Download

1 / 16

160 likes | 258 Views

Vulnerable households in the owner occupied sector. Affordability Issues in Northern Ireland. Owner Occupation in Northern Ireland 1974-2011. Source: Northern Ireland House Condition Survey. Average house price by region: Nationwide Index.

E N D

Vulnerable households in the owner occupied sector Affordability Issues in Northern Ireland

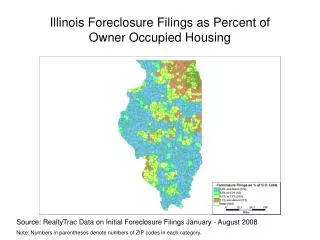

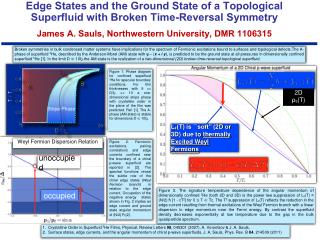

Owner Occupation in Northern Ireland 1974-2011 Source: Northern Ireland House Condition Survey

Average house price by region: Nationwide Index Source: www.nationwide.co.uk/hpi/downloads/All_prop.xls

NI Quarterly House Price Index: Average House Price 2003-2011 Source: Quarterly House Price Index

What the figures show… • Post-boom market adjustment is well advanced and Northern Ireland is in a more realistic position in terms of economic and household income fundamentals. …and hide • Headline figures hide local variation: stronger performance in Belfast and wider BMA. • The situation is relatively positive for first time buyers on a price-to-income ratio, but requirements remain for higher deposits. • Official base rates seem set to remain low, providing some comfort for those who have already purchased with a mortgage, but economic conditions, reductions in real household income and high levels of indebtedness present challenges, and ‘the level of arrears is significantly higher in some parts of the UK, for example in Northern Ireland, Wales and the North of England.’(FSA Retail Conduct Risk Outlook 2012)

Negative Equity FSA Prudential Risk Outlook 2011: • Based on residential mortgage sales between 2005 and 2010, NI had the lowest median loan-to-value at origination of all 12 UK regions (60.3%). However… • The estimated rate of negative equity (11.2%) was the highest in the UK. The UK average was 5.3%. • The indicators on ‘vulnerability to fiscal tightening’ showed areas of concern for Northern Ireland’s economy: e.g. 30% of total employment at Q3, 2010 was in the public sector (UK: 21%). HML analysis (Sept ’11): A further 10% fall in house prices could see 30% of all borrowers in NI in negative equity; also issue of age group affected.

Negative Equity • The scale of house price decline since 2007: Speaking on BBC Northern Ireland’s Spotlight, Professor Michael Moore of Queen’s University suggested that many households will be in negative equity for the full term of their mortgage. “There is going to be no recovery in the lifetime of any of the mortgages that currently exist”. • CML, August 2011: Of an estimated 826,800 negative equity cases in the UK, around 44,000 were in NI, which had the highest estimated negative equity rate of all regions (28% of all active mortgages advanced since 2005).

Actions and Orders for Possession Source: Northern Ireland Courts and Tribunals Service

Affordability Index Uses a typical bank/building society annuity formula to work out the maximum price that a household with a median household income could afford to pay, based on assumptions about a number of variables: • Maximum 35% of household income spent on mortgage costs • ‘Affordable’ home: price equivalent to first quartile (25th percentile) price of all homes sold during given period. • Typical interest rate: 3% (4.5% in 2008 version) • Loan-to-value ratio: 90% (95% in 2008) • A 25-year repayment period (unchanged)

The ‘Affordability Gap’ An indicator of the degree of difficulty experienced by first time buyers in repaying their mortgages: a negative figure indicates affordability problems.

Policy Responses • Co-Ownership: Northern Ireland’s regional shared ownership scheme. Increased funding from the NI Executive to enable 600 purchases annually, to 2014/15. • Pre-action protocol on possession proceedings: introduced for all mortgage possession cases in NI October 2009. • Mortgage Debt Advice Service: Initially a two-year pilot from May 2009, 755 clients sought advice through the service and 180 received advocacy and court representation which helped prevent homelessness. Funding was subsequently secured to deliver the service until March 2015.

Mortgage Rescue Scheme Out to consultation 2008; advice service and mortgage to rent/mortgage to flexible tenure (but not for households in negative equity). 2008-2011: Ministers for Social Development bid for funds to launch financial rescue element, without success. June 2011: Minister for Social Development “support[s] the ideals of a mortgage rescue scheme for Northern Ireland”, but emphasises that a full scheme: could cost £8.25 million over a two-year period; might only enable 72 ‘rescues’; and would impact on other budgets (e.g. health). March 2012: Reports that Minister has no plans to introduce a mortgage rescue scheme: it would not help enough people and would be too expensive to run. Policy Responses

“Headwinds” • Unprecedented house price growth and subsequent sharp decline has left a legacy of negative equity among households who purchased at the height of the housing price boom. • On a price-to-income basis, affordability has improved, but in uncertain economic times, the market remains slow and many households are taking a cautious approach. • More significant level of arrears and possessions than other UK regions (HML forecast: repossession rate of 1.08% in NI in 2012, compared with 0.25% in the South West of England).

For more information: • Quarterly House Price Index:www.nihe.gov.uk/index/corporate/housing_research/completed/house_price_index.htm • House Prices and Affordability Report:www.nihe.gov.uk/house_prices_and_affordability.pdf Research Unit Northern Ireland Housing Executive The Housing Centre 2 Adelaide Street Belfast BT2 8PB www.nihe.gov.uk