Download

1 / 18

190 likes | 339 Views

Buenos Aires, April 2008. Technological entrepreneurship 3 Valuation techniques. Valuation techniques:. Some of the more widely used valuation approaches, including: Asset valuations. Earning valuations. Cash flow valuations. Asset valuations (1).

E N D

Buenos Aires, April 2008. Technological entrepreneurship3 Valuation techniques.

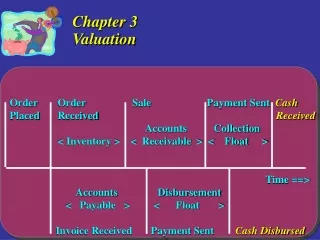

Valuation techniques: Some of the more widely used valuation approaches, including: • Asset valuations. • Earning valuations. • Cash flow valuations.

Asset valuations (1). • Asset valuation is one measure of the investor’s exposure to risk. • If within the company there are assets whose market value approximates the price of the company plus its liabilities, the immediate downside risk is low. • An increase in the value of the assets of a company may represent a major portion of the investor’s anticipated return.

Asset valuations (2). There are various approaches to asset valuation: • Book Value. • Adjusted Book Value. • Liquidation Value. • Replacement Value.

Asset valuations (3):Book Value. • Is the most obvious that a prospective purchaser can examine is the book value. • It provides tangible starting point. • The accounting practices of the company can have significant effects on the firm’s book value. Examples: • Taxes (deflation). • I+D (inflation).

Asset valuations (4):Adjusted Book Value. • Is the obvious refinement of stated book value and the actual market value of tangible assets. • Building and equipment that have been depreciated far bellow their market value. • Land that has substantially appreciated about its book value. • Intangible assets. • The figure resulting should more accurately represent the value of the company’s assets.

Asset valuations (5):Liquidation value. • Consider the net cash amount that could be realized if the assets were disposed in a “quick sale”. • Is not usually importance to a buyer who is interested in the maintenance of a going concern.

Asset valuations (6):Replacement Value. • Is the current cost of reproducing the tangible assets of a business. • It sometimes happens that the market value for existing facilities is considerably less than the cost of building a plant and purchasing equivalent equipment from other sources. • The calculation is more as a reference .

Earning valuations (1). • A second common approach to an investor’s valuation of a company is to capitalize earnings. This involves multiplying figures by a capitalizations factor of price-earnings ratio. • This raises two questions: • Which earnings? • What ratio?

Earning valuations (2). • Earnings Figure: • Historical earnings. • Future earnings under present ownership. • Future earnings under new ownership.

Earning valuations (3):Historical earnings. • Historical earnings can be used to reflect the company’s future performance. • This provides concrete realism. • Historical earnings per se can rarely be used directly, and an extrapolation of these figures to obtain a picture of the future must be considered a rough. • To gain the benefit from the information in a company’s financial history of the past operations, it is necessary to study each of the cost and income elements, their interrelationships, and their trends.

Earning valuations (4):Future earnings. • Wow much and in what ways income and costs are calculated for future operations depends to a large degree on the operating polices and strategies of management. • The existing or future owners ´approach will be influenced by a host of factors: • Management ability. • Economic and not economic objetives. • And so on.

Earning valuations (4):Future earnings. • Two approaches: • Future earnings under present ownership. • Future earnings under new ownership.

Financial topics(5). (*) CFT: COSTO FINANCIERO TOTAL. TNA: TASA NOMINAL ANUAL. TEA: TASA EFECTIVA ANUAL. La cuota inicial incluye intereses, gestión y otorgamiento por cobertura de vida un titular y seguro de incendio. Plazo de interés 60 meses Plazo de amortización 120. Cuota calculada para primera vivienda. Porcentaje de financiación 70% TNA 17.00%, TEA 18.39%, CFT 19.38%. Ingresos mínimos $2500 para primera vivienda y $4000 para segunda vivienda. Créditos sujetos a la aprobación de Santander Río. Esta línea no posee super recompensa