Download

1 / 34

340 likes | 460 Views

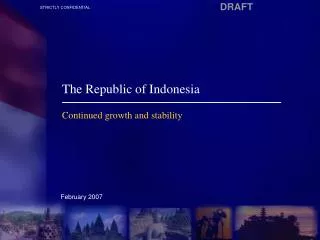

The Republic of Indonesia. Recent Economic Update July 2008. Outline. 1. 2. 3. 4. 5. 6. Fundamental Economic Strengths. 80. 10%. 85. 8%. 90. 95. 6%. 100. 105. 4%. 110. 2%. 115. Jan-08. Feb-08. Mar-08. Apr-08. May-08. Jun-08. Jul-08. 0%. SGD Curncy. PHP Curncy. J.

E N D

The Republic of Indonesia Recent Economic Update July 2008

Outline 1 2 3 4 5 6

80 10% 85 8% 90 95 6% 100 105 4% 110 2% 115 Jan-08 Feb-08 Mar-08 Apr-08 May-08 Jun-08 Jul-08 0% SGD Curncy PHP Curncy J F M A M J J A S O N D J F M A M J THB Curncy IDR Curncy Spread BI Rate – Fed Rate BI Rate Fed Rate (US$bn) (% y-o-y) 70 20 59.45 60 16 11.70 50 12 40 6.60 6.00 11.03 8 30 20 4 10 0 0 Jul Jul Jul Oct Oct Oct Nov Dec Nov Feb Jun Feb Nov Dec Jun Apr Apr Apr Jun Feb Sep Sep Des Mar Mar Mar Sep May Aug May May Aug Aug Jul Oct Jan Jan Nov Dec Feb Jun Apr 'Jan-06 'Jan-07 Feb Jun 'Jan-08 Apr Mar Mar May May Aug Sept Macroeconomic Stability Indonesia is maintaining macroeconomic stability substantiated by a stable exchange rate and increasing foreign reserves IDR / USD Exchange Rate BI Rate and Fed Fund Rate Spread Jun 08 = 650 bps 2006 2007 Foreign Reserves Inflation ± ± 2007: 6% 1% 2007: 6% 1% Export, FDI & Portfolio ± ± 2008: 11.7 % 2008: 11.7 % 2007 2008 2006 2007 2008

Sustained Economic Growth Indonesia has been growing at a rate above 6% since 4Q06 supported by private consumption and investment Real GDP Growth Source: Ministry of Finance

Strengthening Private Consumption 50% 80% 60% 40% 40% 29.2% 30% 20% 0% 20% 1Q05 1Q06 1Q07 1Q08 (20%) 10% (40%) (60%) 0% Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Car Sales Motorcycle Sales Consumption Credit Consumption credit growth is strong. Car and motorcycle sales, as a proxy of demand, have recently experienced significant growth Indonesia Car and Motorcycle Sales Consumption Credit Growth Y - o - Y Growth Y - o - Y Growth 200 5 200 6 200 7 200 8 Source: Bank Indonesia, CEIC

Improving Investment Climate New Investment Law passed in April 2007 aims to facilitate foreign investment. Continuous taxation reform expected to spur further investment Significant Improvements in Investment Climate Imported Capital Goods vs. Investments • Equal treatment for domestic and foreign investment (1) • Extends the validity of land titles • Rights to appoint foreign management • Unrestricted repatriation of profits and capital • Accelerated reform in tax administration • Simplified VAT audits and improved taxpayer services quality • 5% reduction in corporate income tax rate for listed companies which meet certain conditions • Reduction in the tax rate on dividend payments to non-residents from 20% to 10% • Significant increase in budget allocation for capital expenditure • Provides better clarity in business activities that are conditionally open to foreign investors Source: BKPM, CEIC 1. Subject to limits for foreign participation in certain sectors of the economy.

Revised 08 2000 2001 2002 2003 2004 2005 2006 2007 Budget 0% -0.5% -1.0% -1.0% -1.2% -1.3% -1.3% -1.7% -1% -2.1% -2.5% -2% -3% 80% 67% 61% 56% 60% 47% 39% 36% 36% 33% 40% 32% 31% 29% 28% 28% 24% 23% 21% 21% 21% 18% 15% 20% 12% 0% 2002 2003 2004 2005 2006 2007 2008 Total Debt to GDP Foreign Debt to GDP Domestic Debt to GDP Budget Deficit and Debt Ratios Budget Deficit (% of GDP) Avg. – 0.88% Avg. – 1.54% CONSOLIDATION STIMULUS Debt to GDP Ratio Source: Ministry of Finance

2008 Revised State Budget Maintaining fiscal stability in the face of external economic shocks Official State Budget 2008 Key Assumptions • Greater need for energy and food subsidies given persistently high crude oil and commodity price environment • Deficit could increase to 3% of GDP if no action was taken on subsidy allocation • Funding of the revised deficit is within a reasonable range given the consistent decline in the debt-to-GDP ratio over the past five years from 67% in 2002 to 35% in 2007 • Fiscal policy measures to mitigate the impact of heightened food and oil prices have been and are currently being implemented Source: Ministry of Finance

Tax and Non-tax Revenue Tax Revenue Non-Tax Revenue (IDR Trillion) • Tax revenue increasing because of ICP assumption and improved administration • Tax incentives: • Food prices (rice, cooking oil, soy bean, flour) • Reduced tax rate for publicly listed companies • Priority sectors include oil and geothermal • Actual non-oil tax revenue collection as of March 2008 increased 48.1% IDR tn IDR tn • Non-tax revenue increased due to: • Higher oil prices • Higher natural resources / mining revenues • Larger Pertamina and other SOE profits Source: Ministry of Finance

Actively Managing Expenditures and Subsidies Government Expenditure (IDR Trillion) Subsidies (IDR Billion) • 10% cut in ministries’ spending • Capital spending on infrastructure and poverty programs remains a priority • Providing for fiscal risk: • Oil price increase • Overrunning oil consumption • Macroeconomic volatility • Fuel subsidy capped at 3% of GDP: • Consumption limit • Fuel price adjustment • Further budget adjustment • Food subsidies for price stabilisation: • Rice for the poor • Cooking oil for the poor • Soybean and flour for SMEs Source: Ministry of Finance

Impact of Oil Prices and Food Staples on the Economy and 2008 Budget

Soaring Oil Prices Cause Fuel Subsidies to Escalate The ICP rose by 64% since the beginning of the year to average US$109.5/Bbl as of June International Oil Price Source: Bloomberg

Direct Cash Distribution Program Food Assistance Educational and Social Assistance Successfully Raised Fuel Prices to Manage Deficit The government raised fuel prices by an average of 28.7% on May 24, 2008 and has implemented cash and food assistance programs to mitigate impact on the poor Schedule of Fuel Price Adjustment Reduction in subsidy payments and contingency fund provision will be allocated to the following: Ensuring Fiscal Sustainability Source: Ministry of Finance

Fuel Price Hike Lowers Price Gap and Consumption Rise in fuel prices have reduced the price disparity and is expected to curtail over-consumption Subsidized Gasoline Consumption & Price Gap Trend Domestic vs. International Price Disparity Source: Ministry of Finance

Fiscal Policy Response to Soaring Oil Prices Use of Contingency Fund Diversified Financing Alternatives Reduction in Government Spending Fuel Price Hike & Compensation Packages for the Poor Fiscal Policy Measures Energy Savings Initiatives Optimizing Taxation in Nat Res & Commodities Optimizing Oil & Gas Production The Government has implemented a number of measures to ensure fiscal sustainability in the face of soaring oil prices With these fiscal policy measures, deficit is expected to fall from 2.1% to 1.8%

Impact of Fiscal Policy Adjustments on Budget Impact of Revised ICP Assumption on 2008 Revised Budget Outlook Source: Ministry of Finance

Disciplined Approach to Debt Management Objective To minimise cost of debt within manageable risk Prudent Rules Domestic Bond Market Development External Loan Financing Portfolio Management • Prioritise debt securities issuance in domestic market for deficit financing & debt refinancing • Diversify debt instruments to widen investor base • Develop market infrastructure to support efficient price discovery mechanism • Meet Millennium Development Goals (MDGs), (E.g. poverty reduction) • Finance cost recovery projects • Enhance project readiness criteria • Issue benchmark bonds on regular basis (E.g. 5, 7, 10, 15 and 20 years) • Aggressively conduct debt switching to extend duration • Buyback bonds to reduce outstanding debt and stabilize market • Diversify funding sources (e.g., Sukuk) Effective Coordination amongst Fiscal, Monetary and Capital Market Authorities

Impact of Fiscal Policy Adjustments on Financing Impact of Revised ICP Assumption on 2008 Revised Budget Outlook Source: Ministry of Finance

2008 Funding Strategy on Track The Government’s funding plans are well on-track with realized net financing at 69% of net financing required in the Revised 2008 Budget as of June 2008 Net Issuance Realization as at June 26, 2008 • Issuance in the domestic market will be prioritized • Issuance of a variety of domestic government securities • Fixed-rate • Variable rate • T-Bills • Zero coupon • Retail bonds • Syariah securities – Sukuk (3) • International bonds • Source: Ministry of Finance • Redemption and buyback amount subject to change • GDS stands for Government Debt Securities (SUN) • New Syariah instruments expected to be launched in 2008 in the form of Sukuk

Composition of Debt Balanced debt profile with a majority of debt being either Rp denominated or medium to long-dated By Maturity and Interest Rate, Dec 2007 Composition of Central Government Debt By Currency, Dec 2007 Source: Ministry of Finance Note: Exchange rate of Rp.9,034 per US$ used for period end 2007

Holders of Tradable Government Securities There is an increasing proportion of foreign and non-bank holders of Indonesian Government securities Foreign Holdings by Maturity, May 30, 2008 Holders of Tradable Domestic Gov’t Securities Developments in Domestic Market • Yearly issuance schedule publicly available • Established primary dealership infrastructure • Benchmark series • Active communication with market participants • Variety of domestic securities available • T-Bills, fixed rate, floating rate, variable rate, zero coupon, retail bonds and Sukuk (1) • Source: Ministry of Finance • New Syariah instruments expected to be launched in 2008 in the form of Sukuk

2008 1st Semester Revenue and Grant Realization Total Revenue Customs & Excise Revenue • Tax Revenue up to June 30, 2008 reached Rp307,5 T (50,5% of R-Budget) • Tax Revenue 112% from monthly R-Budget Target • Customs & Excise Revenue 122% from monthly R-Budget Target Tax Revenue

2008 1st Semester Expenditure Realization • Realization of 2008 exp. Budget was similar to 2007 • Compare to 2007, realization of 2008 central gov. exp showed a rising trend • Transfer to regions was bit lower than 2007 because of Block Grant (50%, last year 58%)

Energy Subsidies Subsidy Realization, 2006- 2008 (trillion Rp) Projection & Realization of (as of 30 June 2008) Realization of Fuel Consumption (mm KL) Up to 30 June, realization of subsidy was dominated by fuel subsidy BBM : Rp60,5 T, electricity subsidy: Rp26,4 T Realization of fuel consumption Jan - June 2008 reached 19,3 million KL, 2008 projection = 39 - 40 million KL

Challenges for 2008 Downward revision of GDP growth target from 6.4% to a range of 6.0% to 6.4% due to lower U.S. and global economic growth and economic effects of fuel subsidy reduction and cash transfer and food assistance programs Inflationary pressures from persistent high commodity prices (oil and food) With 28.7% domestic fuel price increase, the 2008 and 2009 state budget is sustainable even if oil prices remain high Savings from the reduction in subsidy payments will be allocated to provide direct cash transfers and other direct subsidies to the poor households Maintain a sound banking sector and effective intermediary function Monetary policy will be consistently aimed at addressing external inflationary pressures through preserving exchange rate stability and optimizing open market operation of the central bank Continuous improvement in investment climate to sustain robust economic growth