifeCare

Managing Cash Flow Work on your budget! Identify “problem” spending areas Plug the spending holes! Re-direct money towards paying down your debt Set up equal payments plans Use on-line payment options eSlide - P4065 - LifeCare

Building Good Credit and Improving Your Credit Score Wrap up eSlide - P4065 - LifeCare

Additional Resources www.ftc.gov/credit www.nfcc.org www.annualcreditreport.com LifeCare 800-873-4636 www.lifecare.com eSlide - P4065 - LifeCare