Download

1 / 4

E N D

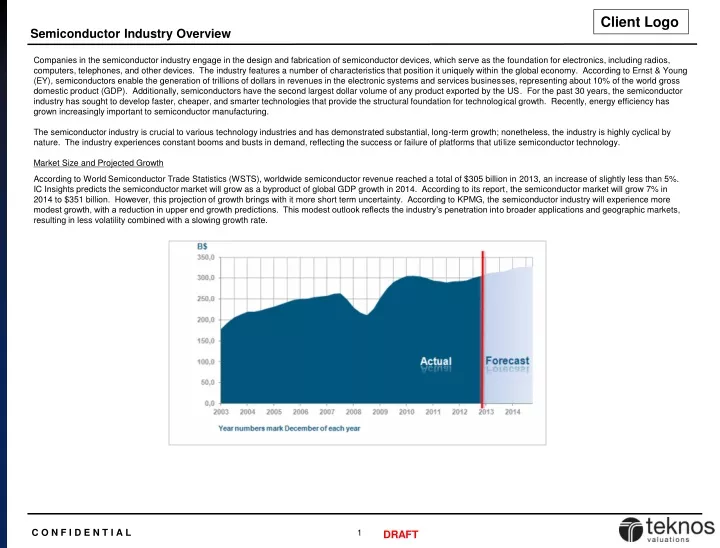

Semiconductor Industry Overview Companies in the semiconductor industry engage in the design and fabrication of semiconductor devices, which serve as the foundation for electronics, including radios, computers, telephones, and other devices. The industry features a number of characteristics that position it uniquely within the global economy. According to Ernst & Young (EY), semiconductors enable the generation of trillions of dollars in revenues in the electronic systems and services businesses, representing about 10% of the world gross domestic product (GDP). Additionally, semiconductors have the second largest dollar volume of any product exported by the US. For the past 30 years, the semiconductor industry has sought to develop faster, cheaper, and smarter technologies that provide the structural foundation for technological growth. Recently, energy efficiency has grown increasingly important to semiconductor manufacturing. The semiconductor industry is crucial to various technology industries and has demonstrated substantial, long-term growth; nonetheless, the industry is highly cyclical by nature. The industry experiences constant booms and busts in demand, reflecting the success or failure of platforms that utilize semiconductor technology. Market Size and Projected Growth According to World Semiconductor Trade Statistics (WSTS), worldwide semiconductor revenue reached a total of $305 billion in 2013, an increase of slightly less than 5%. IC Insights predicts the semiconductor market will grow as a byproduct of global GDP growth in 2014. According to its report, the semiconductor market will grow 7% in 2014 to $351 billion. However, this projection of growth brings with it more short term uncertainty. According to KPMG, the semiconductor industry will experience more modest growth, with a reduction in upper end growth predictions. This modest outlook reflects the industry’s penetration into broader applications and geographic markets, resulting in less volatility combined with a slowing growth rate. Worldwide Semiconductor Billings 1

Semiconductor Industry Overview (continued) • Segment Analysis • The semiconductor industry can be divided into four primary segments: (1) discrete, (2) optoelectronics, (3) sensors, and (4) integrated circuits (ICs). Of these segments, the IC segment is by far the largest, representing approximately 84% of the total market. Below is a description of each segment along with its projected market size. • Discrete – these typically perform a single function in electronic circuits, the purpose of which is switching, amplifying, or transmitting electrical signals. WSTS expects this segment to grow steadily to $19 billion in 2014. • Optoelectronics – these are electrical/optical transducers that use different technological processes than integrated circuits or discrete semiconductors. The growth of this segment is dependent on the growth of digital cameras. In 2014, the optoelectronics segment is estimated to generate revenue of $29 billion. • Sensors – these sense physical variables and convert them into electrical signals. The need for sensors is fueled by mobile applications (smartphones, tablets, and wearable devices) and automotive purposes. This segment is expected to grow to just under $9 billion in 2014. • Integrated circuits – these are miniature electronic circuits that integrate a large number of tiny transistors into a small chip. This market is composed of several sub-segments, including analog, memory, micro, and logic components. This segment is expected to grow to more than $255 billion billion in 2014. Regional Analysis The Asia Pacific region, which includes China, India, and South Korea, continues to expand its already dominant hold of the global semiconductor industry. As of 2013, 58% of the global semiconductor sales came from the Asia Pacific region. The Americas, Europe, and Japan account for the rest of the market, with each region representing between 12% and 19% of the global market. Europe and the Asia Pacific region lead the way in estimated growth for 2014, with expected growth rates of 4% and 6%, respectively. With low manufacturing costs and large domestic demand, the Asia Pacific region continues to attract foreign investment. According to Gartner, continued growth in China, rapid growth in India, and the emergence of new markets in countries such as Vietnam and Thailand are important contributors to the growth of the regional market. 2

Semiconductor Industry Overview (continued) • End-Market Demand • Semiconductors have several applications spanning multiple industries. Below is a list of the semiconductor end-markets with a description of main growth drivers. • Data processing market – this market has generated strong demand from emerging countries and sales in the enterprise sector. Mobile computing platforms are expected to drive market expansion. In addition, the growth of cloud computing and the increase in data centers may contribute to growth in this market. • Consumer electronics market – products such as LCD TVs and blu-ray players are major drivers of revenue within the consumer electronics market. Looking forward, EY expects a global trend of switching from analog to digital TV broadcasting, which should fuel growth in high-resolution TVs and digital set top boxes. • Automotive industry – this industry uses semiconductors for navigation, monitoring tire pressure, sensing path obstacles, fuel efficiency, and more. All of these technologies drive the growth of electronic content in vehicles. Semiconductors for automobiles tend to generate revenue for several years, providing a stable future growth profile for the semiconductor market. • Communications – the proliferation of mobile devices, which use analog chips and microcontrollers for wireless communication, has driven semiconductor growth in recent years. According to the International Data Corporation (IDC), key benefits for this sector include higher connectivity, increased storage, and multimedia-enabled handsets and smartphones. • Industrial – energy-efficient and environmentally-friendly technology drive the growth in the industrial market. The top semiconductor components in this sector include logic, digital signal processing (DSPs), and microcontrollers (MCUs). • Trends • Though consumer electronics and computers were historically the drivers of industry growth, the popularity of these product segments has paved the way for other products and areas of growth. According to EY, popular areas of growth include energy efficiency, sensors and detectors, smartphones and media tablets, embedded intelligence, and high-performance application processors. • Energy Efficiency: In an effort to cut energy use and reduce energy waste within the semiconductor industry, the United States government is partnering with the private sector to finance innovative, energy efficient semiconductor technologies. For example, RF Micro Devices (RFMD) plans to develop gallium-nitride semiconductor technology, which is predicted to be a $334 million industry by 2017, according to Strategic Analytics. This initiative is expected to reduce carbon dioxide emissions by 14 billion tons, saving the United States more than $3 billion in energy spending. • Sensors and Detectors: According to Research and Markets, the market for sensors, detectors, and analyzers exceeded $2 billion in 2014 and is projected to continue a trend of growth. For example, the global market for gas detection is projected to reach more than $3 billion by the 2018, with a compound annual growth rate (CAGR) of more than 4%. In addition, sensors and detectors are prominently featured in tablets, smartphones, and wearable devices. Within these platforms, semiconductor-dependent applications are capable of detecting heart rate, motion, acceleration, and altitude. • Smartphones and Tablets: As the technological environment continues to transition away from desktop computers towards mobile devices, smartphones, and tablets will be a key driver of semiconductor growth. According to the IDC, semiconductor revenue for 4G phones experienced an annual growth rate of more than 121% in 2013 and a CAGR of 38% from 2012 to 2017. The IDC predicts the semiconductor industry’s overall consumer revenue will have a CAGR of 5% from 2012 to 2017, with smartphones and tablets dominating this segment. 3

Semiconductor Industry Overview (continued) Embedded Intelligence: According to Zacks Investment Research, the implementation of “The Internet of Things” and embedded technologies will allow for new avenues of growth within the semiconductor industry. For example, software defined networking (SDN), smart grids, and intelligent metering applications are expected to see particularly strong growth in 2014, with a 19% CAGR through 2016, according to IC Insights. High-Performance Application Processors: High performance application processors, a system on a chip (SoC) designed to support mobile applications, are key structural components for applications that make smartphones and tablets marketable. These high-end processors enable the performance and storage required for creating new and advanced applications, including context-aware computing, augmented reality, and computational photography. Overview Because revenue for the semiconductor industry is reflective of global GDP and the overall demand for platforms utilizing semiconductor technology, short-term growth has been cyclical. During times of economic prosperity, the semiconductor industry experiences increased corporate and consumer spending. During economic downturns, semiconductor revenues are strained as corporate technology budgets are trimmed and consumers are more hesitant towards purchasing the newest semiconductor-equipped technologies. According to Value Line, as a product of this cyclical nature and the ever-shortening product lifecycles, the semiconductor industry will continue to experience intense competition and volatility. In addition to issues of industry volatility, associated with semiconductor modernization and globalization are various legislative challenges that must be addressed to ensure industry stability, including the need to facilitate open markets, the protection of intellectual property, streamlined export control regulations, improved security and authentication of semiconductor products, and continued support for sustainable, innovative development. Despite the temporary lulls in the industry’s growth and potential policy challenges in the future, the semiconductor industry will remain the structural foundation for technological innovation and a key contributor to the globalization of innovative technology. 4