Download

1 / 0

10 likes | 218 Views

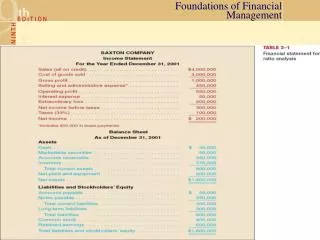

Similarities and Differences Module 4 – Cost Control. Rural Hospital Profitability. CAH. PPS. Profit Formula. CAH. PPS. Revenue per patient - Cost per patient Profit per patient To increase profits a business must: Increase revenues Decrease expenses. Cost Benefits of a CAH. CAH.

E N D