Download

1 / 34

340 likes | 541 Views

Affordable Care Act MAGI and non-MAGI. Session 2 Presented by Tokie Moriel & John Tvedt. Session Objectives. Define MAGI Discuss Key Points including: Countable income changes Household composition changes Verification procedures

E N D

Affordable Care ActMAGI and non-MAGI Session 2 Presented by Tokie Moriel & John Tvedt DHS/DFO/IMTA/2013-07-15

Session Objectives • Define MAGI • Discuss Key Points including: • Countable income changes • Household composition changes • Verification procedures • Explain how SSI-related (non-MAGI) coverage is affected under ACA DHS/DFO/IMTA/2013-07-15

Definition of MAGI • Modified Adjusted Gross Income (MAGI) • Tax based methodology • Earned & Unearned Income • Household Composition • 5% income disregard • No other income deductions, diversions or disregards • Effective Dates • Applications – January 1, 2014 • Renewals – March 31, 2014 DHS/DFO/IMTA/2013-07-15

Tax Definitions of MAGI • Family - Taxpayer (includes married taxpayers filing jointly) and all claimed tax dependents • Family size - Number of individuals in the family • Household income - The sum of the taxpayer’s MAGI plus the MAGI of tax dependents in the family if required to file DHS/DFO/IMTA/2013-07-15

MAGI-Based Methodologies • Align financial eligibility rules across all insurance affordability programs • Seamless and coordinated system of eligibility and enrollment • Maintain eligibility of low-income populations, especially children DHS/DFO/IMTA/2013-07-15

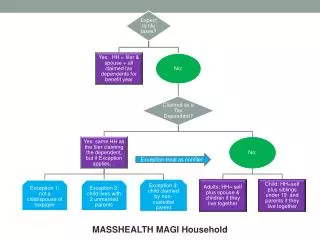

Whose Eligibility is Based on MAGI? DHS/DFO/IMTA/2013-07-15

Medicaid and CHIP Exempt Income under MAGI • Child support income received is not counted • Depreciation of business expenses, including capital losses will also not be counted • Scholarships, fellowship grants and awards used for education purposes • Worker’s compensation • Veteran’s benefits • American Indian and Alaska Native (AI/AN) income derived from distributions, payments, ownership interests, and real property usage rights • Non-recurring lump sum DHS/DFO/IMTA/2013-07-15

Medicaid and CHIPHH Comp Changes under MAGI • Taxpayers and tax dependents use tax household with limited exceptions • Parents, children and siblings are included in same household • Stepparents and parents treated the same • Children and siblings with or without income included in same household as rest of family • Older children included in family if claimed as tax dependent by parents • Child income does not count if child not required to file a tax return DHS/DFO/IMTA/2013-07-15

Rules for Non-filers • Rules for non-filers parallel those for filers • Spouses/parents and children living together in the same household • No distinction between biological, adopted or step-children nor between biological or step-parents • “Children” include individuals under 19 DHS/DFO/IMTA/2013-07-15

Establishing Filing Requirements and Tax Dependency Relationships • Filing requirements and tax dependency based on reasonable expectations at time of determination • If taxpayer cannot reasonably establish tax dependency relationship, inclusion of tax dependent in household determined in accordance with non-filer rules DHS/DFO/IMTA/2013-07-15

How is MAGI Verified? • Electronic data matches • Validation of data • Reasonable compatibility standard DHS/DFO/IMTA/2013-07-15

MAGI Budget Period (“Point in Time”) • Cost sharing reductions and premium tax credits for coverage through Exchange based on annual income • Medicaid and CHIP eligibility is based on current monthly income • Iowa will continue calculating income based on known fluctuations if it is indicative of future projected income as in the case of seasonal workers DHS/DFO/IMTA/2013-07-15

Scenario 1 – Jones Family The General Rule Applied • John and Joan Jones are married. They file jointly and claim Joan’s son by a first marriage, JP, age 17, as a tax dependent • John and Joan together currently earn $2,300 per month, with projected annual income of $27,600 • Joan’s ex-husband pays $500 per month in child support • JP works part-time earning roughly $135 per month DHS/DFO/IMTA/2013-07-15

Scenario 1 – Jones Family • Tax and Medicaid Household is John, Joan and JP • Child support income is exempt and not counted • JP’s income is not countable because it is below the filing threshold requirement for dependents DHS/DFO/IMTA/2013-07-15

Scenario 1 – Jones Family The family’s income should fall within the FPL ranges where: • John and Joan are potentially eligible for cost sharing reductions and premium tax credits through the marketplace • JP is potentially eligible for CHIP DHS/DFO/IMTA/2013-07-15

Scenario 2 – John Doe Differences in Treatment of Income • John is a single parent with 2 children, ages 6 and 10, whom he claims as tax dependents • John earns $3,000 per month, with projected annual income of $36,000 • John also receives $1,800/year ($150/mo) in taxable AI/AN income DHS/DFO/IMTA/2013-07-15

Scenario 2 – John Doe • Tax and Medicaid household is John and 2 children • Household income for: • Medicaid/CHIP is $3000/month • Marketplace is $37,800/annual DHS/DFO/IMTA/2013-07-15

Scenario 2 – John Doe The family’s income should fall within the FPL ranges where: • John is potentially eligible for cost sharing reductions and premium tax credits through the marketplace • Both children are potentially eligible for CHIP DHS/DFO/IMTA/2013-07-15

Scenario 3 – Lewis Family Differences in HH Composition • Mary Lewis is a working grandmother who claims her daughter (Samantha), age 20 and a full-time student, and granddaughter (Joy), age 2, as tax dependents • Mary earns $4,500/month ($54,000/year) • Samantha earns $300/month ($3,600/year) DHS/DFO/IMTA/2013-07-15

Scenario 3 – Lewis Family • Tax household is Mary, Samantha and Joy • Medicaid/CHIP households are: • Mary’s is the same as tax household of Mary, Samantha and Joy • Samantha’s is the same as Mary’s household of Mary, Samantha and Joy • Joy’s only includes Joy and her mother Samantha (exception: non-filer rules apply) DHS/DFO/IMTA/2013-07-15

Scenario 3 – Lewis Family • Household income for Mary and Samantha: • Medicaid/CHIP is $4800/month • Marketplace counts the same income as Medicaid or $57,600/annual • Household income for Joy: • Medicaid/CHIP is $300/month ELIAS will automatically apply the 5% disregard when necessary. DHS/DFO/IMTA/2013-07-15

Scenario 3 – Lewis Family The family’s income should fall within the FPL ranges where: • Mary and Samantha are potentially eligible for premium tax credits through the marketplace • Joy is potentially eligible for Medicaid DHS/DFO/IMTA/2013-07-15

Non-MAGI • Non-MAGI includes the following people: • Individuals who are age 65 or older, blind, disabled, or eligible for or enrolled in Medicare • Individuals with long-term care needs • Eligibility for Medicare cost sharing assistance DHS/DFO/IMTA/2013-07-15

MAGI-Exempt • MAGI exempt includes: • Anyone for whom agency not required to make income determination including, but not limited to: • IV-E Foster Care and Subsidized Adoption • FMAP-related MN • BCCT • Newborns DHS/DFO/IMTA/2013-07-15

MAGI-Exception for 65+ • Exception applies when age (65+) is a condition of eligibility • Current methods apply when determining eligibility for group covering individuals age 65 and older • MAGI methods applied in determining eligibility of a caretaker relative regardless of the age of the caretaker relative DHS/DFO/IMTA/2013-07-15

Eligibility on Non-MAGI Basis • Individuals who are eligible for a mandatory coverage group based on MAGI may still choose to have eligibility determined under a non-MAGI coverage group using non-MAGI eligibility standards (e.g., for disabled individuals, LTC needs) DHS/DFO/IMTA/2013-07-15

MAGI Screen • If an individual meets criteria for eligibility based on MAGI, they must be promptly enrolled • State must pursue eligibility on non-MAGI basis if: • Individual indicates potential for eligibility on other basis on single streamlined application • Individual submits application designed for non-MAGI eligibility • Individual requests such determination • Agency otherwise has information indicating such potential eligibility DHS/DFO/IMTA/2013-07-15

MAGI-Screen (con’t) • If the agency has information indicating potential eligibility on another basis or at the individual’s request, we must request additional information needed to make a determination on a non-MAGI basis. Individual is not required to provide information needed by the agency to complete an eligibility determination on a non-MAGI basis • Enrollment based on MAGI proceeds pending completion of the non-MAGI determination DHS/DFO/IMTA/2013-07-15

MAGI-Screen (con’t) • If disability is confirmed, the individual must be enrolled in a non-MAGI group if otherwise eligible and MAGI eligibility is discontinued. If not eligible, such as over resources then MAGI eligibility may continue • If not eligible on non-MAGI basis individual remains eligible in MAGI-based group DHS/DFO/IMTA/2013-07-15

John Jones Scenario • John is a single 25-year old living on his own • He has some medical conditions, but he is able to hold down a part-time job, and earns $1,000/month • He submits the single streamlined application online and indicates his need for supportive services • The State has a HCBS waiver program which could potentially meet John’s needs DHS/DFO/IMTA/2013-07-15

John Jones Eligibility based on MAGI • Medicaid MAGI household of one • Based on John’s income he is eligible for Medicaid with an FPL of 100% DHS/DFO/IMTA/2013-07-15

John Jones Eligibility on non-MAGI Basis • Because John has indicated a need for specialized services which may be covered under the State’s waiver program, agency needs to request additional information from John to determine his eligibility for that program • The agency will need to provide John with the information he needs to decide whether to complete the non-MAGI determination • Pending completion of the determination of eligibility for the waiver program, John will remain enrolled through the adult group DHS/DFO/IMTA/2013-07-15

John Jones Eligibility on non-MAGI Basis • If John is determined eligible for the waiver program, he must enroll in that program • If John does not provide all information needed to determine eligibility for the waiver program or the State determines he is not eligible, he will remain in the adult group DHS/DFO/IMTA/2013-07-15

Conclusion • Additional ACA webinars • Session review – Income Maintenance Workers ONLY DHS/DFO/IMTA/2013-07-15