Download

1 / 37

380 likes | 396 Views

Home Insurance. Important Insurance Terms. Risk – Chance of loss or injury Peril – Anything that may cause a loss Hazard – Anything that increases the likelihood of loss through peril Negligence – Failure to take ordinary or reasonable care to prevent accidents. Risk Management Methods.

E N D

Important Insurance Terms • Risk – Chance of loss or injury • Peril – Anything that may cause a loss • Hazard – Anything that increases the likelihood of loss through peril • Negligence – Failure to take ordinary or reasonable care to prevent accidents

Risk Management Methods • Risk Avoidance • Avoid risks, but may have serious trade-offs • Can avoid traffic accident by not driving, but may not be able to get to work • Risk Reduction • Decrease the likelihood of harm or risk • Can reduce accident injury by wearing a seatbelt

Risk Management Methods • Risk Assumption • Taking responsibility for negative results of a risk • Makes sense to assume risk when the possible loss is small like not fully insuring an old car • Self-insurance is another option; set up a savings acct. to cover loss • Risk Shifting • Use an insurance company • May have a deductible, a combination of risk assumption and shifting, which is a set amount the policyholder must pay on a loss

Property and Liability Insurance • Natural disasters as well as injuries and property damage cost billions of dollars a year • Two types of risk related to home • 1) Risk of damage to or loss of property • 2) Risk of responsibility for injuries to other people or damage to their property

Property and Liability Insurance • Property Damage or Loss • Two basic types of risks for property owners • Physical damage such as wind, fire, flooding • Loss or damage caused by criminal behavior such as robbery, burglary, vandalism, and arson • Liability • Legal responsibility for the financial cost of another person’s losses or injuries, even is it is not your fault • Usually found responsible because negligence on your part helped cause the mishap

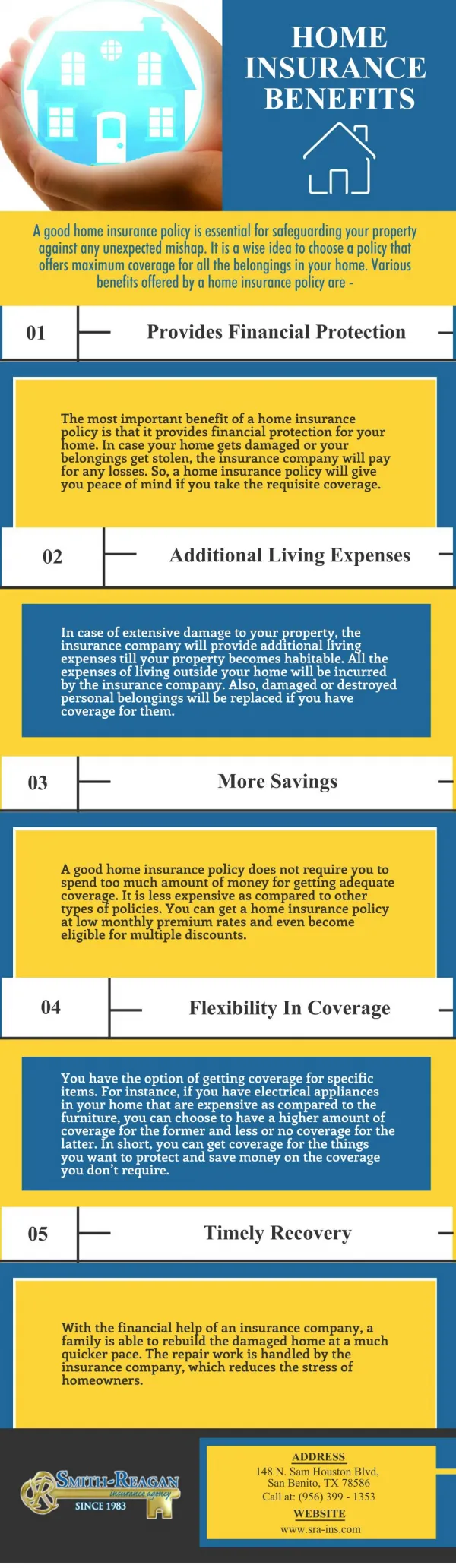

Homeowners Insurance • A binding, legal contract between the insured and the insurer to protect their home and belongings if they are damaged or destroyed • Provides against losses caused by fire, water damage, storms, theft, and other perils • Provides against monetary losses as a result of negligence for medical bills, legal fees, death benefits

Who/What Do HO Policies Protect? • Anyone named in the policy • Spouse • Children • Other residents • Guests • Also covers garages, sheds, pools, landscaping

What isn’t Protected • Cars, boats, ATVs – things that would have its own insurance • One of a kind items like jewelry, art, and collections – must purchase additional coverage for these items • In areas prone to natural disasters, additional coverage is needed

Renter’s Insurance • Protects those who live in a “home” owned by someone else • Inexpensive to purchase • Covers your belongings which are not covered under the owners insurance • Protects against theft, loss of personal property, and loss of use

What Renters Insurance Covers • Covers • Personal possessions • Loss of use (pays for you to live elsewhere) • Medical payments for those injured there • Doesn’t Cover • Structural damage caused by carelessness

Homeowners Policies • Most homeowners insurance are package policies with the following coverages • Property/Structure • Property/Personal belongings • Liability protection • Loss of use

Property/Structure Coverage • Repair or rebuild your home if damaged or destroyed by fire, hurricane, hail, lightning or other disasters listed in your policy • Will not pay for damage caused by a flood, earthquake or routine wear and tear • Always purchase enough coverage to rebuild your home

Property/Personal Belongings Coverage • Furniture, clothes, and personal items stolen or destroyed by insured disasters • Most cover 50-70% of the cost of your dwelling limit, so if your house is insured at $200,000, and they pay 50%, the payout limit would be $100,000 • Covers items you take on vacation or use at school

How Much Will You Get? • Actual Cash Value vs Replacement Cost • Actual cash value only pay for what the property was worth at the time of the loss (depreciated value) • Replacement cost coverage will pay what it actually costs to replace the items you lost • Both involve paying a deductible first

Liability Insurance • Protects you when you are at fault or sued • Covers bodily injury for those hurt at your home • Covers property damage liability for damage done to building or belongings • Most policies cover behavior of household pets

Loss of Use Insurance • Pays for you to stay somewhere else while home is being rebuilt or repaired • May limit coverage to 10 to 20% of home’s total coverage • May limit the payment period to 6 to 9 months

Personal Property Floaters • Extra coverage for valuable items • Jewelry • Furs • Fine arts • Musical instruments • Collections • Guns

Household Inventories • Documentation of personal belongings with purchase dates and cost information • Should keep receipts, serial numbers, brand names, proof of value • Video of home including closets and storage areas • Photographs with dates and values on back • Keep in fireproof box or safe deposit box and update regularly

Personal Liability and Related Coverages • Amounts of coverages • Most policies cover liability up to $100,000 • Supplement with an umbrella policy to add protection for all kinds of personal injury claims – if someone sues you for slander (writing or saying something untrue) • More expensive policies are available for the wealthy • Medical payments coverage pays cost of minor accidental injuries to visitors on your property • Supplemental coverage could cover damage you do to other people’s property

What Isn’t Covered • Jewelry, furs, boats, electronics • Animals and fish • Motorized vehicles not licensed for road use, except those used for home maintenance • Sound devices in motor vehicles • Aircraft parts • Property belonging to tenants • Property in rentals • Business property

Other Coverages • Credit card fraud, check forgery, counterfeit money • Removal of damaged property • Emergency removal of property to protect it from damage • Temporary repairs after a loss to prevents further damage • Fire department user fees

How much coverage do you need? • 80% to full coverage for homes • Must have coverage if borrowing money from bank • Coverage for personal belongings is usually 55 to 75% of insurance you have on your home • Claim settlements • Actual cash value – receive replacement cost minus depreciation • Replacement value – receive full cost of repairing or replacing item

Home Insurance Cost Factors • Location – water supply, fire hydrant, crime, weather • Type of Structure – wood, brick • Price, Coverage Amount, Policy Type – higher deductible means lower premiums • Home Insurance Discounts – smoke detectors, fire extinguisher, dead bolts • Company Differences – compare companies

Location • Those close to water supply or hydrant get discount • Those near high crime, severe weather pay more

Lower Deductibles • Decreases cost because insurance company pays less out because you are assuming more financial reasonability

Discounts • Smoke detectors • Fire extinguisher • Deadbolts • Alarm system

Selecting Insurance Companies • Consider prices, but also service and coverage • Not all settle claims in the same way

Attractive Nuisances • An attractive nuisance is an object, structure or condition that is both dangerous and irresistibly inviting or intriguing to children. • Name some attractive nuisances

What is an Attractive Nuisance • Unenclosed swimming pool, goldfish pool, idling lawnmower, paint sprayer, table saw, construction sites, and equipment • Most natural conditions are not considered attractive nuisances • To be liable for injury, an owner must create or maintain the harmful object • Attractive nuisance doctrine arises when the child doesn’t realize the extent of the danger

Typical Local Laws • Pools – fences and locks • Discard Refrigerators – removal of doors • Fences – barbed wire below a certain height • Old Cars and Other Junk – must be fenced in • Chemicals – discard of pesticides, paints, etc. • Dangerous Dogs

Landowner can be held responsible if a child is injured by an "artificial condition" and all five of the following criteria are met: • 1) Landowner knows (or should know) that children are likely to trespass on the property • 2) The condition has the potential to cause death or serious bodily harm to children • 3) The children involved are too young or inexperienced to understand the risk presented by the condition

Landowner can be held responsible if a child is injured by an "artificial condition" and all five of the following criteria are met: • 4)The benefit of maintaining the condition or the cost required to remedy the condition is minimal compared with the risk to children. • 5)The landowner fails to take reasonable measures to eliminate the danger posed by the condition.

Who is Protected • Example 1 – 12 year old child climbed onto the roof of building and fell 3 stories to the ground. • Owner was liable because • 1. Children were known to play in area • 2. Roof had an area that was sloped and slippery – something a child might not notice • 3. Owner could’ve locked door to the rook

Who is Protected • Example 2 – A 10 year old fell 3 stories from a roof after climbing up and playing on it. • Owner was not liable because • 1. This owner had no reason to know that children would play on the roof • 2. No hidden danger on the roof itself caused the all

Who Is Protected • Example 3: During construction of a house, a contractor left sheetrock propped against a wall and unattended. An 11 year old girl investigating the building site was injured when the sheetrock tumbled down on her. • Owner was liable because: • 1. Children were likely to come onto the building site • 2. The sheetrock was left unattended for days • 3. It could have easily been stacked in a safer manner