Download

1 / 26

260 likes | 263 Views

Explore the factors contributing to the decline in the US personal saving rate and its implications for the country's future growth, retirement planning, and economic dependence. Consider the importance of private saving, data revisions, and the impact of capital gains on wealth accumulation.

E N D

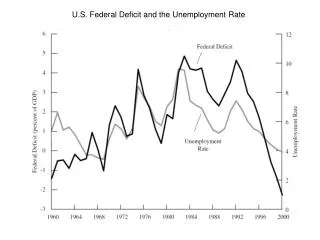

The U.S. Saving Rate • The U.S. personal saving rate declined throughout the 1980s and 1990s • Personal saving/disposable personal income • Does it matter?

Concerns • Fed vice-chair Roger Ferguson: “The fall in the personal saving rate could have important implications for the ability of the country to finance investment in plant and equipment, for future growth in productivity and real incomes, and for our growing economic dependence on other countries to finance our spending patterns.”

Concerns • Cleveland Fed researcher Jagadeesh Gokhale argued that “low saving by U.S. households may adversely impact their ability to maintain their living standards during retirement—a challenge that will only gain in difficulty with lengthening life spans.”

3 Reasons Not to Worry • private saving, not personal saving, is the relevant measure of saving • the personal saving rate may be revised upward in the future • the personal saving rate ignores the capital gains that people earn, and is thus a misleading measure of the increase in their net worth.

Look at private saving • Private saving, not personal saving, is more appropriate • Private saving = business saving + personal saving, since people own businesses and thus own their saving

Look at private saving • Looking at private saving • The decline in the 1980s and 1990s is not as steep as in the personal saving rate • Recent increases in business saving are large and drive the private saving rate almost as high as in the 1960s

Data revisions • The personal saving rate is revised substantially • In August 1999, I said “The personal saving rate turned negative recently for the first time ever”

Data revisions • In May 2002, I said “The personal saving rate turned negative recently for the first time ever”

Data revisions • In May 2007, I said “The personal saving rate turned negative recently for the first time ever; but I am getting this strange feeling of déjà vu”

Data revisions • The personal saving rate is revised substantially • Today, I say, “The personal saving rate has never been negative!”

Data revisions • Why is the personal saving rate revised so much? • Income is not measured well at first: government tends to underestimate it • Since saving is measured as income minus consumption, then underestimates of income lead to measured savings that are too low

Data revisions • On average the personal saving rate is revised up by 3 percentage points! • So, if you think it is 5% initially, it is probably 8%.

Capital Gains • The biggest problem, though, is that the personal savings rate ignores capital gains (and thus changes in wealth) • This is by design, since NIPA is designed to deal with economic activity (production) • But then we shouldn’t use it to estimate changes in a stock variable, such as wealth

Capital Gains • What we should really care about is the change in people’s wealth, not their saving • In the 1990s, people had huge wealth gains, and consumed more, which showed up as a declining savings rate, since their spending increased faster than their incomes

Capital Gains • The group of households whose personal saving rate declined in the 1990s is exactly the same group of households who received capital gains from owning stock—those in the top 20% of the income distribution. • Poorer households, those in the bottom 40% of the income distribution, increased their saving rate in the 1990s

Capital Gains • Milt Marquis: “To a large extent the low personal saving rate in the U.S. economy is a systematic response of households to changes in its fundamental determinants, most notably the increase in financial wealth.”

Implications • Changes in the saving rate over time mainly reflect changes in the net worth of households • The decline in net worth/disposable income from 6.3 in mid-2007 to 4.7 in early-2009 led households to save more • Households are in about the same position today that they were in the early 1990s; it would not be surprising if this level of savings persisted