Download

1 / 15

E N D

Want to be a millionaire? No problem! Suppose you are currently 21 years old, and can earn 10 percent on your money (about what the typical common stock has averaged over the last six decades - but more on that later). How much must you invest today in order to accumulate $1 million by the time you reach age 65?

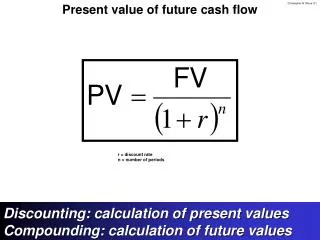

We first define the variables: FV = $1 million r = 10 percent t = 65 - 21 = 44 years PV = ? Set this up as a future value equation and solve for the present value: $1 million = PV x (1.10)44 PV = $1 million/(1.10)44 = $15,091.

Q. Suppose you need $20,000 in three years to pay your college tuition. If you can earn 8% on your money, how much do you need today? A. Here we know the future value is $20,000, the rate (8%), and the number of periods (3). PV = $20,000/(1.08)3 = 15,876.54 = 15,876.64

Annuity Present Value Suppose you need $20,000 each year for the next three years to make your tuition payments. Assume you need the first $20,000 in exactly one year. Suppose you can place your money in a savings account yielding 8% compounded annually. How much do you need to have in the account today? (Note: Ignore taxes, and keep in mind that you don’t want any funds to be left in the account after the third withdrawal, nor do you want to run short of money.)

Annuity Present Value - Solution Here we know the periodic cash flows are $20,000 each. Using the most basic approach: PV = $20,000/1.08 + $20,000/1.082 + $20,000/1.083 = $18,518.52 + $_______ + $15,876.65 = $51,541.94 Here’s a shortcut method for solving the problem using the annuity present value factor: PV = = $20,000 x 2.577097 = $51,541.94

Future Value for a Lump Sum Q. Deposit $5,000 today in an account paying 12%. How much will you have in 6 years? A. Multiply the $5000 by the future value interest factor: $5000 (1 + r)t = $5000 1.9738227 = $9869.1135

In 1934, the first edition of a book described by many as the “bible” of financial statement analysis was published. Security Analysis has proven so popular among financial analysts that it has never been out of print. According to an item in The Wall Street Journal, a copy of the first edition was sold by a rare book dealer in 1996 for $7,500. The original price of the first edition was $3.37. What is the annually compounded rate of increase in the value of the book?

Set this up as a future value (FV) problem. Future value = $7,500 Present value = $3.37 t = 1996 - 1934 = 62 years FV = PV x (1 + r)t so, $7,500 = $3.37 x (1 + r)62 (1 + r)62 = $7,500/3.37 = 2,225.52 Solve for r: r = (2,225.52)1/62 - 1 = .1324 = 13.24%

Suppose you deposit $5000 today in an account paying r percent per year. If you will get $10,000 in 10 years, what rate of return are you being offered? Set this up as present value equation: FV = $10,000 PV = $ 5,000 t = 10 years PV = FVt/(1 + r)t $5000 = $10,000/(1 + r)10 Now solve for r: (1 + r)10 = $10,000/$5,000 = 2.00 r = (2.00)1/10 - 1 = .0718 = 7.18 percent

Assume the total cost of a college education will be $75,000 when your child enters college in 18 years. You have $7,000 to invest. What rate of interest must you earn on your investment to cover the cost of your child’s education? Solution: Set this up as a future value problem. $75,000 = $7,000 x FVIF(r,18) FVIF(r,18) = $75,000 / $7,000 = 10.714 (1 + r)18 = 10.714 Take the 18th root of both sides: 1 + r = 10.7141/18 = 10.714.05555 = 1.14083 r = 1.14083 - 1 = .14083 = 14.083%. So, you must earn at least 14.083% annually to accumulate enough for college. If not, you’ll come up short.

Q. You want to buy a Mazda Miata to go cruising. It costs $17,000. With a 10% down payment, the bank will loan you the rest at 12% per year (1% per month) for 40 months. What will your payment be? C = $15,300/32.83469 C = $ 465.97

Suppose that a 25-year old could accumulate $1 million by age 65 by investing $22,095 today and letting it earn interest (at 10%compounded annually) for 40 years. Now, rather than plunking down $22,095 in one chunk, suppose she would rather invest smaller amounts annually to accumulate the million. If the first deposit is made in one year, and deposits will continue through age 65, how large must they be? Set this up as a FV problem: C = $1,000,000/442.59256 = $2,259.41 Becoming a millionaire just got easier!

In the previous example we found that, if one begins saving at age 25, accumulating $1 million by age 65 requires saving only $2,259.41 per year. Unfortunately, most people don’t start saving for retirement that early in life. (Many don’t start at all!) Suppose Bill just turned 40 and has decided it’s time to get serious about saving. Assuming that he wishes to accumulate $1 million by age 65, he can earn 10% compounded annually, and will begin making equal annual deposits in one year, how much must each deposit be?

Set this up as a FV problem: r = 10% t = 65 - 40 = 25 FV = $1,000,000 Then: C = $1,000,000/98.3471 = $10,168.07 • Moral of the story: Putting off saving for retirement makes it a lot more difficult!