Download

1 / 36

370 likes | 551 Views

Session II Regulatory Capital and Solvency Standards. Dr. Peter Kandl April 2, 2007. Objectives. To give an overview on regulatory standards in the banking and insurance industry To highlight the need for regulation To present the framework for calculating capital and solvency requirements.

E N D

Session IIRegulatory Capital and Solvency Standards Dr. Peter Kandl April 2, 2007

Objectives • To give an overview on regulatory standards in the banking and insurance industry • To highlight the need for regulation • To present the framework for calculating capital and solvency requirements

Financial Institutions – Market Players Forms of financial institutions • Commercial / Retail banks • Hold customer deposits • Extend credit to businesses, households and governments • Securities houses • Investment banks (initial sale of securities in primary markets) • Broker-dealers (trading securities in secondary markets) • Universal banks • Combination of “traditional” banking and securities activities • Insurance companies • Property and casualty (P&C) or life insurance coverage • Reinsurance (Provide insurance coverage to primary insurer)

Systemic Risk • Both commercial banks and securities houses play role of intermediary • Facilitate payment flows across customers • Maintain markets for financial instruments • Systemic risk • Risk of a sudden shock that would damage the financial system • Involves contagious transmission of a shock • Affects other firms • Not limited to direct stakeholders • Failure can be potentially harmful to the overall financial system • Failure of a financial institution has fundamentally different effects than failure of an industrial corporation

Sources of Systemic Risk • Panicky behaviour of depositors or investors • Bank run • Depositors demand immediate return of their funds • Liquidity and credit crunch • Sudden drop in securities prices may lead to margin calls • Forces leveraged investors to liquidate positions at great cost • Interruptions in payment system • Failure of one counterparty results in chain reaction • Technological breakdown

Regulation of Commercial Banks • Deposit insurance (first established in 1933 in the US) • Insurance fund protects investors if their bank fails • Eliminates bank run • Most countries have developed compulsory deposit insurance program, but great variety across countries concerning implementation • Some of financial risks is passed on to the deposit insurance fund (I.e. government or taxpayer) • Creates need for regulation of insured institutions • Herstatt risk • 1974 failure of Bankhaus Herstatt, an active player in FX market • Bank shut down in noon, after having received DEM • Counterparties never received their USD • Serious liquidity squeeze for counterparties • Shock for whole FX market • Birth of Basel Committee on Banking Supervision (BCBS)

Regulations of Securities Houses • Objectives (fundamentally different than for commercial banks) • Protection of customers • Rationale: small investors are less capable of informed investment decisions • Opportunistic behaviour by financial intermediaries, antitrust legislation • Laws against trading on inside information • Disclosure rules for other conflicts of interests • Ensuring integrity of markets • Stabilise financial markets • Suitability standards, unsuitable recommendations may constitute fraud (punishable by law)

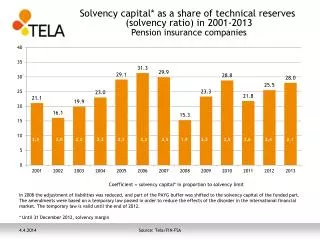

Regulations of Insurance Companies • Objectives • Protection of future benefits • Rationale: Event that triggers payment of benefits may occur decades later than inception date of contract • Claim amount often very high • Insurance companies have been heavily regulated (approval of tariffs and products) • Insurance protection fund • Regulation practice • Different across world / life insurance products tight to social security system • Solvency I: Prudential reservation rules instead of strong Capital rules • Solvency II project: harmonisation of regulatory practice based on new solvency framework

Balance sheets of financial intermediaries (*) claim / technical reserve (**) depending on pension scheme

Basel Committee on Banking Supervision (BCBS) • BCBS consists of central bankers from G-10(*) countries, plus Luxemburg and Switzerland • BCBS is sub-committee under Bank for International Settlements (BIS) • Setting (legally not binding) standards for banking supervision (harmonization) in order to • Promote safety and soundness to global financial system • Set level-playing field for global institutions • Have minimum risk-based capital standards for core institutions • Instituted minimum capital levels for internationally active banks (*)G-10 Belgium, Canada, France, Germany, Italy, Japan, the Netherlands, Sweden, UK, USA

Banking Supervision • Financial institutions ultimately regulated by their national supervisory authorities • USA • Board of Governors of the Federal Reserve System (FED) • Office of the Comptroller of the Currency (OCC) • Federal Deposit Insurance Corporation (FDIC) • United Kingdom • Financial Services Authority (FSA) • Switzerland • Federal Banking Commission (FBC/EBK)

Committee of European Banking Supervisors • Established in Nov 2003, first meeting Jan 2004 • High level representatives from the banking supervisory authorities and central banks of EU, including Central European Bank • 27 countries, 46 member organisations • Part of legal framework (has legal power) in EU, • Challenges and tasks • Ensure consistency in implementation of Basel II in member states • Pursue convergence of supervisory practices related to Basel II • Streamlining supervisory process for cross-border groups (co-cooperation between home-host authorities) • Effective consultations, enhance quality of supervisory standards

Insurance Supervision • Global: • IAIS (International Association of Insurance Supervisors) • Established in 1994 • Represents insurance regulators and supervisors of some 180 jurisdictions • Issues global insurance principles, standards and guidance paper • Promotes financial stability • Europe: • CEIOPS (Committee of European Insurance and Occupational Pension Supervision) • Same role as CEBS • United Kingdom • FSA • Switzerland • Federal Office of Private Insurance (FOPI / BPV) • Finma (as of 2009; fusion of FBC and FOPI)

Basel Accords • 1988 Accord (Basel I) • Risk-based capital charges for credit risk (assets) • 1996 Amendment • Incorporates market risk charge for trading book and FX-risk & CO-risk of banking book • Allows use of internal models • Basel II • More risk sensitive charges for credit risk; replaces partially 1988 accord • New capital requirements for operational risk

Roadmap for the insurance industry (1/2) • 1973 / 1979 First Non-Life / Life Directive • Simple rule-based framework, establishment of solvency margin • The solvency margin is the minimum amount of extra capital that an insurance provider must have to fall back on in unforeseen circumstances

Roadmap for the insurance industry (2/2) • Mid-1990s Third generation of life and non-life Insurance Directives (Solvency I) • Establishment of a single market for insurance („single passport system“) • System relies on mutual recognition of the supervision exercised by different national authorities according to rules harmonised to the extent necessary at the EU level • Since 2002 Solvency II (EU project) • Principles on capital adequacy and solvency (IAIS) (January 2002) • Framework made public in late 2005; implementation expected in 2011

Principles of Basel II / Solvency II Based on three pillars: • Minimum capital / solvency requirements • Rules (and / or principles) for calculating capital / solvency requirements • Supervisory review • Supervisory process to ensure fulfilment of minimum capital / solvency requirements, adequate internal processes ( governance structures, soundness of internal control and risk management systems) • Market discipline • Disclosure of information to shareholders and other stakeholders (incl. counterparties)

Role of Capital • Capital as buffer against unexpected losses • Must be permanent • Must allow for legal subordination (not preferred in case of bankruptcy) • Goal: absorb potential losses and thus avoiding bankruptcy / insolvency • Broader definition than equity (recognition of reserves, retained earnings, revaluation reserves, hybrid debt, subordinated term debt) • Classification according to quality into Tier 1, Tier 2 and Tier 3 capital (“tiering of capital”)

Basel II - Capital Requirements • Capital adequacy measured as (simplified) • Credit risk: risk weighted assets • Market / Operational risk: risk charges x 12.5 • „Well capitalized bank“: ratio 10% • Minimum regulatory standard of 8% corresponds approximately to BBB rating

Solvency II Framework / Structure Valuation of Assets & Liabilities Required capital by risk type Aggregation Identification ofrisk absorbingelements Market / ALM risk Assets Insurance risk Gross Capital requirement RequiredCapital SCR Liabilities Credit risk Risk Absorption Diversification Operational risk • Recognise that certain liabilities canbe used to absorb risks • Expected profits arisingfrom one year new business subtracted • Market consistent valuation of assets & liabilities • Option factored in • Takes into accountrisk mitigation andreinsurance • Allows for diversificationwithin risk types • Considers certaincombinatorial risks • Correlation andconcentration effectsacross risk types

Risk Based Solvency Regime Economic Balance Sheet Solvency Coverage Ratio (SCR) Insurance liabilities (fair value / bestestimate) Risk bearing capital >= 100% Required capital Assets (at market or near market value) • SCR < 100% does not imply insolvency • Introduction of intervention levels / ladders SCR green Required capital 100% Increasinglevel of regulatory intervention Risk bearing capital yellow 80% orange MCR* Free capital 30% red Risk bearing capital Capitalrequirements * MCR = Minimum Coverage Ratio

Credit Risk Charge – Standardised Approach • 8% of sum of risk-weighted assets • Risk weights according to claim type and obligor rating • External credit assessments for rating according to • Recognition process • Eligibility criteria • Implementation considerations • Recognition of credit risk mitigation techniques • Collateralization (for unsecured loans / haircuts) • On-balance sheet netting • Guarantees and credit derivatives

Credit Risk - Internal Approaches • Internal ratings-based approach (IRB) • Risk weight functions for corporate, sovereign, bank, retail, and equity asset classes • Foundation approach • Based on bank’s estimate of PD • LGD, EAD and M (effective maturity) provided by supervisor • Advanced approach • Use of bank’s internal PD, LGD, EAD and M estimates • Reliable process allowing to collect, store and utilize loss statistics over time is required

Market Risk - Approaches Two different approaches for calculation of capital charges: • “Standardized” method • Set of rules and weights • Internal models approach (IMA) • Banks are allowed to use internal models to determine capital requirements for market risk • Based on bank’s internal risk management system • Strong system of verification • Backtesting

Operational Risk 3 different approaches, based on either: • Basic indicator approach • 15% of average of positive annual gross income over 3 previous years (aggregate measure of business activity) • Does not account for controls • Can be strongly misleading (e.g. the lower fees, the smaller the capital charge) • Standardized method • Similar to basic indicator approach, but uses different multipliers for each out of 8 predefined lines of business • Total capital charge is 3-year average of sum of annual business line charges (can be negative), subject to floor of 0

Operational Risk (cont’d) • Advanced measurement approach (AMA) • Banks can use their internal models, as long as sufficiently comprehensive and systematic • Qualitative requirements regarding operational risk function, involvement of management, risk assessments, loss data analysis, monitoring, reporting, documentation, reviews • Banks are allowed to recognise risk mitigant effects of insurance (limited to 20% of total OR charge)

Key Elements of Swiss Solvency Test (SST) Standard Models or Internal Models Mix of predefined and company specific scenarios Scenarios Valuation Models Risk Models Market Risk Market Value Assets Credit Risk Best Estimate Liabilities Life (non BVG) RM Life (BVG) Output of analytical models (Distribution) Aggregation Method Target Capital SST Report

Standard Models P&C Risk Market Risk Correlations btw risk factors (interest rates, equity, FX, implied volatilities) Small Claims (Gamma Distribution) Premium Risk Large Risk (Lognormal) Insurance Risk Catastrophes (Compound Poisson-Pareto) Run-off Risk (Lognormal) RiskMetrics type approach with ~80 risk factors. Sensitivities w.r.t. risk factors of both assets and liabilities have to be determined Life Risk Credit Risk Covariance approach for 8 risk factors (mortality, morbidity,…) Internal models have to be used if substantial embedded options and nonlinearities are in the books e.g. replicating portfolios, market consistent scenarios,… Basel II (standard, advanced or IRB); recalibration to 99% TVaR. Spread risk treated within the market risk model. Internal Models (CR+, KMV type,…) Credit risk of default of reinsurers is treated via a scenario Scenarios Historical financial market risk scenarios (Crash of 2001/2002, Russia crisis,…) Predefined scenarios (pandemic, industrial accident, default of reinsurers,…) Company specific scenarios (at least three, e.g. nuclear meltdown, earthquake in Tokyo,…). Scenarios have to describe impact of events on all relevant risk factors (e.g. Pandemic leads not only to excess mortality but also to downturn of financial markets).

Synopsis Objectives banking regulation • Avoid Bank Run / minimise systemic risks • Focus: Stabilise financial system (including payment & settlement) • Method: • Strengthen risk management • Minimum capital standards • Regulatory authority EU: CEBS (coordination) / Transposition into EU law (CAD: capital adequacy directive) • Regulatory authority UK: FSA • Regulatory authority Germany: BaFin • Regulatory authority Switzerland: FBC (FINMA)

Synopsis Objectives insurance regulation • Protect future benefits • Focus: Protection of beneficiaries • Method: • Strengthen risk management • Minimum solvency capital standards • Regulatory authority EU: CEIOPS (coordination) • Regulatory authority UK: FSA • Regulatory authority Germany: BaFin • Regulatory authority Switzerland: FOPI (FINMA)

Synopsis Regulatory framework - structure Basel IISolvency II • Pillar I Capital requirements Solvency requirements MR, CR, OR MR, CR, Ins.R, (OR) • Pillar II Review / Review / Quality RM Quality RM • Pillar III Disclosure Disclosure requirements requirements • Switzerland „Swiss Finish“ Swiss Solvency Test

Synopsis Regulatory systems - capital / solvency adequacy Basel IISolvency II • Approach Balance sheet extracts Total balance sheet • MR Standard / Internal Standard / Internal • CR Standard / Standard / Internal Internal (Basic / Adv.) • Ins.R - Standard / Internal • OR Simple Standard Standard Internal (“AMA”) • Aggregation Weighted Average Distribution (Correlation Diversification)

Synopsis Implementation roadmap 2005 2006 2007 2010 • Basel II Framework CAD Implementation QIS I to IV • Swiss Finish Implementation • Solvency II QIS I QIS II QIS III Implementation FrameworkDirective • SST Framework “SSTReport” Capital needsadapted