Download

1 / 69

690 likes | 902 Views

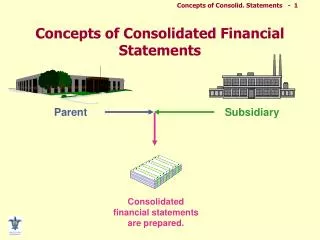

CONSOLIDATED STATEMENTS General Concepts. Same GAAP as separate statements Only external transactions Specific consolidation mechanics depend on Parent’s accounting for investment in subsidiary. CONSOLIDATION MECHANICS. Consolidation workpapers No “set of books” for consolidated entity

E N D

CONSOLIDATED STATEMENTSGeneral Concepts • Same GAAP as separate statements • Only external transactions • Specific consolidation mechanics depend on Parent’s accounting for investment in subsidiary

CONSOLIDATION MECHANICS • Consolidation workpapers • No “set of books” for consolidated entity • Each party maintains their own books • Eliminating entries • Necessary to eliminate “intercompany items” • Appear only on consolidation workpapers

INVESTMENT ELIMINATION • Investment account (Parent’s books) vs. Stockholders’ equity (Subsidiary’s books) • Treatment of the differential • Cost of the investment • FMV of subsidiary’s net assets (% acquired) • Book value of subsidiary’s net assets (% acquired)

INVESTMENT ELIMINATIONContinued • Positive differential (Cost vs. Book value) • Errors or omissions on subsidiary’s books • Excess of FMV over book value of subsidiary’s net assets • Existence of goodwill • Negative differential (Cost vs. Book value) • Errors or omissions on subsidiary’s books • Excess of book value over FMV of subsidiary’s net assets • Bargain purchase or “negative goodwill”

INVESTMENT ELIMINATIONContinued • Treatment of noncontrolling interest • Cost vs. Equity methods on Parent’s books • Intercompany receivables and payables • Valuation accounts at acquisition • Accumulated depreciation • Allowance for change in FMV of investment securities • Allowance for uncollectible accounts • Discount or premium on bonds payable • Negative Retained earnings of subsidiary at acquisition • Other stockholders’ equity accounts • Accounts accruing to common stock

Consolidation Workpaper Trial Balance Data Elimination Entries Account Titles Parent Subsidiary Debits Credits Consolidated Work flow

100% Purchase at Book Value Trial Balance Data Elimination Entries Account Titles Peerless Spec. Foods Debits Credits Consolidated Cash 50,000 50,000 100,000 Accounts Rec. 75,000 50,000 125,000 Inventory 100,000 60,000 160,000 Land 175,000 40,000 215,000 Bldg. and Equip. 800,000 600,000 1,400,000 Inv. in Sp. Foods 300,000(2)300,000 Total Debits 1,500,000 800,000 2,000,000 Accum. Depr. 400,000 300,000 700,000 Accounts Payable 100,000 100,000 200,000 Bonds Payable 200,000 100,000 300,000 Common Stock 500,000 200,000 (2)200,000 500,000 Retained Earn. 300,000100,000 (2)100,000 300,000 Total Credits 1,500,000 800,000 300,000 300,000 2,000,000

100% Purchase at Book Value Trial Balance Data Elimination Entries Account Titles Peerless Spec. Foods Debits Credits Consolidated Cash 50,000 50,000 100,000 Accounts Rec. 75,000 50,000 125,000 Inventory 100,000 60,000 160,000 Land 175,000 40,000 215,000 Bldg. and Equip. 800,000 600,000 1,400,000 Inv. in Sp. Foods 300,000 300,000 Total Debits 1,500,000 800,000 2,000,000 Accum. Depr. 400,000 300,000 700,000 Accounts Payable 100,000 100,000 200,000 Bonds Payable 200,000 100,000 300,000 Common Stock 500,000 200,000 200,000 500,000 Retained Earn. 300,000100,000 100,000 300,000 Total Credits 1,500,000 800,000 300,000 300,000 2,000,000

Purchase – Above Book Value (4) 340,000 (4) 40,000 (4)200,000 (4)100,000 Trial Balance Data Elimination Entries Account Titles Peerless Spec. Foods Debits Credits Consolidated Cash 10,000 50,000 Accounts Rec. 75,000 50,000 Inventory 100,000 60,000 Land 175,000 40,000 Bldg. and Equip. 800,000 600,000 Inv. in Sp. Foods 340,000 Differential Total Debits 1,500,000 800,000 Accum. Depr. 400,000 300,000 Accounts Payable 100,000 100,000 Bonds Payable 200,000 100,000 Common Stock 500,000 200,000 Retained Earn. 300,000100,000 Total Credits 1,500,000 800,000

Purchase – Above Book Value 380,000 380,000 Trial Balance Data Elimination Entries Account Titles Peerless Spec. Foods Debits Credits Consolidated Cash 10,000 50,000 Accounts Rec. 75,000 50,000 Inventory 100,000 60,000 Land 175,000 40,000 Bldg. and Equip. 800,000 600,000 Inv. in Sp. Foods 340,000 Differential Total Debits 1,500,000 800,000 Accum. Depr. 400,000 300,000 Accounts Payable 100,000 100,000 Bonds Payable 200,000 100,000 Common Stock 500,000 200,000 Retained Earn. 300,000100,000 Total Credits 1,500,000 800,000 (5) 40,000 (4) 340,000 (5) 40,000 (4) 40,000 (4)200,000 (4)100,000

Purchase – Above Book Value 60,000 125,000 160,000 255,000 1,400,000 2,000,000 700,000 200,000 300,000 500,000 300,000 2,000,000 380,000 380,000 Trial Balance Data Elimination Entries Account Titles Peerless Spec. Foods Debits Credits Consolidated Cash 10,000 50,000 Accounts Rec. 75,000 50,000 Inventory 100,000 60,000 Land 175,000 40,000 Bldg. and Equip. 800,000 600,000 Inv. in Sp. Foods 340,000 Differential Total Debits 1,500,000 800,000 Accum. Depr. 400,000 300,000 Accounts Payable 100,000 100,000 Bonds Payable 200,000 100,000 Common Stock 500,000 200,000 Retained Earn. 300,000100,000 Total Credits 1,500,000 800,000 (5) 40,000 (4) 340,000 (5) 40,000 (4) 40,000 (4)200,000 (4)100,000

to Balance Sheet section Comprehensive Three-Part Workpaper Trial Balance Data Elimination Entries Consoli- Item Parent Subsidiary Debits Credits dated Credit Accounts: Revenues Gains Debit Accounts: Contra Revenues Expenses Losses Net Income Beginning Retained Earnings Add: Net Income Deduct: Dividends Ending Retained Earnings INCOME STATEMENT SECTION RETAINED EARNINGS SECTION

From Retained Earnings Statement section Comprehensive Three-Part Workpaper Trial Balance Data Elimination Entries Consoli- Item Parent Subsidiary Debits Credits dated Debit Accounts: Assets Contra Liabilities Credit Accounts: Contra Assets Liabilities Stockholders’ Equity: Capital Stock Paid-in Capital Retained Earnings BALANCE SHEET SECTION

ELIMINATING ENTRIESFirst Subsequent Period(Equity Method) • Impact of current equity method entries • Ignore any impairment of goodwill • Assignment of income to noncontrolling interest • Investment account – Stockholders’ equity of subsidiary • Including identification of noncontrolling interest • Identification of differential • Allocation of differential • Depreciation/amortization of appropriate differentials • Impairment of goodwill

ELIMINATING ENTRIESFurther Subsequent Period(Equity Method) • Impact of current equity method entries • Ignore impairment of goodwill • Assignment of income to noncontrolling interest • Investment account – Stockholders’ equity of subsidiary • Retained earnings of subsidiary at BEGINNING of current year • Including identification of noncontrolling interest • Identification of REMAINING differential • Allocation of REMAINING differential • Including appropriate valuation accounts • Depreciation/amortization of appropriate differentials • Impairment of goodwill

20X1 Consolidation--100 Percent Ownership P 100% S Investment cost $300,000 Book value: Common stock--Special Foods $200,000 Retained earnings--Special Foods 100,000 $300,000 Peerless’s share x 1.00-300,000 Differential $ -0- January 1, 20X1 (1) Investment in Special Foods Stock 300,000 Cash 300,000 Record purchase of Special Foods stock.

20X1 Consolidation--100 Percent Ownership Peerless Special Products Foods Common Stock, January 1, 20X1 $500,000 $200,000 Retained Earnings, January 1, 20X1 300,000 100,000 20X1: Separate Operating Income, Peerless 140,000 Net Income, Special Foods 50,000 Dividends 60,000 30,000 20X2: Separate Operating Income, Peerless 160,000 Net Income, Special Foods 75,000 Dividends 60,000 40,000

$50,000 x 1.00 $30,000 x 1.00 20X1 Consolidation--100 Percent Ownership Peerless records its 20X1 income and dividends from Special Foods under the equity method with the following entries: (2) Investment in Special Foods Stock 50,000 Income from Subsidiary 50,000 Record equity-method income. (3) Cash 30,000 Investment in Special Foods Stock 30,000 Record dividends from Special Foods.

20X1 Consolidation--100 Percent Ownership Trial Balance Data Elimination Entries Consoli- Item Parent Subsidiary Debits Credits dated Income from Subsidiary 50,000 Dividends Declared (60,000 (30,000) Investment in Special Foods Stock 320,000 (4) 50,000 (4) 30,000(60,000) (4) 20,000 ) Remove both the investment income reflected in the parent’s income statement and the parent’s portion of any dividends declared by the subsidiary.

20X1 Consolidation--100 Percent Ownership Trial Balance Data Elimination Entries Consoli- Item Parent Subsidiary Debits Credits dated (5)100,000 300,000 (5) 300,000 (5) 200,000 500,000 Income from Subsidiary 50,000 (4) 50,000 Retained Earnings, January 1 300,000 100,000 Dividends Declared (60,000 (30,000 (4) 30,000 (60,000) Investment in Special Foods Stock 320,000 (4) 20,000 Common Stock 500,000 200,000 ) ) Remove the intercorporate ownership claim and stockholders’ accounts of the subsidiary as of the beginning of the period.

$75,000 x 1.00 $40,000 x 1.00 20X2 Consolidation--100 Percent Ownership Peerless records its 20X2 income and dividends from Special Foods under the equity method with the following entries: (6) Investment in Special Foods Stock 75,000 Income from Subsidiary 75,000 Record equity-method income. (7) Cash 40,000 Investment in Special Foods Stock 40,000 Record dividends from Special Foods.

20X2 Consolidation--100 Percent Ownership Trial Balance Data Elimination Entries Consoli- Item Parent Subsidiary Debits Credits dated Income from Subsidiary 75,000 Retained Earnings, January 1 430,000 120,000 Dividends Declared (60,000 (40,000 Investment in Special Foods Stock 355,000 (8) 75,000 (8) 40,000 (60,000) (8) 35,000 ) ) Remove the intercorporate ownership claim and stockholders’ accounts of the subsidiary recorded during the period.

20X2 Consolidation--100 Percent Ownership Trial Balance Data Elimination Entries Consoli- Item Parent Subsidiary Debits Credits dated Income from Subsidiary 75,000 (8) 75,000 Retained Earnings, January 1 430,000 120,000 Dividends Declared (60,000 (40,000 (8) 40,000 (60,000 Investment in Special Foods Stock 355,000 (8) 35,000 Common Stock 500,000 200,000 (9)120,000 430,000 (9) 320,000 (9) 200,000 500,000 ) ) ) Eliminate the beginning balance in the investment account and the stockholders’ equity accounts of the subsidiary at the beginning of 20X2.

ELIMINATING ENTRIESFirst Subsequent Period(Cost Method) • Impact of current cost method entries • Assignment of income to noncontrolling interest • Investment account – Stockholders’ equity of subsidiary • Including identification of noncontrolling interest • Identification of differential • Allocation of differential • Depreciation/amortization of appropriate differentials • Impairment of goodwill

ELIMINATING ENTRIESFurther Subsequent Period(Cost Method) • Impact of current cost method entries • Assignment of income to noncontrolling interest • Investment account – Stockholders’ equity of subsidiary • Retained earnings of subsidiary at ACQUISITION • Including identification of noncontrolling interest • Identification of REMAINING differential • Allocation of REMAINING differential • Including appropriate valuation accounts • Depreciation/amortization of appropriate differentials • Impairment of goodwill • Assign undistributed PRIOR earnings of subsidiary to noncontrolling interest

80% 20% NCI S 20X1 Consolidation--80 Percent Ownership Investment cost $240,000 Book value: Common stock--Special Foods $200,000 Retained earnings--Special Foods 100,000 $300,000 Peerless’s share x .80 -240,000 Differential $ -0- P January 1, 20X1 entry: (10) Investment in Special Foods Stock 240,000 Cash 240,000 Record purchase of Special Foods stock.

80 Percent Purchase at Book Value 240,000 200,000 100,000 80 Percent Purchase at Book Value Trial Balance Data Elimination Entries Account Titles Peerless Spec. Fd. Debits Credits Consolidated Cash 110,000 50,000 Accounts Rec. 75,000 50,000 Inventory 100,000 60,000 Land 175,000 40,000 Bldg. and Equip. 800,000 600,000 Inv. in Sp. Foods 240,000 Total Debits 1,500,000 800,000 Accum. Depr. 400,000 300,000 Accounts Payable 100,000 100,000 Bonds Payable 200,000 100,000 Common Stock 500,000 200,000 Retained Earn. 300,000 100,000 Total Credits 1,500,000 800,000 Nonctrl. Interest 60,000

80 Percent Purchase at Book Value 240,000 200,000 100,000 Trial Balance Data Elimination Entries Account Titles Peerless Spec. Fd. Debits Credits Consolidated Cash 110,000 50,000 Accounts Rec. 75,000 50,000 Inventory 100,000 60,000 Land 175,000 40,000 Bldg. and Equip. 800,000 600,000 Inv. in Sp. Foods 240,000 Total Debits 1,500,000 800,000 Accum. Depr. 400,000 300,000 Accounts Payable 100,000 100,000 Bonds Payable 200,000 100,000 Common Stock 500,000 200,000 Retained Earn. 300,000 100,000 Total Credits 1,500,000 800,000 Nonctrl. Interest 60,000 300,000 300,000

80 Percent Purchase at Book Value 240,000 700,000 200,000 300,000 500,000 300,000 60,000 2,060,000 200,000 100,000 Trial Balance Data Elimination Entries Account Titles Peerless Spec. Fd. Debits Credits Consolidated Cash 110,000 50,000 Accounts Rec. 75,000 50,000 Inventory 100,000 60,000 Land 175,000 40,000 Bldg. and Equip. 800,000 600,000 Inv. in Sp. Foods 240,000 Total Debits 1,500,000 800,000 Accum. Depr. 400,000 300,000 Accounts Payable 100,000 100,000 Bonds Payable 200,000 100,000 Common Stock 500,000 200,000 Retained Earn. 300,000 100,000 Total Credits 1,500,000 800,000 160,000 125,000 160,000 215,000 1,400,000 2,060,000 Nonctrl. Interest 60,000 300,000 300,000

20X1 Consolidation--80 Percent Ownership Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Income from Subsidiary 40,000 Dividends Declared (60,000 (30,000 Investment in Special Foods 256,000 (13) 40,000 (13) 24,000 (13)16,000 ) ) Peerless’s 80 percent share of Special Foods’ income and dividends is eliminated.

20X1 Consolidation--80 Percent Ownership Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Income to Non- controlling Int. Dividends Declared (60,000) (30,000) (13) 24,000 Noncontrolling interest . (14)10,000 (10,000) (14) 6,000(60,000) (14) 4,000 A separate entry establishes the amount of income allocated to noncontrolling shareholders and enters the increase in their claim on net assets of the subsidiary.

20X1 Consolidation--80 Percent Ownership Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Retained Earnings, January 1 300,000 100,000 Investment in Special Foods 256,000 (14) 16,000 Common Stock 500,000 200,000 Noncontrolling interest (14) 4,000 (15) 100,000300000 (15) 240,000 (15)200,000 500,000 (15) 60,00064,000 An entry is required to eliminate the stockholders’ equity accounts of the subsidiary and the investment account balance shown at the beginning of the period.

Second Year of Ownership--20X2 Peerless earns separate operating income of $160,000 and pays dividends of $60,000. In 20X2, Special Foods reports net income of $75,000 and pays dividends of $40,000.

$75,000 x .80 $40,000 x .80 20X2 Consolidation--80 Percent Ownership (16) Investment in Special Foods Stock 60,000 Income from Subsidiary 60,000 Record equity-method income. (17) Cash 32,000 Investment in Special Foods Stock 32,000 Record dividends from Special Foods.

20X2 Consolidation--80 Percent Ownership Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Income from Subsidiary 60,000 Dividends Declared (60,000 (40,000 Investment in Special Foods 284,000 (18)60,000 (18) 32,000 (18) 28,000 ) ) An entry is required to remove the income that Peerless has recognized from Special Foods, Peerless’s share (80 percent) of Special Foods’ dividends, and the change in the investment account that occurred in 20X2.

20X2 Consolidation--80 Percent Ownership Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Income to Non- controlling Int. Dividends Declared (60,000) (40,000) (18) 32,000 Noncontrolling Interest An entry is needed to assign $15,000 of subsidiary income to the noncontrolling shareholders, based on subsidiary income of $75,000 and a 20 percent noncontrolling interest.

20X2 Consolidation--80 Percent Ownership Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Income to Non- controlling Int. (19) 15,000(15,000) Dividends Declared (60,000) (40,000) (18) 32,000 (19) 8,000(60,000) Noncontrolling Interest (19) 7,000 An entry is needed to assign $15,000 of subsidiary income to the noncontrolling shareholders, based on subsidiary income of $75,000 and a 20 percent noncontrolling interest.

20X2 Consolidation--80 Percent Ownership Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Retained Earnings, January 1 420,000 120,000 Investment in Special Foods 284,000 (18) 28,000 Common Stock 500,000 200,000 Noncontrolling Interest (19) 7,000 An entry is required to eliminate the stockholders’ equity accounts of the subsidiary and the investment account balance reported by the parent at the beginning of the year and to establish the amount of the noncontrolling interest’s claim on the net assets of the subsidiary at the beginning of the year.

20X2 Consolidation--80 Percent Ownership Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Retained Earnings, January 1 420,000 120,000 (20) 120,000420,000 Investment in Special Foods 284,000 (18) 28,000 (20) 256,000 Common Stock 500,000 200,000 (20) 200,000500,000 Noncontrolling Interest (19) 7,000 (20)64,00071,000 An entry is required to eliminate the stockholders’ equity accounts of the subsidiary and the investment account balance reported by the parent at the beginning of the year and to establish the amount of the noncontrolling interest’s claim on the net assets of the subsidiary at the beginning of the year.

Investment cost $310,000 Book value: Common stock--Special Foods $200,000 Retained earnings--Special Foods 100,000 $300,000 Peerless’s share x .80-240,000 Differential $ 70,000 P 80% 20% NCI S Purchase at More Than Book Value Peerless Products purchases 80 percent of the common stock of Special Foods on January 1, 20X1, for $310,000.

Excess of cost over fair value of net identifiable assets (80%) $10,000 Total differential $70,000 Excess of fair value over book value of net identifiable assets (80%) $60,000 Purchase at More Than Book Value Cost of investment $310,000 Fair value of net identifiable assets $300,000 Book value of net identifiable assets (80%) $240,000

Purchase at More Than Book Value The entry to record Peerless Products purchasing Special Foods stock on January 1, 20X1 is: (21) Investment in Special Foods Stock 310,000 Cash 310,000 Record purchase of Special Foods stock.

Purchase at More Than Book Value In 20X1, Peerless Products earns income of $140,000 and pays dividends of $60,000. Special Foods reports net income of $50,000 and pays dividends of $30,000. (22) Investment in Special Foods Stock 40,000 Income from Subsidiary 40,000 Record equity method income: $50,000 x .80 (23) Cash 24,000 Investment in Special Foods Stock 24,000 Record dividends from Special Foods: $30,000 x .80

Purchase at More Than Book Value Entries are needed on Peerless’s books to recognize the write-off of the differential: (24) Income from Subsidiary 4,000 Investment in Special Foods Stock 4,000 Adjust income for differential related to inventory sold: $5,000 x .80 (25) Income from Subsidiary 4,800 Investment in Special Foods Stock 4,800 Amortize differential related to buildings and equipment.

20X1 Consolidation--80 Percent Ownership Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Income from Subsidiary 31,200 Dividends Declared (60,000) (30,000) Investment in Special Foods Stock 317,200 . (26)31,200 (26) 24,000 (26) 7,200 An entry is required to eliminate the subsidiary income.

20X1 Consolidation--80 Percent Ownership Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Income from Noncontrolling Interest Dividends Declared (60,000) (30,000) (26) 24,000 Noncontrolling Interest (27)10,000 (27) 6,000 (60,000) (27) 4,000 An entry is required to eliminate the subsidiary dividends.

20X1 Consolidation--80 Percent Ownership Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Retained Earnings, January 1 300,000 100,000 Investment in Special Foods Stock 317,200 (26) 7,200 Differential Common Stock 500,000 200,000 Noncontrolling Interest (27) 4,000 (28)100,000 300,000 (28) 310,000 (28) 70,000 (28) 200,000 500,000 (28) 60,000 64,000 An entry is required to eliminate the subsidiary dividends.

20X1 Consolidation--80 Percent Ownership Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Cost of Goods Sold 170,000 115,000 Land 175,000 40,000 Buildings and Equipment 800,000 600,000 Goodwill Differential (28) 70,000 (29) 4,000 289,000 (29) 8,000 223,000 (29) 48,000 1,448,000 (29) 10,000 (29) 70,000 An entry is needed to assign beginning differential.

20X1 Consolidation--80 Percent Ownership Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Depreciation 50,000 20,000 Goodwill Im- pairment Loss Goodwill (29) 10,000 Accumulated Depreciation 450,000 320,000 (30) 4,800 74,800 (31) 2,500 2,500 (31) 2,500 7,500 (30) 4,800 774,800 Entries are necessary to amortize the differential related to buildings and equipment and to write down the differential related to goodwill.

Consolidated Net Income, 20X1 Consolidated net income, 20X1: Peerless’s separate operating income $140,000 Peerless’s share of Special Foods net income: $50,000 x .80 40,000 Write-off of differential related to inventory sold during 20X1 - 4,000 Amortization of differential related to buildings and equipment - 4,800 Goodwill impairment loss -2,500 Consolidated net income, 20X1 $168,700