Download

1 / 43

430 likes | 579 Views

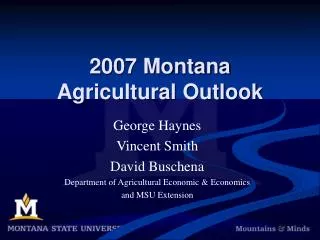

2013 Agricultural Commodity Outlook. Iowa Chapter of ASFMRA Annual Meeting Ames, Iowa Feb. 7, 2013 Chad Hart Associate Professor/Grain Markets Specialist chart@iastate.edu 515-294-9911. Cattle Crush Margin. The Crush Margin is the return after the feeder steer and corn costs.

E N D

2013 Agricultural Commodity Outlook Iowa Chapter of ASFMRA Annual Meeting Ames, Iowa Feb. 7, 2013 Chad Hart Associate Professor/Grain Markets Specialist chart@iastate.edu 515-294-9911

Cattle Crush Margin The Crush Margin is the return after the feeder steer and corn costs. Live weight: 1250 pounds Feeder weight: 750 pounds Corn: 50 bushels per head Source: ISU Extension

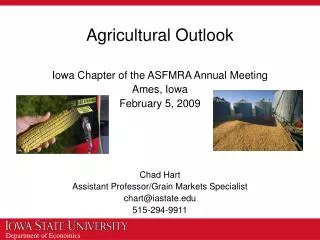

Hog Crush Margin The Crush Margin is the return after the pig, corn and soybean meal costs. Carcass weight: 200 pounds Pig price: 50% of 5 mth out lean hog futures Corn: 10 bushels per pig Soybean meal: 150 pounds per pig Source: ISU Extension

U.S. Meat Production & Prices Source: USDA-WAOB

U.S. Corn Supply and Use Source: USDA-WAOB

U.S. Soybean Supply and Use Source: USDA-WAOB

Projected Corn Yields Top: 2012 Yield Bottom: Change from 2011 Units: Bushels/acre

Projected Soybean Yields Top: 2012 Yield Bottom: Change from 2011 Units: Bushels/acre

World Corn Production Source: USDA-WAOB

World Soybean Production Source: USDA-WAOB

World Weather Source: USDC and USDA

Corn Export Shifts Source: USDA-FAS

Soy Export Shifts Source: USDA-FAS

U.S. Blended Gasoline Consumption 7.6 bil. gal. 7.4 bil. gal. Source: DOE-EIA, via USDA-ERS

Current Corn Futures 6.78 5.57 5.37 Source: CME Group, 2/5/2013

Current Soybean Futures 14.18 12.82 12.44 Source: CME Group, 2/5/2013

Total Acreage Shift Source: USDA-NASS

Acreage Shift by Crop Acreage change from 2011 Units: 1,000 acres Source: USDA-NASS

Acreage Shift by State Top: Planted in 2012 Bottom: Change from 2011 Units: 1,000 acres Source: USDA-NASS

Thoughts for 2013 and Beyond • Supply/demand concerns • Soil moisture issues • Biofuel and export strength • Worldwide response to drought-induced pricing • Risk management • Crop insurance • Price protection

Thank you for your time!Any questions?My web site:http://www.econ.iastate.edu/~chart/Iowa Farm Outlook:http://www.econ.iastate.edu/ifo/Ag Decision Maker:http://www.extension.iastate.edu/agdm/