Download

1 / 21

E N D

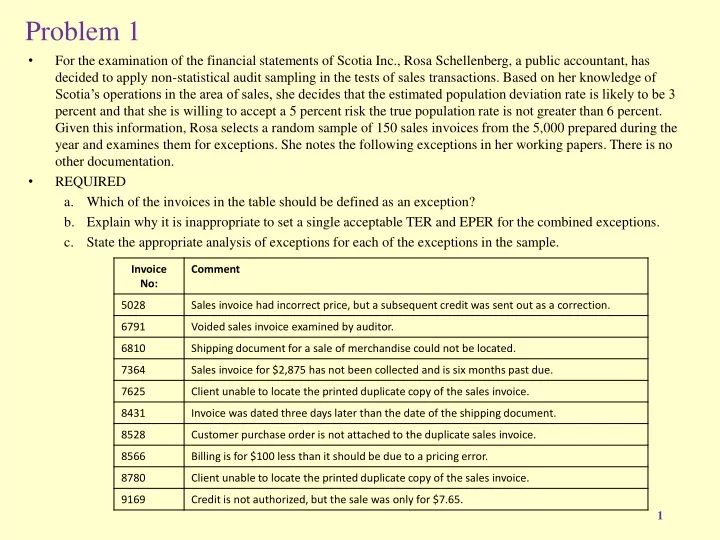

Problem 1 For the examination of the financial statements of Scotia Inc., Rosa Schellenberg, a public accountant, has decided to apply non-statistical audit sampling in the tests of sales transactions. Based on her knowledge of Scotia’s operations in the area of sales, she decides that the estimated population deviation rate is likely to be 3 percent and that she is willing to accept a 5 percent risk the true population rate is not greater than 6 percent. Given this information, Rosa selects a random sample of 150 sales invoices from the 5,000 prepared during the year and examines them for exceptions. She notes the following exceptions in her working papers. There is no other documentation. REQUIRED Which of the invoices in the table should be defined as an exception? Explain why it is inappropriate to set a single acceptable TER and EPER for the combined exceptions. State the appropriate analysis of exceptions for each of the exceptions in the sample.

Solution a. b. It is inappropriate to set a single acceptable tolerable exception rate and estimated population exception rate for the combined errors because each attribute has a different significance to the auditor and should be considered separately in analyzing the results of the test.

c. For each exception, the auditor should check with the controller to determine his explanation for the cause. In addition, the appropriate analysis for each type of exception is as follows:

Problem 2note: good segregation of duties has the receptionist prepare a prelisting of cash receipts when they are received in the mail You have been asked to do planning for statistical testing of the audit of cash receipts. Following is a partial audit program for the audit of cash receipts. Review the cash receipts journal for large and unusual transactions. Trace entries from the prelisting of cash receipts to the cash receipts journal to determine whether each is recorded. Compare customer name, date, and amount on the prelisting with the cash receipts journal. Examine the related remittance advice for entries selected from the prelisting to determine whether cash discounts were approved. Trace entries from the prelisting to the deposit slip to determine whether each has been deposited. REQUIRED Identify which audit procedures can be tested using attribute sampling. Justify your response. State the appropriate sampling unit for each of the tests in part (a). Define the attributes that you would test for each of the tests in part (a). State the audit object associated with each of the attributes. Define exception conditions for each of the attributes that you have described in part (c). Which of the exceptions would be indicative of potential fraud? Justify your response.

Solution It would be appropriate to use attributes sampling for all audit procedures except audit procedure 1. Procedure 1 is an analytical procedure for which the auditor is doing a 100% review of the entire cash receipts journal. The appropriate sampling unit for audit procedures 2-5 is a line item, or the date the prelisting of cash receipts is prepared. The primary emphasis in the test is the completeness objective and audit procedure 2 indicates there is a prelisting of cash receipts. All other procedures can be performed efficiently and effectively by using the prelisting.

Problem 3 – Attribute Sampling Lenter Supply Corp. is a medium sized distributor of wholesale hardware supplies in southern Manitoba. It has been a client of yours for several years and has instituted excellent internal control for the control of sales, at your recommendation. In providing control over shipments, the client has prenumbered “warehouse removal slips” that are used for every sale. It is company policy never to remove goods from the warehouse without an authorized warehouse removal slip. After shipment, two copies of the warehouse removal slip are sent to billing for the computerized preparation of a sales invoice. One copy is stapled to the duplicate copy of the prenumbered sales invoice, and the other copy is filed numerically. In some cases more than one warehouse removal slip is used for billing one sales invoice. The smallest warehouse removal slip number for the year is 14682 and the largest is 37521. The smallest invoice number is 47821 and the largest is 68507. In the audit of sales, one of the major concerns is the effectiveness of the control in making sure all shipments are billed. The auditor has decided to use attribute sampling in testing internal control.

State an effective audit procedure for testing whether shipments have been billed. What is the sampling unit for the audit procedure? • A random selection of warehouse removal slips should be made • Examined to see if they have the proper sales invoice attached • The sampling unit will be the warehouse removal slip • Assuming the auditor expects no deviations in the sample but is willing to accept a TDR of 3%, at a 10% RIA, what is the appropriate sample size? • TDR = 3% • RIA = 10% (Beta Risk) • EPDR (Expected Population Deviation Rate) = 0 • As auditor expects no deviations

Sample Size – CAS 530 • R = nP • R is the PPS Factor determiner from a PPS table. • n is the sample size • P is the precision or Tolerable Deviation Rate • The auditor also needs to know the Expected Population deviation Rate (EPDR) • Usually obtained from last years audit sampling results • Use and EPDR of 0. i.e. the auditor expects no deviations

Given a confidence level of 90% and TDR of 3% • With and EPDR of 0, R = 2.31 • Thus n = R/P = 2.31/0.03 = 77.

The following table is from the text, Appendix 10A. Beta risk or risk of incorrect acceptance. The risk of accepting an account as materially accurate when it is in fact materially misstated. More audit work would actually be needed and it is not performed. Alpha risk or risk of incorrect rejection. The risk of rejecting an account as materially accurate when it is in fact not materially misstated. This would require more audit work when it is really not needed.

EPDR Sample size

n = n’ 1 + n’/N Effect of population size -Initial sample size only -Possible to make adjustment to initial sample size based on overall population size -Finite correction factor n = revised sample size n’ = initial sample size N = population size

From the problem Population is 37521 – 14682 + 1 = 22840 n’ = 77/(1+(77/22840)) = 76.74 Thus revised sample size is still 77 the population has very little effect

Use of a random number table • A one-to-one correspondence between warehouse removal slip • How is this correspondence achieved? • Random stab in the random number table

Population of Warehouse Removal Slips 14,682 – 37,521 Random Stab Random Number Table

Upper Exception Limit (UEL) or CUER or Computed Upper Exception Rate • Sample size = 100 • TER = 3% • RIA = 10% • Number of deviations = 1 • Using the following tables: • UEL = 3.8% • Are the controls working? No, UEL > TER