Download

1 / 25

250 likes | 462 Views

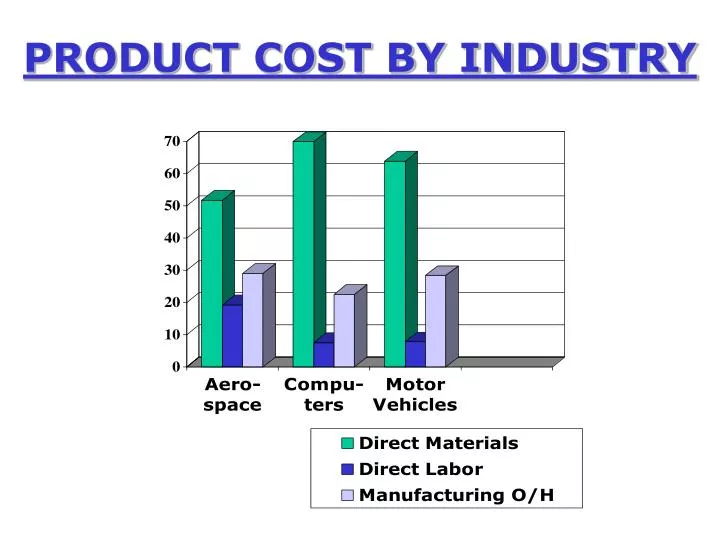

PRODUCT COST BY INDUSTRY. Overview of Costing for Manufacturing Companies. Manufacturing Overhead. Indirect Cost Pool Cost Allocation Base Cost Object Direct Costs. Machine Hours. Product Cost. Direct Materials. Direct Labor. Five Step Approach to Job Costing.

E N D

Overview of Costing for Manufacturing Companies Manufacturing Overhead Indirect Cost Pool Cost Allocation Base Cost Object Direct Costs Machine Hours Product Cost Direct Materials Direct Labor

Five Step Approach to Job Costing • Identify the cost object. • Identify the direct costsfor the job. • Identify the indirect cost poolsassociated with the job. • Select the cost allocation basefor each indirect cost pool. • Calculate the rate per unitof the allocation base to allocate indirect costs.

Calculation of Overhead Rates Overhead Rate = Total Costs in the Cost Pool Total Quantity of the Cost Allocation Base

Activity-Based Costing The key assumption in Activity-Based Costing is that overhead costs are caused by a variety of activities, and that different products utilize these activities in a non-homogeneous fashion. ABC attempts to select as the allocation base the best cost driverfor each overhead cost item; i.e., the cost driver that best captures the cause and effect relation-ship between products and overhead costs.

Overview of Costing for Manufacturing Companies Manufacturing Overhead Indirect Cost Pool Cost Allocation Base Cost Object Direct Costs Machine Hours Product Cost Direct Materials Direct Labor

Overview of Costing Under ABC PURCH- ASING PERSONNEL MACHINE SHOP INDIRECT COST POOLS COST ALLO-CATION BASES COST OBJECT COST TRACING DIRECT COSTS MACH. HRS # OF PARTS D.L. HR.S INDIRECT COSTS DIRECT COSTS D.M. D.L. WARRANTY

Cost Allocation Bases used for Manufacturing OverheadU.S. Manufacturers

Cost Allocation Bases used for Manufacturing Overhead Japanese Manufacturers

Cost Allocation Bases used for Manufacturing OverheadU.K. Manufacturers

Dialysis Clinic, Inc. Two types of Dialysis:

Dialysis Clinic, Inc. Summary of Costs and Identification of Cost Drivers:

Dialysis Clinic, Inc. Summary of Costs and Identification of Cost Drivers:

Dialysis Clinic, Inc. Summary of Costs and Identification of Cost Drivers:

Dialysis Clinic, Inc. Summary of Costs and Identification of Cost Drivers:

Dialysis Clinic, Inc. Calculation of Overhead Rates:

Dialysis Clinic, Inc. Calculation of Overhead Rates:

Dialysis Clinic, Inc. Calculation of Overhead Rates:

Dialysis Clinic, Inc. Allocation of Costs using A.B.C.:

Dialysis Clinic, Inc. Allocation of Costs using A.B.C.:

Dialysis Clinic, Inc. Allocation of Costs using A.B.C.:

Dialysis Clinic, Inc. Allocation of Costs using A.B.C.:

Dialysis Clinic, Inc. Summary of Costs:

Dialysis Clinic, Inc. Summary of profitability:

Dialysis Clinic, Inc. Summary of profitability: