Download

1 / 14

140 likes | 234 Views

The Credit Crisis. Raghuram Rajan Chicago Booth School of Business. Outline. The Crisis: Origins The Impact Resolving the crisis? Regulatory Lessons. Bad Investments. Child of past crises Emerging markets => Industrial country corporations => Industrial country household

E N D

The Credit Crisis Raghuram Rajan Chicago Booth School of Business

Outline • The Crisis: Origins • The Impact • Resolving the crisis? • Regulatory Lessons

Bad Investments • Child of past crises • Emerging markets => Industrial country corporations => Industrial country household • Sophisticated Financial Sector • Effectively sold mortgages from Phoenix, Arizona to buyers around the world • $ 100 sub-prime mortgages generated $ 80 AAA • Originate to distribute spreads risks but • Quality of originations weakened • Depended on house price rising

Bad Investments contd. • Banks held on to poor quality assets • Poor governance and risk management • At the top • Through the organization • Tail risk • Writing earthquake insurance • Where were the risk managers?

Financed with short term debt • Short term debt cheaper because • Lenders better protected. • Rolling over financing is easy in good times. • Market requires banks to hold little capital because losses remote. • Aided and abetted by Fed policy • Greenspan “put”

The Impact: Sequence of events • House price stops rising • Mortgage Defaults=> MBS fall in value, become more difficult to price, and price becomes more volatile • Market for mortgage backed assets dries up. • Illiquidity • Potential Insolvency • More hits on their way • Credit cards • Commercial real estate • Commercial and industrial loans

Credit markets freeze • Banks unwilling to sell impaired assets • Banks unwilling to substitute for shadow financial system • Worries about borrower credit risk. • Worries about own liquidity if lenders want money back. • Worries about likely fire sales pushing securities prices further down – common discount rate for risky assets • Banks unwilling to raise enough equity • Stability is not the major focus of the private sector in the midst of a crisis! • Institutional overhang not a major problem right now because demand for credit low. But will hamper recovery.

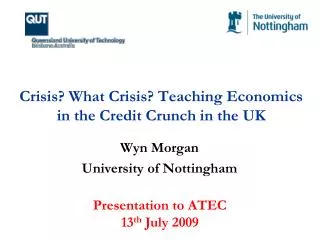

Declining credit asset prices pull equity prices downwards ABX.07-1 AAA versus BKX* index prices

When will credit markets find a bottom? • When the risk of large institutions collapsing is small. • Guarantee debt • Audit institutions (the Stress Test) • Clean up bank balance sheets by isolating/selling problem assets • Good bank/bad bank • Recapitalize banks through a mix of private and public funds • Some actions may have to be mandated • This will allow asset prices to recover and credit to flow more freely, thus not impeding recovery. • Will require more public money: political support weak

3 Lessons for financial regulation • Regulators and markets are subject to the same euphoria that bankers are. Over the cycle • the market becomes less risk averse, so regulatory arbitrage increases • enforcement as well as risk management get weaker. • How do you ensure regulations have bite? • Illiquidity is contagious. Problems can emerge from anywhere and hit elsewhere. • Stability is a public good in the midst of a crisis, with limited private incentive to help create it.

Implications • Heavy handed, focused, regulation will most likely to lead to arbitrage, without insulating sensitive areas. • Bright lines? Utilities? • Lighter, across-the-board, regulation with contingent escalation of regulatory powers and actions more useful. • No matter what regulators do, disaster can always strike. Create private sector buffers that will not be eroded in good times.

A problem • Large complex entities! • Break them up? • Slow their growth (higher capital and supervision)? • Limit their growth? • Force them to become easier to fail.

T Thank You!