Download

1 / 18

180 likes | 444 Views

THE RISE AND FALL (and RISE?) OF ELAN. (Or How Accounting Can Compensate for Strategic Shortcomings—for a While.) By Baruch Lev *.

E N D

THE RISE AND FALL (and RISE?) OF ELAN (Or How Accounting Can Compensate for Strategic Shortcomings—for a While.) By Baruch Lev* *Thanks to Jennifer Tucker for her assistance in preparing this case. The information underlying this case is all in the public domain: stock data, Elan’s announcements and financial reports, and newspaper articles. I made no attempt to independently verify the information in this case. January 2006

Elan Who? • Founded in Dublin, Ireland in 1969, and began trading on NASDAQ in 1984 (ADS on NYSE from 1995). • As of January 2002, Elan was the world’s 20th largest drug company with a market capitalization of $12 billion ($20 billion in 2001). It was the largest Irish company, accounting at its height for ¼ of the total market capitalization of the Irish Stock Exchange. • Elan started as a drug-delivery system company (e.g., nicotine patches) and developed into a full-range drug development company through a series of acquisitions in the 1990s. It focuses on the development and commercialization of pharmaceutical products using its extensive range of proprietary drug delivery technologies, and on the development of products and services in neurology, pain management, oncology, infectious disease and dermatology. • Alas, from the heights of $65 in 2001, Elan’s stock price crashed to $1-2 in 2002 (total market value around $600 million). WHAT HAPPENED?

Forecast Actual Data Source: I/B/E/S

What Did Investors Know, and When? • It Is Clear From Elan’s Stock Price Behavior That Each News Item Caught Investors by Complete Surprise. • But Quarterly and Annual Financial Reports, Audited by Independent Accountants, Are Supposed to Provide Investors with a Continuous Stream of Information, Minimizing Surprises and Disappointments. • So, What Happened to Elan’s Financial Reports? Consider the Following Three Major Issues:

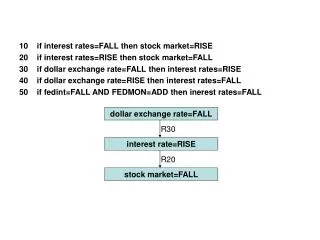

I. Accounting for Research & Development (R&D) Costs Accounting Rule: All R&D expenditures—particularly heavy for drug companies—have to be immediately expensed in the income statement, thereby decreasing short-term reported earnings. A Bind: Current hit to earnings for uncertain future benefit. Elan’s cure: 55 Joint Ventures (JV) Elan Joint Venture Partner Outcome: Rather than incurring R&D expenses, Elan recorded large licensing revenues from JVs. In 1999, Elan invested $211M JV and recorded $139M licensing revenues. In 2000, $405M investment in JV, and $299M in licensing revenues. In 2001, $229M investment, and $173M revenues.

Elan’s Commentary: “We don’t have to do the Merck model of bringing everything inside. The advantage of that is complete control. The disadvantage is it costs a lot of money.” (Ivan Lieberburgh, Elan’s chief scientific officer). Main Source: 1/30/02. The Wall Street Journal Europe. P 1.

II. Accounting for Investments But if Elan doesn’t record R & D expenses, the joint ventures do. So what is gained? Reporting Rules Investment <20%: Cost/Market Investment>20% but 50%: Equity Method Investment>50%: Consolidation Elan’s Joint Ventures Elan 19.9% Ownership JV Most of the JV partners were moribund companies. “Some of the best bargains can be made bottom fishing.” (Lynch, Elan’s CFO). Outcome: The financials of the JV were not consolidated into Elan’s reports. Losses and debt were shifted to JV and obscured from investors.

III. Separating Core from Non-Core Earnings Accounting Rule: Extraordinary, non-recurring (non-core) revenue or expense items have to be separated in the income statement from recurring-core items to enable investors to assess the sustainability of earnings. In 2002, amid serious financial difficulties, Elan sold various product lines (divisions) and allegedly aggregated the proceeds with regular product revenues. In some cases Elan lent money to buyers or had a significant investment in buyers of the product lines. Sometimes, Elan’s executives “freelanced” as buyers executives.

GAAP Violations: Where Were the Auditors? • If revenues (licensing income in Elan’s case) require future commitments, they should be apportioned over subsequent periods. (Elan admits, and restates earnings by $344 million). • If firm has significant influence over a related company (JV in Elan’s case), equity method is called for despite < 20% investment. (Elan had veto power over JV research, 50% board representation). • Some buyers of product lines should probably have been identified as “related parties.” The concept of “arm’s length transaction.” • The “original sin”—GAAP requirement to expense all R&D and other intangible investments.

How About The Fundamentals? Accounting Misrepresentation Often Come In the Wake of Strategic Mishaps and are aimed at portraying “business as usual” • Strategic Issues • Elan probably paid too much for “growth” acquisitions. For example, the in-process R&D write-offs of some acquisitions were even higher than the purchase price. • It had chosen some weak joint-venture partners so that it had to write off investments. • Getting quickly to be a major drug company is very costly and risky.

Is There Life Beyond Accounting Scandals? On January 2, 2003 the Wall Street Journal (p. D4) reported the results of a study showing that people suffering from relapsing forms of multiple sclerosis might benefit from the experimental (not yet approved by the FDA) drug Antegren. The drug is co-developed by Biogen Inc., and Elan Corp. The worldwide MS market is estimated at about $2.5 billion, and expected unfortunately to grow to $4 billion by 2005. Elan’s stock price increased by 13% on the news. (But, it also increase 13% on the preceding trading day, 12/31/02. Insider trading/information leakage?)

More recently: December 23, 2004: “Three midsize drug makers are faring better than larger rivals…. Thanks to cost-cutting programs and a narrow focus on a few therapeutic areas, companies such as Ireland’s Elan Corp.,…have been bringing new products to market and enjoying some of their best financial results in years.” (The Wall Street Journal, p. B2).

Still Struggling After All These Years • “On 28 February 2005, we and Biogen Idec voluntarily suspended the marketing and clinical dosing of Tysbari. This decision was based on reports of two serious adverse events in patients treated with Tysbari…” • “At December 31, 2004, we have $46.6 million of other intangible assets and goodwill and $1.9 million of inventory relating to Tysbari… Ourreassessment does not indicate impairment at this stage…” • “Goodwill arising from acquisitions since 1998 is capitalized and amortized…The average amortization period of goodwill is 19 years.” • Net 2004 loss under Irish GAAP: $368.3 million vs. net loss under U.S. GAAP: $394.7 million. • 2004 R&D: $259.0 million vs. 2003 R&D: $331.4 million. Source: Elan's 2004 Financial Report.

Stock Prices Healthcare Index ELAN Data Source: Yahoo Finance

The Moral of the Story • Comprehensive, In-Depth Knowledge of Accounting is Essential for Investment Decisions, Board Supervision, Bond Ratings, and Lending Decisions, Not to Mention—Management. The Warning Signs are Often Out There: For example: • 19.9% Investment in Subsidiaries. • Revenues, yet no R&D, expenses. • The Earnings-Cash Flow Gap. • The Irish-U.S. GAAP Reconciliation. • Questionable assets. • Indeed, Elizabeth McDonald (Forbes, 9/18/2001) saw it all from public sources, but investors ignored the warning (price down 2% only).