Download

1 / 41

410 likes | 485 Views

Maxine on Healthcare. Let me get this straight. We're going to be "gifted" with a health care plan we are forced to purchase and fined if we don't,

E N D

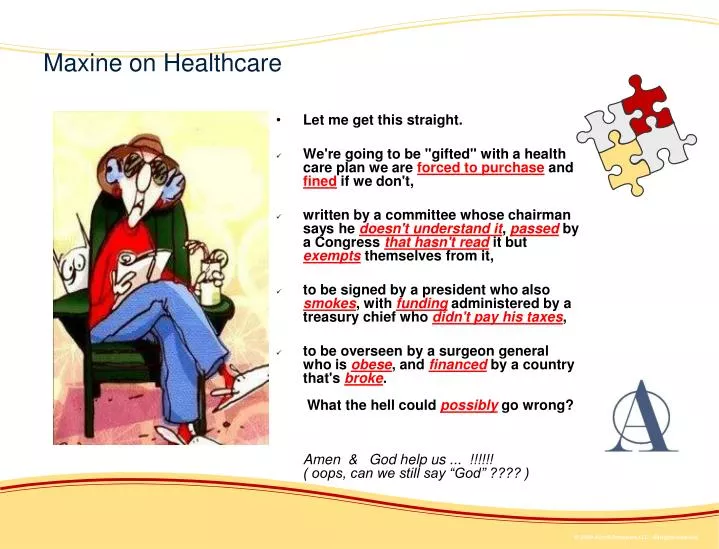

Maxine on Healthcare Let me get this straight. We're going to be "gifted" with a health care plan we are forced to purchase and fined if we don't, written by a committee whose chairman says he doesn't understand it, passed by a Congress that hasn't read it but exempts themselves from it, to be signed by a president who also smokes, with funding administered by a treasury chief who didn't pay his taxes, to be overseen by a surgeon general who is obese, andfinanced by a country that's broke. What the hell could possibly go wrong?Amen & God help us ... !!!!!! ( oops, can we still say “God” ???? )

Wisconsin Grocers AssociationComprehending ObamacarePresented by: Randy Averill Averill Anderson, LLC Mark Anderson Averill Anderson, LLC Brian Smith Rogers Benefit Group, Inc.

I’m from the government And I’m here to help you!

2700 PAGES +30 PAGES OF REGULATIONS for each of those pages OVER 80,000 PAGES! Store-front is in place, but there are a lot of empty shelves!

How The Government Insured Squeeze Medicine Hospital Payments-to-cost Ratios for Medicare, Medicaid & Private Payers 1995-2007

The Uninsured: Who are They? “46.3M Uninsured at the end of 2008”

Overall Approach • Starting 1/1/2014, all US Citizens must have “Minimum Essential Coverage” • Individual • Employer-sponsored • Government programs • Create state-based insurance exchanges • Expand Medicaid and offer cost-sharing subsidies • Require employers to play or pay • Impose new regulation and reporting requirements • Establish government long term care benefits • Roll out • 1st Wave March 23, 2010 to 2013 • 2nd Wave 2014

The Core of Reform: Expand Coverage • 0% to 133% of Federal Poverty Level = 23.3% of population or about 71 million Americans.IRS is the collector! • Will be given access to Medicaid (free coverage) current Medicaid population ~ 45 million people. IRS is the collector! • 134% to 400% of Federal Poverty Level = 66.9% of population or about 204 million Americans. IRS is the collector! • Will be able to purchase health insurance with federal subsidies on state exchanges (if employer does not offer FQHBP-level coverage). IRS is the collector! www.census.gov: 2008 Inflation Adjusted Dollars, 2009/2010 FPL guidelines

True Cost of Health Reform The true first 10 year costs: $1.8 Trillion What the Democrats call the “first 10 years” (2010 – 2019) The true first 10 years (2014 – 2023) Percentage of “10 year” costs that hit in the first 4 years: 1% Chart produced by: Jeffrey H. Anderson, Senior Fellow, Pacific Research Institute

Individual Mandate 2014 • Starting 1/1/2014, all U.S. citizens must have “minimum essential coverage” • Cannot consist of only excepted benefits – e.g. limited scope dental, vision, health FSA • Plans should use “good faith effort” to comply with a “reasonable interpretation” • Individual non-compliance penalties start at $95 in 2014, phase to $695 per adult in 2017 (1/2 for child) • Massachusetts “The Connector” individual penalty began < $100, today $1,200

Premium Assistance Tax Credits • Designed to guarantee that qualified individual’s medical insurance cost is limited to a specified percentage of their household income.

Exchanges 2014 • Available in 2014 for individuals and companies with less than 100 employees • Assist consumers in shopping for medical insurance • State government sponsors, reviews and approves • Insurance companies submit policy, coverage and premiums • State-run co-op plan option

2014 Employer Responsibility • No employer mandate • Federal government incentives/disincentives to employers to provide minimum essential coverage • Based on # of FTE Employees • Tax Credit • Penalties . . . A few empty shelves

Full Time Equivalent (FTE) • Used to determine which rules apply to specific businesses • Example • 40 employees working 30 hours or more per week • Part-Time employees worked 3,200 hoursduring the previous month

Employer Incentives / Disincentives 2010 • Small Employer Tax Credit 2010 • Eligibility • 25 FTE or less • Average Annual Salary <$50,000 • Employer pays at least 50% of Premium Small business tax credit calculator powered by H&R Block: http://www.makinghealthcarereformwork.com/healthcarereform/healthcare.html

Shared Responsibility Surcharge – No Employer Coverage 2014 • Employers with at least 50 FTE not offering coverage (minimum essential benefits) • If one employee receives a tax subsidy to buy insurance through an “Exchange” then this applies

Shared Responsibility Surcharge – Employer Coverage 2014 • Employers with more than 50 FTE offering coverage • Employee buys through an Exchange and receives premium assistance credit • Must pay the lessor of $3,000 for each “employee receiving a premium credit” or $2,000/FTE (minus 30)

Vouchers: 2014 • Employer offering minimum essential coverage and pays any portion of cost must provide Free Choice Voucher to a qualified employee • Qualified Employee • EE Required contribution between 8-9.8% of household income • Household income < 400% FPL • Waives Participation • Voucher value based on plan in which “employer pays the largest portion of the cost of the plan” • Employee uses voucher to purchase exchange coverage • Excess value of voucher kept by employee

CLASS 2010 Community Living Assistance Services & Supports Act • Effective January 1, 2011 • Creates a voluntary federal long-term care plan • 5-year waiting period before benefits are payable • Secretary of HHS • must publish details by October 1, 2010 • Premiums $240/mo CMS actuary • Vesting period • Benefit triggers • Cash Benefit $50 - $290 / day

Revenue(TAX) Raising Provisions • Starting July 1, 2010, imposes a 10% tax on tanning services. • Beginning in 2011, the pharmaceutical industry will pay annual industry fees. The fee will be phased in and will hold steady at $2.8 billion a year after 2019. • A new 3.8% tax will be added on income from interest, dividends, annuities, royalties and rents for those individuals who make more than $200,000 and couples that make more than $250,000 annually. • Beginning October 1, 2012, insurers charged a $1 to $2 Comparative Effectiveness Research fee per covered life

Revenue(TAX) Raising Provisions • Beginning in 2013, manufacturers of medical devices will pay a 2.3% excise tax on sales of medical devices. • Beginning in 2013, the Medicare payroll tax rate increase by 0.9% for individuals who make more than $200,000 and couples that make more than $250,000 annually. • Beginning in 2014, Health Insurance Sector Tax, a non-deductible premium tax imposed on insurers and TPA’s • $8.0 Billion Excise Tax • $11.3 Billion in 2015, 2016 • $14.3 Billion in 2018

Health Reform Implementation Timeline • Effective plan years beginning on or after March 23, 2010 • Small employer health insurance credit • Wellness rewards increased 20% to 30% • Executive medical plans offered to HCE only discriminatory • Grandfathered Plan Option

Health Reform Implementation Timeline • 2011 • No reimbursement for OTC drugs unless prescribed. • Form W-2 Reporting • Effective for coverage January 1, 2011 • Report value of employer sponsored health coverage • Does not include FSA Contributions, LTC, accident or disability, disease specific hospital or fixed indemnity insurance • Generally COBRA rates • CLASS may begin

Health Reform Implementation Timeline • 2012 • Uniform explanation of coverage • 4-page pre-enrollment coverage document sent outlining benefits and exclusions • 60-Day notice in Advance of Material Modifications • “FSA maximum contribution - $2,500”

Wisconsin Grocers AssociationComprehending ObamacarePresented by: Randy Averill Averill Anderson, LLC Mark Anderson Averill Anderson, LLC Brian Smith Rogers Benefit Group, Inc.

Grandfather Status Health plans in force March 23, 2010 are considered a “grandfathered” plan are exempt from some of the changes. To remain grandfathered, you cannot make benefit changes that increase employees cost.

Grandfather Status – The following benefit changes will not cause loss of grandfathered status: Adding employees to your plan Complying with federal or state law Increasing employee contributions by 5 percent or less Voluntarily changing benefits to comply with healthcare reform

Grandfather Status – Examples of changes that will cause a plan to lose grandfathered status: Obtaining a new policy, certified, or contract of insurance sold after March 23, 2010 Eliminating benefits for a particular condition Adding or decreasing overall annual dollar limit Increasing coinsurance percentage Increasing deductible or out-of-pocket maximum by more than medical inflation, plus on-time-only 15 percent increase Increasing copayments for any service by more than the annual rate of medical inflation, plus a one-time-only 15 percent or $5 increase, whichever is greater Decreasing employer contribution rate by more than 5 percent Changing carriers (fully-insured plans only)

Benefit Changes – Plans sold or renewed with an effective date on or after Sept 23, 2010, will experience the following benefit changes: Lifetime maximum. Plans will have an unlimited maximum Annual dollar limits. No annual dollar limits on covered essential health benefits including: - Prescription drugs - Emergency services - Hospitalization - Maternity and newborn care - Mental and substance use disorder, including behavioral health treatment - Ambulatory patient services - Rehabilitation and facilitative services and devices - Laboratory services - Preventative and wellness services and chronic disease management - Pediatric services, including dental and vision care Emergency care. Plans will cover services for emergency medical care administered in a hospital’s emergency facility at the in-network benefit level.

Benefit Changes – New groups or plans no longer grandfathered on or after Sept. 23, 2010, will also include: Preventive services. Plans will cover in-network preventive care services at 100 percent. Members will not pay a copayment, coinsurance, or deducible. Some preventive services covered by the regulation include: -Immunizations - Blood pressure screenings - Cholesterol screenings - Mammograms - Colonoscopies - Obesity screenings - Type 2 diabetes screenings - Diet counseling - Obesity screenings and counseling - Tobacco-use screenings

Pre-existing conditions Pre-existing condition limitations will not apply to a covered person under age 19. This provision will apply to your benefit plan at your next renewal after Sept. 23, 2010, unless otherwise specified.

Early Retiree Reinsurance Program The regulations create a new $5 billion reinsurance program for employers that provide health insurance coverage to early retirees who are over age 55 but are not eligible for Medicare. This program began June 21, 2010, and continues until insurance exchanges become available on Jan. 1, 2014 or funding for the new program runs out.

Primary care physicians and Gynecological and obstetric services If a plan requires designation of a primary care physician who specializes in pediatrics may be selected as the primary care physician for a covered dependent child. If a plan provides coverage for gynecological or obstetric care, authorizations or referrals for such care are no longer required for such care, as long as the provider remains in your network.

Non-discrimination rules Groups may no longer restrict membership in a benefits program that favors highly compensated individuals, as defined by the federal government. The only exception for this provision is if the health plan has retained its grandfather status.

Minimum Loss Ration 85% Large Group 80% Small Group

Exchanges State based for individuals and group 2-100 employees Operational by January of 2014 Community rated with 5 benefit categories; Bronze, Silver, Gold, Platinum, Catastrophic Required to maintain a call center, enroll individuals and determine tax credits. Carriers participating in the exchange will pay a fee, must meet marketing requirements and be accredited.

Healthcare Reform = ChangeEmployee • Health Benefit Options • Employer Plan • Government health plans • Exchange • Guaranteed coverage on demand • Cost • Employer plan contribution • Tax credit subsidy • Value of free choice Voucher • Cost of non-employer plans • Pay penalty

Healthcare Reform = ChangeEmployer • Attract and retain the best employees by offering high value benefit plans while minimizing costs • Budget • FTE – Subsidy / Penalty situation • Private insurance plan design • Alternative sources for health benefits • Government programs – Medicaid, Medicare, BadgerCare, etc • Exchange plan options and individual premium • Value of Voucher • Employee Contribution • Employee Household income • Compliance with rules and regulations

Thank you! Have questions? AVERILL ANDERSON, LLC - employer benefit solutions- (800) 388-0964 hra@averillanderson.com