Download

1 / 11

110 likes | 115 Views

Itu2019s no over-exaggeration to say that bankruptcy can and does change your life. Not only can recovering financially be a challenge, it also takes a toll on your emotional health.

E N D

Life After Bankruptcy – Here’s How to Repair Your Credit • It’s no over-exaggeration to say that bankruptcy can and does change your life. Not only can recovering financially be a challenge, it also takes a toll on your emotional health. • If you’re in this position, re-building your credit score can be a struggle. But we want to reassure you that with the right strategy – it can be done.

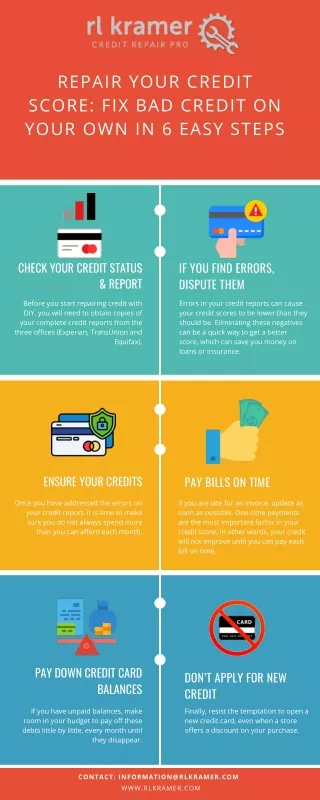

Tip #1 – Make sure that your credit record accurately details your bankruptcy • First things first – double check that your bankruptcy appears on your credit record. If it doesn’t you should contact Experian, as the alternative is to have multiple credit accounts showing as delinquent, and some creditors may even continue to report negative account markers even after your bankruptcy has been discharged.

Tip #2 - Use credit • Don’t be tempted to switch to using cash only in your day-to-day life. The only was to improve your credit score is to actually use credit! • You should register for a free credit reporting service, such as ClearScore or Noddle. These free services will provide you with customised tips as to how you can improve your rating, as well as suggesting credit products that may be suited to your score.

Tip #3 – Use clever credit products • It will undoubtedly be difficult, if not impossible, to be approved for regular credit products, so you’ll need to do your research as to which products offer the best chance of acceptance. • As a starting point, you can apply for a credit card designed for those with bad credit. Or, for a more certain chance of acceptance, you could use a rebuilder credit card. One type of credit rebuilder card is the CashPlus* Creditbuilder. The downside is that it costs £76 per year, but you’ll be guaranteed to be accepted. • The way it works is that the card acts as a ‘loan’ of the £76, which is repaid in £5.95 monthly repayments. These are reported on your credit file, and once complete it will show as a successfully repaid loan. • If you do go down this route, just be sure to meet ALL of your monthly payments. Not doing so could damage your credit even further.

Tip #4 – Avoid companies that claim to repair your credit • Only you – and you alone – can repair your credit. But unfortunately, there’s a litany of scammers and dodgy companies that claim to be able to fix your credit issues in record time. • DO NOT LISTEN TO THEM. • Some of these companies say that they can remove the bankruptcy from your credit file. However if the information is correct, they aren’t legally allowed to do this. You’ll simply receive a report that the information is accurate, although you’ll still end up paying a fee for the privilege.

Tip #5 – Make sure you pay all of your bills on time, every time • That means gas, electricity and contractual services (such as your internet and phone). If needed, add reminders to your phone’s calendar as to when bills are due – or pin them to a board in date order.

Tip #6 - Keep up with your non-bankruptcy account payments • It’s highly likely that not all of your credit accounts would have been included in your bankruptcy, so it’s mission-critical that these debts are paid on time. Debts that may fall under this category include: • Student loans • Magistrates court fines • Maintenance arrears • Child support arrears • Social fund loans • Walking possession order or controlled goods agreement made before your bankruptcy • Secured debts (such as a mortgage) • Debts to HM Revenue and Customs • Council tax liability order

Tip #7 – Can’t manage your money? Seek expert help • If you feel your spending spiralling out of control again, or are struggling to get a grip on bills, it’s imperative that you seek out advice from a trusted debt agency as soon as possible.

Above all else – and beyond these seven bankruptcy tips – it will be perseverance that helps you finally rebuild your credit rating. Just stay committed, focus on stringent money management, and eventually you’ll see your credit score beginning to climb.

Thank You National Debt Help • Beckwith House, 1 Wellington Road North, Stockport, SK4 1AF https://www.national-debt-help.co.uk