Download

1 / 29

310 likes | 449 Views

The Continuous Limit of Markov Switching GARCH Carol Alexander & Emese Lazar, ICMA Centre. Workshop on Statistical Modelling of Complex Systems M ünchen , 2006. Outline. Introduction Motivation Literature on the continuous limit of GARCH ( Nelson , Corradi)

E N D

The Continuous Limit ofMarkov Switching GARCHCarol Alexander & Emese Lazar, ICMA Centre Workshop on Statistical Modelling of Complex Systems München, 2006 Carol Alexander & Emese Lazar, ICMA Centre, 2006

Outline • Introduction • Motivation • Literature on the continuous limit of GARCH (Nelson, Corradi) • Continuous time limit of weak GARCH • Weak MS GARCH • Continuous limit of weak MS GARCH • Conclusions Carol Alexander & Emese Lazar, ICMA Centre, 2006

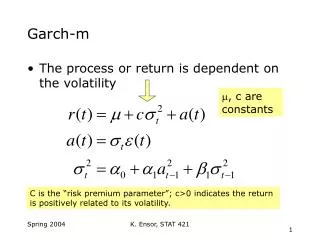

Introduction Normal GARCH(1,1)(Engle 1982, Bollerslev 1986): ht = the conditional variance of the residuals Carol Alexander & Emese Lazar, ICMA Centre, 2006

Motivation for the continuous time limit of GARCH • Many advantages to link discrete time modelling to continuous time modelling (GARCH option pricing) • We are interested in a stronger relationship between the two types of models (DT and CT) – an equivalence: • The limit of the DT model should be the CT model • Discretizing the CT model should give the DT model • Time aggregation is important because: if a model is not aggregating in time → then a different model will be valid for each frequency → but discretizing the CT model will give the same model for each frequency → contradiction Carol Alexander & Emese Lazar, ICMA Centre, 2006

Continuous limit of GARCH freedom to set the assumptions! Notation: Δω, Δα, Δβfor parameters using returns with step-length Δ - the returns and the conditional variance (normalized): Carol Alexander & Emese Lazar, ICMA Centre, 2006

Convergence theorems – which one? • Nelson (1990): Continuous-time limit: stochastic variance process with independent BM • Corradi (2000): Continuous-time limit: deterministic variance process Carol Alexander & Emese Lazar, ICMA Centre, 2006

Diffusion in variance? YES: • The variance of the variance is nonzero in discrete time, it should be the same in continuous time • Results from simulations • More intuitive NO: • GARCH has only one source of uncertainty in discrete time • The Euler discretization of Nelson’s limit model does not return the original GARCH model (but Taylor’s ARV model) • Nelson’s model cannot be extended to multi-state GARCH • GARCH and GARCH diffusion have non-equivalent likelihood functions (Wang, 2002) • Other papers: Duan et al. (2005), Brown et al (2002) Carol Alexander & Emese Lazar, ICMA Centre, 2006

Simulation results Carol Alexander & Emese Lazar, ICMA Centre, 2006

Weak GARCH Drost and Nijman (1993): ht = the best linear predictor (BLP) of the squared residuals Weak GARCH is aggregating in time! Carol Alexander & Emese Lazar, ICMA Centre, 2006

Simulated volatility smiles Volatility smiles generated by the weak GARCH, assuming θ = 0.05; ω = 0.0045; α = 0.1; μ(t) = 0; e(t) = 0; S0 = 100; V0 =0.09; T – t = 1; r = 0% 100 steps and 100,000 runs were used for the simulations (a) τ(t) = 0; η(t) = 3 (b) τ(t) = -1; η(t) = 5 (c) τ(t) = -1.5; η(t) = 10 Carol Alexander & Emese Lazar, ICMA Centre, 2006

Weak GARCH – inverse relationship • Drost and Nijman (1993) derive the low frequency parameters (ω, α and β) from the high frequency parameters • We inverse this relationship by deriving the high frequency parameters from the low frequency ones (also in Drost and Werker, 1996) • Then we compute the limit of the parameters as the time step converges to zero Carol Alexander & Emese Lazar, ICMA Centre, 2006

Weak GARCH – assumptions • There is no distributional assumption about the error process, having a general function for the unconditional kurtosis • Assumption 1: the kurtosis has a finite limit • Assumption 2: the BLP of the squared residuals converges at rate Δ to the conditional variance Carol Alexander & Emese Lazar, ICMA Centre, 2006

Conditional moments The conditional moments (normalized) are: Carol Alexander & Emese Lazar, ICMA Centre, 2006

Limit of weak GARCH –results Convergence rates for the parameters (proved): → also see Drost and Werker (1996) Continuous time model: Carol Alexander & Emese Lazar, ICMA Centre, 2006

Discretization - idea (in progress) → Time aggregation property is kept! Carol Alexander & Emese Lazar, ICMA Centre, 2006

Discretization - idea • The independent Brownian motion in the variance process is discretized as follows: • This is not normally distributed (chi-square instead), but it satisfies the basic properties required: Carol Alexander & Emese Lazar, ICMA Centre, 2006

Multi-state GARCH • They generally offer a better fit than single-state models, they can model time varying skewness and kurtosis • NM GARCH is a simplified version of MS GARCH where the transition matrix has rank 1 • However, NM GARCH does not have a continuous time limit (it is not a Lévy process), because it does not satisfy the stochastic continuity condition (the number of variance switches during a fixed period of time converges to infinity when the time step converges to zero – this is because the conditional probability of a switch does not change when the frequency changes): Carol Alexander & Emese Lazar, ICMA Centre, 2006

Normal mixture distribution • can model skewness & excess kurtosis; analytically tractable • Interpretation: • The normals give the different types of traders in the market • The normals give the different types of expectations in the market Carol Alexander & Emese Lazar, ICMA Centre, 2006

Markov Switching 0.9 0.8 State 1 small step large step 0.66 0.1 0.4 0.2 0.2 State 2 0.33 0.8 0.6 Carol Alexander & Emese Lazar, ICMA Centre, 2006

Markov switching GARCH • State indicator vector: • State probabilities = conditional expectations: • Transition matrix = help to form expectations: • We have: Carol Alexander & Emese Lazar, ICMA Centre, 2006

MS GARCH: 3 types • Cai (1994), Hamilon & Susmel (1994): Realized variance - leads to a non-recombining tree for the volatility process - estimation problems • Gray (1996), Klaassen (2002): Weighted average - analytically not too tractable; not intuitive • Haas, Mittnik & Paolella (2004): Its own lagged value - tractable - the variance series allowed to be more free from each other Carol Alexander & Emese Lazar, ICMA Centre, 2006

Realized volatility (simulated) Carol Alexander & Emese Lazar, ICMA Centre, 2006

Weak MS GARCH Based on Haas, Mittnik & Paolella (2004) and Drost and Nijman (1993): Carol Alexander & Emese Lazar, ICMA Centre, 2006

Weak MS GARCH • The GARCH component of the model is aggregating in time • Still, the model is not aggregating because multi-state models do not aggregate in time • Explanation: if for a time step Δ there are two states, then for a time step of length 2 Δ there would be 3 or 4 states • Another problem: Nelson’s assumptions cannot be generalized for this framework, so convergence rates similar to Corradi’s are used Carol Alexander & Emese Lazar, ICMA Centre, 2006

Weak MS GARCH Convergence rates for the parameters (proved): To achieve convergence, we must assume: Transition rate matrix: Carol Alexander & Emese Lazar, ICMA Centre, 2006

Limit of weak MS GARCH The limit model is: Carol Alexander & Emese Lazar, ICMA Centre, 2006

Properties • The framework can be extended to include the leverage effect similar to the AGARCH model of Engle and Ng (1993) • The state uncertainty for an option can be hedged using another derivative (only in a two-state world) • The market is arbitrage free, but incomplete • The discretization, however, would not return the original model Carol Alexander & Emese Lazar, ICMA Centre, 2006

Conclusions • Used the weak definition of GARCH to derive its ‘equivalent’ continuous time limit; the limit model has correlated brownians • Showed that there is no freedom to choose the convergence rates for the parameters; the weak definition implies the convergence rates • Defined the weak MS GARCH; for this only the GARCH component is aggregating in time and the relationship between the parameters for different frequencies is derived • Its continuous limit is very flexible, but it cannot (?) be discretized to return the original model • NM GARCH models do not have a continuous time limit Carol Alexander & Emese Lazar, ICMA Centre, 2006

Further questions • Are the assumptions realistic? Can they be proved? • Applications GARCH option pricing • What to do with the discretization problems? Carol Alexander & Emese Lazar, ICMA Centre, 2006