Download

1 / 16

160 likes | 330 Views

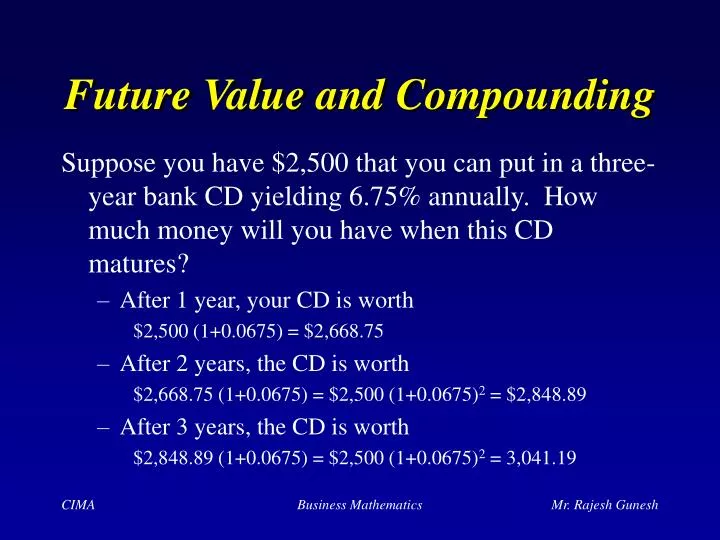

Future Value and Compounding. Suppose you have $2,500 that you can put in a three-year bank CD yielding 6.75% annually. How much money will you have when this CD matures?. After 1 year, your CD is worth $2,500 (1+0.0675) = $2,668.75 After 2 years, the CD is worth

E N D

Future Value and Compounding Suppose you have $2,500 that you can put in a three-year bank CD yielding 6.75% annually. How much money will you have when this CD matures? • After 1 year, your CD is worth $2,500 (1+0.0675) = $2,668.75 • After 2 years, the CD is worth $2,668.75 (1+0.0675) = $2,500 (1+0.0675)2 = $2,848.89 • After 3 years, the CD is worth $2,848.89 (1+0.0675) = $2,500 (1+0.0675)2 = 3,041.19 Business Mathematics

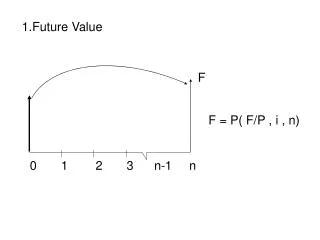

Future Value and Compounding More generally, FV = PV (1+i)n , where FV = the future value of a lump sum PV = the initial principal, or present value of the lump sum i = the annual interest rate n = the number of years interest compounds Business Mathematics

3 0 1 2 FV = 2500 (1.0675)3 = 3041.19 Future Value and Compounding A good way of understanding this process is through the use of a time line: i = 6.75% PV = –2500 Business Mathematics

Future Value and Compounding How much would this CD be worth at maturity if interest compounds quarterly? • The trick is to convert the interest rate into a periodic rate and compound each period, rather than annually. FV = PV (1+i/m)nm , where m is the number of periods per year. • FV = $2,500(1+0.0675/4)34 = $3,055.98. Business Mathematics

3 0 1 2 Present Value and Discounting Suppose you will receive $5,000 three years from now. If you can earn 4.5% on your savings, how much is this worth to you today? i = 4.5% PV = ? FV = 5000 $5,000 = PV (1+0.045)3 PV = $5,000 / (1+0.045)3 = $4,381.48 Business Mathematics

Present Value and Discounting More generally, PV = FV / (1+i)n , where FV = the future value of a lump sum PV = the initial principal, or present value of the lump sum i = the annual discount rate n = the number of years Business Mathematics

Present Value and Discounting If discounting occurs at a frequency other than annually: PV = FV / (1+i/m)nm , where m = the number of discounting periods per year Business Mathematics

3 0 1 2 i PV = ? PMT PMT PMT FV = ? Annuities An annuity is a series of payments or receipts made at regular intervals for a determined period of time Business Mathematics

3 0 1 2 100 100 100 + 100(1.09) = 109.00 + 100(1.09)2 = 118.81 327.81 Future Value of an Annuity If you will receive $100 at the end of each of the next 3 years and can invest it at 9%, how much will it be worth at the end of the 3 years? 9% = 100.00 Business Mathematics

Future Value of an Annuity More generally, FV = PMT + PMT(1+i) + PMT(1+i)2 + PMT(1+i)3 + … + PMT(1+i)n–1 n–1 = PMT (1+i)n–t–1 t=0 = PMT [(1+i)n – 1] / i Business Mathematics

Future Value of an Annuity If compounding occurs at a frequency other than annually, FV = PMT [(1+i/m)nm – 1] / (i/m) Business Mathematics

9% 3 0 1 2 100 100 100 91.74 = 100 / (1.09) 84.17 = 100 / (1.09)2 77.22 = 100 / (1.09)3 253.13 Present Value of an Annuity How much is this $100, 3-year annuity worth today, assuming a 9% discount rate? Business Mathematics

Present Value of an Annuity More generally, PV = PMT / (1+i) + PMT / (1+i)2 + PMT / (1+i)3 + … + PMT / (1+i)n n = PMT 1 / (1+i)t t=1 = PMT [1 – 1 / (1+i)n] / i Business Mathematics

Present Value of an Annuity If compounding occurs at a frequency other than monthly, PMT [1 – 1 / (1+i/m)nm] / (i/m) Business Mathematics

Effective Annual Rates Which provides the highest total return, a savings account that pay 5.00% compounded annually or one that pays 4.75% compounded monthly? • One way to answer this is to calculate the future value of $100 invested in each • PV1 = $100 (1.05) = $105.00 • PV2 = $100 (1+0.0475/12)12 = $104.85 Business Mathematics

Effective Annual Rates Alternatively, you can calculate the effective annual rate associated with each account EAR = (1 + i/m)m – 1 • EAR1 = (1 + 0.05/1)1 – 1 = 0.0500 = 5.00% • EAR2 = (1 + 0.0475/12)12 – 1 = 0.0486 = 4.86% Effective annual rates are directly comparable in terms of total yield Business Mathematics