Download

1 / 31

310 likes | 429 Views

Sales Ideas & Marketing Concepts …. That Work !!! Robert G. Williams VP of Annuity Training. Today’s Agenda. How To Create Interest Which Crediting Method is Best. Index Annuity. How Does it Really Work? The Stairway to Financial Peace of Mind. Year 5.

E N D

Sales Ideas & Marketing Concepts …. That Work !!!Robert G. WilliamsVP of Annuity Training

Today’s Agenda • How To CreateInterest • Which Crediting Method is Best

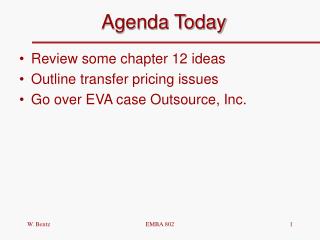

Index Annuity • How Does it Really Work? • The Stairway to Financial Peace of Mind Year 5 Year 6 Year 3 Year 4 Year 1 Year 2 $$$$

Hypothetical Annual Reset 8% Cap Index account $116,640 8% Cap Index Account $108,000 Index Gains Locked IN $108,000 What happens next year? Index Rises 10% Index Rises 10% Index Falls 10% Index Falls 10% $100,000 Annual Reset locks in the gain. Potential $ Protection

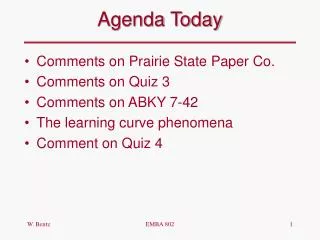

Index Annuity Hypothetical Year (8%) $102,350 1 2 3 4 5 6 7 (5%) $104,755 (7%) $107,217 (0%) $109,737 (3%) $112,315 $114,955 (6%) (0%) Index Value Min Guar % $108,000 $113,400 $121,338 $121,338 $124,978 $132,477 $117,656 $132,477 Surrender Fee May Apply Surrender Fee Will Apply

Sailing the Waters of theStock Market Poor Market Performance Market Index Financial Advisor

Monthly AverageHow It Works S&P 500 1,000 13,200 ÷12 =1,100 -1,000 =100 ÷ 1,000 =10%

Point to PointHow It Works S&P 500 or Dow 30 April 1, xx =1,000 March 31, xx =1,100 1,100 -1,000 =100 ÷ 1,000 =10%

Monthly AverageHow It Works S&P 500 1,000 13,200 ÷12 =1,100 1300 -1,000 =100 ÷ 1,000 =10% 900

Monthly AverageHow It Works S&P 500 (Oct. 1, 2003) 1018.22 13,372.68 ÷12 = 1114.39 - 1018.22 = 96.17 ÷ 1018.22 = 9.44%

Annual Point to PointHow It Works S&P 500 (Oct. 1, 2003) 1018.22 1131.50 - 1018.22 = 113.28 ÷ 1018.22 = 11.1%

Calculating Monthly Point to Point Date S&P Value Oct. 1 1018.22 Nov. 3 1059.02 • Subtract the starting value from the current value • Divide the sum by the starting value • Record the Index Change and New Starting point for the next month 1059.02 – 1018.22 = 40.80 40.80 ÷ 1018.22 = 4.0% Index Change for 1st month = 4.0% Starting point for 2nd month = 1059.02

Which Was PROBABLY More Beneficial To Consumer • Monthly Point to Point…9.23% • Monthly Average…9.44% • Annual Point to Point…11.1%

Index Crediting Assumptions • Monthly Point to Point Cap…3% • Monthly Average Cap…10% • Annual Point to Point Cap…9% • Closing Prices on First Business Day of each Month

Index Crediting Assumptions • Monthly Point to Point Total…24.69% 3% Monthly Cap Total…9.29% Credited Amount…9.29% • Monthly Annual Average…15.54% 10% Annual Cap Credited…10.00% • Annual Point to Point …26.30% 9% Annual Cap Credited…9.00%

Index Crediting Assumptions • Monthly Point to Point Total…29.84% 3% Monthly Cap Total…26.32% Credited Amount…26.32% • Monthly Annual Average…19.09% 10% Annual Cap Credited…10.00% • Annual Point to Point …34.13% 9% Annual Cap Credited…9.00%

Index Crediting Assumptions • Monthly Point to Point Total…26.10% 3% Monthly Cap Total…5.30% Credited Amount…5.30% • Monthly Annual Average…12.10% 10% Annual Cap Credited…10.00% • Annual Point to Point …26.67% 9% Annual Cap Credited…9.00%

Index Crediting Assumptions • Monthly Point to Point Total…24.22% 3% Monthly Cap Total…12.45% Credited Amount…12.45% • Monthly Annual Average…10.01% 10% Annual Cap Credited…10.00% • Annual Point to Point …26.38% 9% Annual Cap Credited…9.00%

Index Crediting Assumptions • Monthly Point to Point Total…9.34% 3% Monthly Cap Total…8.15% Credited Amount…8.15% • Monthly Annual Average…2.46% 10% Annual Cap Credited…2.46% • Annual Point to Point …9.48% 9% Annual Cap Credited…9.00%

Potential vs. Protection INDEX ANNUITY $$ -40% -20% 0% +20% +40% INVESTMENT

Why Index Annuities Investments Savings Program + 40% Participate in all or a portion of the S&P and/or DJIA $ +2.35% - 40%

Index Annuity vs. Market Market Up? You Don't Lose! You Win! Market Down?

And, of course…. Thanks for your business……..