Download

1 / 87

900 likes | 1.13k Views

ETHICS . What Every Tax Preparer Needs to Engrave in Their Thoughts. Presented By: Marcia L. Miller, MBA, EA Financial Horizons, Inc. Weston, Florida ProactiveTax@aol.com.

E N D

ETHICS What Every Tax Preparer Needs to Engrave in Their Thoughts

Presented By: • Marcia L. Miller, MBA, EA • Financial Horizons, Inc. • Weston, Florida • ProactiveTax@aol.com

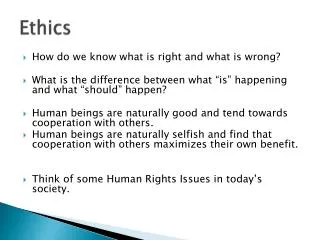

Ethics has always been a requirement, but will our clients agree not to control us by swaying our ethical requirements? • Frivolous tax arguments and tax scams will always be a dilemma to be reckoned with, but now – more than ever – it is imperative that we not trust the client too much.

Imagine a Pyramid • At the bottom appears the CodeofProfessionalConduct’s six principles are the cornerstone of ethical behavior. They include: 1 - Responsibilities 2 - The Public Interest 3 - Integrity 4 - Objectivity and Independence 5 - Due Care 6 - Scope and Nature of Services

Principles • These are positive statements of responsibility in the Code of Professional Conduct that provide the framework for the rules, which govern performance.

Next are the rules by which we are governed whether we are in the practice of accounting or merely providing professional services. • Independence • Integrity and objectivity • General Standards • Compliance with Standards • Accounting Principles • Confidential Client Information • Contingent Fees • Acts Discreditable • Commissions and Referral Fees • Advertising and Other Forms of Solicitation • Form of Organization and Name

RULES • Broad but specific descriptions of conduct that would violate the responsibilities stated in the principles in the Code of Professional Conduct.

Now as the Pyramid narrows, you as the professional, must make your own interpretations of these specific rules, some of which may require rulings for certain circumstances.

INTERPRETATIONS • This refers to those pronouncements issued by organizations such as the AICPA’s Division of Professional Ethics to provide guidelines concerning the scope and application of the rules of conduct.

ETHICS RULINGS • Rulings summarize the application of rules and interpretations to a particular set of factual circumstances.

“YOUR BEHAVIOR” • Lastly, at the top of your pyramid is the Behavior for which your peers are judging your actions. • Your Behavior needs to be impacted by the Code, Interpretations and Rulings.

CIRCULAR 230 • In order to protect citizens from incompetent and unethical practitioners, governments have passed laws and regulations regarding the professional conduct of certain professionals who provide accounting and tax services. In particular, Certified Public Accountants (CPAs) and Public Accountants (PAs) are regulated by State Boards of Accountancy; and professionals who are authorized to practice before the Internal Revenue Service (IRS) are regulated by Treasury Department Circular 230 and the IRS Office of Professional Responsibility. The body of law which is intended to protect citizens from unethical behavior is sometimes referred to as regulatory ethics. Those who are regulated and fail to uphold the required standards of ethical and professional conduct are guilty of committing acts which are not only unethical, but also illegal.

CIRCULAR 230 • Many accounting and tax practitioners are not directly regulated by State Boards of Accountancy or the Internal Revenue Service. However, the standards of ethical and professional conduct established by those authorities represent the high expectations of the citizens who are served by the accounting profession. Because these standards are widely published and well known, they may also be used in a court of law when a citizen sues to obtain damages from a practitioner. Therefore, it is important for all accounting and tax professionals, whether regulated or not, to understand the high level of ethical and professional conduct that is expected because of the trust that is conveyed to them by the individuals and businesses they serve.

CIRCULAR 230 • Liability for Fraud Actual fraud and constructive fraud present two different circumstances under which an accountant may be found liable. An accountant may be held liable for actual fraud when he or she intentionally misstates a “material fact” to mislead his or her client, and the client detrimentally relies on the misstated fact. A material fact is one that a reasonable person would consider important in deciding whether to act. Constructive fraud, on the other hand, will be found when an accountant is grossly negligent in the performance of his or her duties. The intentional failure to perform a duty in reckless disregard of the consequences of such a failure would constitute gross negligence on the part of an accountant. Both actual and constructive frauds are potential sources of legal liability under which a client may bring an action against an accountant. When a client is dissatisfied with the performance of an accounting firm, he or she will often sue on all three common law theories in the alternative. The Federal Rules of Civil Procedure permit a pleader, in a claim or defense, to make two or more statements which are not necessarily consistent with each other. A plaintiff may sue on several theories.

CIRCULAR 230 • Treasury Department Circular 230 Circular 230 provides regulations governing the practice of Attorneys, Certified Public Accountants, Enrolled Agents, Enrolled Actuaries, Enrolled Retirement Plan Agents, and Appraisers before the Internal Revenue Service. As part of an ongoing effort to improve ethical standards for tax professionals and to curb abusive tax avoidance transactions, the Treasury Department and the Internal Revenue Service have issued final regulations amending Circular 230 to achieve the strategic goal of ensuring that attorneys, accountants, enrolled agents, and other tax practitioners adhere to professional standards and follow the law. Subpart B of Circular 230 describes the duties and restrictions relating to practice before the Internal Revenue Service, the best practices for tax advisors, and standards with respect to tax returns, financial documents, and workpapers. Subpart C describes the sanctions for violation of the regulations, and defines incompetence and disreputable conduct for which a practitioner may be sanctioned. The most recent revision of Circular 230 is available on the Internal Revenue Service website.

CIRCULAR 230 • Tax professionals who are authorized to practice before the Internal Revenue Service (that is, to represent clients) are regulated by the Office of Professional Responsibility (OPR) and are legally obligated to follow Circular 230 requirements. Tax professionals who are not authorized to practice before the Internal Revenue Service are not directly regulated by OPR. However, all tax professionals should be familiar with Circular 230 as many of the standards and best practices discussed are universally applicable. Some of the most important requirements regarding professional conduct are summarized below. • Furnishing Information: A practitioner must furnish records or other information to the IRS or OPR upon a proper and lawful request unless the practitioner believes in good faith and on reasonable grounds that the records or information are privileged. If the practitioner does not possess the requested records, he/she must promptly notify the requesting IRS officer or employee. The practitioner must ask the client where the requested records are located, and provide any information regarding the identity of any person who the practitioner believes may have possession of the requested records to the IRS officer or employee. • Knowledge of Client’s Omission: If a practitioner knows that a client has not complied with the revenue laws or has made an error in or omission from any return or other document submitted to the U.S. government, the practitioner is obligated to advise the client promptly of the facts of such noncompliance, error, or omission. The practitioner must also advise the client of the consequences of such noncompliance, error, or omission as provided under the Internal Revenue Code and regulations.

CIRCULAR 230 • Diligence as to Accuracy: A practitioner must exercise due diligence as to the accuracy of all returns, documents, other papers, and oral or written representations which relate to IRS matters. If the practitioner relies on the work product of another person, he/she will be presumed to exercise due diligence if the practitioner has used reasonable care in engaging, supervising, training, and evaluating the person, taking into account the nature of the relationship between the practitioner and the person. • Prompt Disposition of Pending Matters: A practitioner may not unreasonably delay the prompt disposition of any matter before the Internal Revenue Service. • Assistance from Disbarred or Suspended Persons: A practitioner may not knowingly accept assistance regarding IRS matters, either directly or indirectly, from any person who is under suspension or disbarment from practice before the Internal Revenue Service.

CIRCULAR 230 • Notaries: A practitioner may not act as a notary public with respect to any matter administered by the IRS if the practitioner is also employed by the client regarding IRS matters or is in any way interested in the matter pending before IRS. • Fees: A practitioner may not charge unconscionable fees. Generally, a practitioner is not allowed to charge a contingent fee for tax return preparation or other matters before the IRS. A contingent fee is a fee that is based on a percentage of the refund reported on a return, or is otherwise dependent on the result obtained. However, contingent fees are allowed in the following situations: Services rendered in connection with an examination or other challenge to a taxpayer’s original return. Services rendered in the preparation of an amended return or claim for refund or credit which is filed within 120 days of the taxpayer receiving a notice of examination or a written challenge to the return. Services rendered in connection with a claim for refund or credit regarding the determination of interest and penalties assessed by the IRS. Services rendered in connection with any judicial proceeding arising under the Internal Revenue Code.

CIRCULAR 230 • Return of Client’s Records: A practitioner is obligated to promptly return, upon request, any and all records that belong to the client, or that the client needs to comply with his/her federal tax obligations. The practitioner may retain copies of the records returned to the client. A dispute over fees does not relieve the practitioner of this responsibility. (There is an exception, where allowed by state law, whereby the practitioner may retain the records subject to the fee dispute, but must provide the client with reasonable access to review and copy the records.) The practitioner is not required to release returns or other documents which have been prepared by the practitioner or the practitioner’s firm if the return or document is being withheld due to the client’s nonpayment of fees with respect to that return or document.

CIRCULAR 230 • Conflicting Interests: A practitioner shall not represent a client before the IRS if the representation involves a conflict of interest. A conflict of interest exists if the representation of one client will be directly adverse to another client. There is also a conflict of interest if there is a significant risk that the representation of a client will be materially limited by the practitioner’s responsibilities to another client, a former client or a third person, or by the practitioner’s own personal interests. A practitioner may reasonably believe that he/she will be able to provide competent and diligent representation to clients where a potential conflict of interest exists. The clients may consent to such representation if it is not prohibited by law. Each affected client must waive the conflict of interest and give informed consent in writing within 30 days after being informed of the conflict. The practitioner must retain copies of the written consents for at least 36 months after the conclusion of the representation of the affected clients, and must provide those consents upon request to any officer or employee of the IRS.

CIRCULAR 230 • Solicitations: A practitioner may not advertise or solicit clients, either publicly or privately, in any manner that could be considered false, fraudulent, misleading, deceptive, or coercive. Any uninvited solicitation must clearly identify the solicitation as such, and also identify the source of information used in choosing the recipient. If a practitioner publishes a fee schedule, he/she may not charge more than the published fees for at least 30 days after the last date of publication. The practitioner must retain a copy of any communication containing fee information, along with a list or description of persons to whom the communication was distributed. The practitioner must retain these copies for at least 36 months after they were last used. This applies to all methods of communication – mailings, e-mails, radio, television, flyers, telephone directories, and all others.

CIRCULAR 230 • Clients’ Refund Checks: A practitioner who prepares tax returns may not endorse or otherwise negotiate any check issued to a client by the government with respect to a federal tax liability. • Best Practices: Tax professionals should adhere to best practices when preparing tax returns or other documents or providing advice regarding federal tax matters. In addition to compliance with standards, best practices include the following: • Communicating clearly with clients and having a clear understanding with clients as to the scope of advice and assistance being given. • Establishing the facts, determining which facts are relevant, evaluating the reasonableness of any assumptions, relating the facts to the applicable law, and arriving at conclusions that are supported by the law and the facts. • Advising clients regarding the importance and potential consequences of the conclusions reached, including the avoidance of penalties if the taxpayer relies on the advice. • Acting fairly and with integrity in the conduct of your business. • Developing procedures to ensure best practices are followed by all members, associates, and employees of the firm.

CIRCULAR 230 • Standards with Respect to Tax Returns: Circular 230 establishes certain standards with respect to tax returns and other submissions to the Internal Revenue Service. A tax professional may NOT: • Advise a client to take a position on a return or document submitted to the IRS unless the position is not frivolous. • Advise a client to submit a document to the IRS for the purpose of impeding or delaying

CIRCULAR 230 • Advise a client to submit a document to the IRS for the purpose of impeding or delaying administration of federal tax laws. • Advise a client to submit a return or document that is frivolous. • Advise a client to submit a return or document that contains or omits information in a manner that demonstrates an intentional disregard of a rule or regulation (unless the client is also advised to submit documents that evidence a good faith challenge to the rule or regulation). • In order to comply with standards, a tax professional must: • Inform a client of any penalties that may reasonably apply to a position taken on a tax return, if the practitioner gave advice regarding the position or prepared or signed the tax return. • Inform a client of any opportunity to avoid penalties by disclosure, and of the requirements of adequate disclosure.

CIRCULAR 230 • A tax professional may generally rely in good faith without verification upon information furnished by the client. However, a practitioner may not ignore the implications of information furnished by the client or otherwise known by the practitioner. If the information provided by the client appears to be incorrect, inconsistent, or incomplete, the professional must make reasonable inquiries to obtain reliable information. • Giving Written Advice: When giving written advice to a client, a tax professional may NOT: • Base the advice on unreasonable factual or legal assumptions; • Unreasonably rely on the representations or statements of the taxpayer or any other person; • Ignore or fail to consider all relevant facts that the professional knows or should know; or • Take into account the risk of being audited or having the advice challenged by the IRS.

CIRCULAR 230 Incompetence and Disreputable Conduct: Incompetence and/or disreputable conduct may subject a tax professional who is authorized to practice before the IRS to sanctions for violation of the regulations. Incompetent and/or disreputable acts include the following: Conviction of any criminal offense under the federal tax laws. Conviction of any criminal offense involving dishonesty or breach of trust. Conviction of any felony under federal or state law which would render a practitioner unfit to practice. Knowingly giving false or misleading information to the Department of the Treasury or its officers or employees. Soliciting employment or attempting to deceive a client or prospective client using false or misleading representations, or intimating that the practitioner is able to obtain special consideration or action from the IRS or its officer or employee. Willfully failing to file a federal tax return, or participating in evading or attempting to evade any assessment or payment of any federal tax. Willfully assisting, counseling, or encouraging a client or prospective client to violate any federal tax law, or knowingly counseling or suggesting to a client or prospective client an illegal plan to evade federal taxes.

CIRCULAR 230 • Misappropriation or failure to remit funds received from a client for the purpose of paying taxes or other government obligations. • Directly or indirectly trying to influence the official action of any IRS officer or employee by the use of threats, false accusations, duress or coercion, or by offering or promising gifts, favors, or anything of value. • Disbarment or suspension from practice as an attorney, certified public accountant, public accountant, or actuary by any state or other U.S. jurisdiction. • Knowingly aiding and abetting another person to practice before the IRS during a period of suspension, disbarment, or other period of ineligibility. • Contemptuous conduct in connection with practice before the IRS, including the use of abusive language or malicious or libelous communications. • Knowingly, recklessly, or through gross incompetence giving a false opinion on questions arising under Federal tax laws. • Willfully failing to sign a tax return prepared by the practitioner. • Willfully disclosing or otherwise using a tax return or tax information in a manner not authorized by the Internal Revenue Code.

CIRCULAR 230 • Confidentiality, Privacy, and Disclosureof Financial or Tax Information • Citizens have a right to expect professionals who assist them with private financial matters to be trustworthy. The accounting and tax professional has an obligation to maintain and respect the confidentiality of information obtained in the performance of all professional activities. The Gramm-Leach-Bliley Act of 1999 requires each financial institution and tax preparer to disclose its privacy policy to those who trust them with nonpublic personal information. • In general, the tax preparer’s privacy policy should state that nonpublic personal information is not disclosed without the client’s consent. Any exceptions should be explained in the privacy policy. The following are some common exceptions that a tax preparation firm should explain in its privacy policy: Disclosure to employees, technical advisors, software consultants, or electronic filing providers. Disclosures required to comply with federal, state, or local laws, or with licensing requirements. Disclosures required to comply with legal subpoenas or other legal actions. The Internal Revenue Service also has requirements regarding the disclosure of tax information. These requirements are found in Revenue Procedure 2008-35, published in the Internal Revenue Bulletin on July 21, 2008. Section 7216(a) of the Internal Revenue Code imposes criminal penalties on tax return preparers who knowingly or recklessly make unauthorized disclosures or uses of information furnished in connection with the preparation of a tax return. Any disclosure or use of tax information requires the informed consent of the taxpayer.

Due Diligence It probably doesn’t mean that practitioners must use all measures possible to verify all information that client provides but the scope of our investigations has broadened. It would be likely that facts and circumstances would be considered.

Letter to Client Due to the tighter standards imposed by the new rules, the cost of providing written tax opinions will likely be higher unless the disclaimer approach is taken.

Firm Responsibilities Effective for all members, associates and employees there must be a conformity with Circular 230.

Tax Return Preparation Tax return should not be signed as preparer if it contains a position that does not have a realistic possibility of being sustained on its merits. Audit roulette does not count. Does it have a one in three chance (or greater) of being sustained on its merits. If position is improper it is frivolous. Preparers must make taxpayers aware of the penalties involved.

Penalties Reckless violation or incompetence is grounds for censure, suspension or disbarment from practice. All information, hearings, pleadings, evidence, reports decisions will be made available to the public.

Changing Face of Return Prep SBWOTA changes Substantial or Gross valuation misstatement >$5,000 penalties to 20% or 40%, respectively unless: Substantial authority or Adequately disclosedandreasonable basis.

Understatement of Tax Liability by Return Preparers Prior • 1st Tier penalty $250 for Income Tax preparer if: • Not disclosed; Not ‘realistic possibility’ (1/3) • 2nd Tier penalty if willful neglect; $1,000 preparer penalty

Tax return preparer penalties • Old Law: An income tax return preparer is liable for penalties for failing to have a reasonable factual or legal basis for a position taken on a return. • Evolved into a "realistic possibility of success" standard, as a one-in-three chance of prevailing on the merits of an issue.

Tax return preparer penalties • If the position did not meet the realistic possibility of success an income tax preparer could avoid the penalty for non-frivolous positions through adequate disclosure. • Only subject to the penalty if an understatement arose as the result of : (1) a nondisclosed position that failed to meet the "realistic possibility of success" standard, or (2) a disclosed position that was frivolous.

Understatement of Tax Liability by Return Preparers Now: • ANY return prepared > 5/27/07 • More Likely Than Not sustained (51%+) 1st Tier is greater of $1,000 or 50% of fees • 2nd Tier is greater of $5,000 or 50% of fees • Change effectively applies penalties, due to understatement of taxpayer liability, to preparers ofALLreturns (Gift, Estate, 941, Excise, 990-T, W-2’s, 1099’s)

New Preparer Penalty Legislation • Undisclosed Positions: Preparer may be subject to penalties even though the taxpayer would not as a result of an understatement. • Standard for Taxpayers: Substantial Authority • Standard for Practitioners: Higher level, was a realistic possibility of success, now is MORE LIKELY THAN NOT, (more than 50% likely to succeed)

New Preparer Penalty Legislation • New Law: Return preparer is subject to a penalty of up to 50% of the fees for the assignment if: - the position was not disclosed and the return preparer did not have a reasonable belief that the position was more likely than not correct, or - the position was disclosed but did not have a reasonable basis.

New Preparer Penalty Legislation • Accounting firms may be forced to change the Engagement letters, Organizer Letters and even the Circular 230 disclaimer on e-mails and memoranda advising clients to disclose any position that does not meet the "more likely than not" standard. • Notice 2007-54 delayed application for all returns filed before 2008.

New Preparer Penalty Legislation • Tax professionals should react with caution to this change in the law. • It has been suggested that some practitioners in order to protect themselves may disclose every position taken on a return on Form 8275 rather than risk the penalty. Line-by-line basis, that there is no certainty that each number reflected on the return is more likely than not correct……….. • AICPA Urged Congress to Reconsider….see article in Sept Journal Of Accountancy, page 25.

Are YOU willing to GAMBLE$1,000 or 50% of professional fees for………. • 1099 issued to individual in lieu of Form W-2? • Asset is held for investment versus sale? • Expense capitalized versus deducted? • Form W-2 issued to self-employed member (partner) of LLC (partnership)? • Value of non-cash charitable contributions? • Basis of asset sold? • Worthlessness of a Stock or Debt? • ClaimingReal Estate Pro when not? • Unreasonably LOW compensation of S shareholder? • Business Miles driven by taxpayer?

Getting the records and proof from clients: don’t trust your client too much • Suggested solutions for consideration Document, document, document!!! • Form 8275 - Disclosure Statement – Disclose a position contrary to a rule such as a statutory position or IRS revenue ruling.

IRS advice: avoid the ‘Dirty Dozen’ tax scams of 2009 • Phishing • Economic Stimulus Payments • Frivolous Tax Arguments- taxes are illegal • Fuel Tax Credit Scams • Hiding Income Offshore • Abusive Roth IRAs • Zero Wages • False claims for refunds and abatements • Return Preparer Fraud • Disguised Corporate Ownership • Trust Misuse • Use of Charitable Organizations to shield income

Update on Circular 230 1. In general, Treasury Department proposed changes to Circular 230 on March 6, 2006 2. What is a contingent fee? Fee based in whole or part on a position taken on a tax return; includes refund or reimbursement of fees Cannot charge contingent fee on Original Can charge contingent free on: Amended return, exam of original return, or judicial proceeding

Tax Return Preparation • 230 regs forbid practitioners from signing a return that contains a position that does not have ‘realistic possibility’ of being sustained. • Generally 1-in-3 or better chance of being sustained. • ‘Risk of audit’ cannot be considered. • Disclosure to client of potential penalties • Disclosure of position on return? IRS sanctions include censure, suspension, or disbarment from practice before IRS.

New Preparer Penalties Update • Standard is now “MLTN” or >50% • Applies to all tax returns • IRS Notice 2008-13 • May rely on good faith upon information furnished by T/P or 3rd party • You don’t have to audit your clients • Make reasonable inquiries • Do not ignore other information you may have

Pension Protection Act Penalties 1. Thresholds for accuracy related penalties reduced - From 200% to 150% for Substantial valuation misstatement (20% penalty) - From 400% to 200% for Gross valuation misstatement (40% penalty) 2. Appraisal penalties increased - $1,000 or 10% of tax understatement - Max = 125% x appraisal fee unless ‘more likely than not’ correct appraisal

Accuracy Related Penalty NOTE: Per the IRS general instructions: The portion of the accuracy-related penalty attributable to the following types of misconduct cannot be avoided by disclosure on Form 8275: • Negligence • Disregard of rules or regulations • Any substantial understatement of income tax • Any substantial valuation misstatement • Any substantial overstatement of pension liabilities • Any substantial estate or gift tax valuation understatements