Download

1 / 88

880 likes | 886 Views

TWO VIEWS OF THE RELATIONSHIP BETWEEN GOVERNMENT AND MARKETS. Markets are inherently unstable, and government policy is stabilizing. 2. Markets are inherently stable, and government policy is destabilizing. A FUNDAMENTAL DIFFERENCE BETWEEN MICROECONOMICS AND MACROECONOMICS.

E N D

TWO VIEWS OF THE RELATIONSHIP BETWEEN GOVERNMENT AND MARKETS • Markets are inherently unstable, • and government policy is stabilizing. 2. Markets are inherently stable, and government policy is destabilizing.

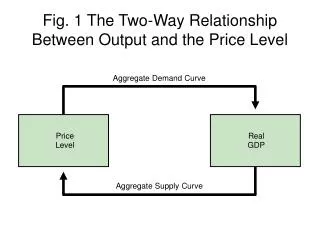

A FUNDAMENTAL DIFFERENCE BETWEEN MICROECONOMICS AND MACROECONOMICS Microeconomics focuses on a particular market (say, the market for oranges). It puts the rest of the economy “on hold” by invoking the ceteris paribus assumption. Showing how a particular market works is based on the assumption that all other markets are working fine. Macroeconomics focuses on large sectors of the economy (say, on input markets, such as the market for labor, or on output markets). It deals with the interaction among the different sectors and shows that, under certain assumptions, disturbances or malfunctions in one sector can infect all other sectors.

PART I: From Supply and Demand to Circular Flow

PART I From Supply and Demand to Circular Flow Supply and demand curves keep track of prices and quantities. Multiply the p times the q for output markets to get expenditures (e). Sum the expenditures in output markets to get total expenditures (E) Multiply the w times the n for input markets to get income (y). Sum the incomes in all input markets to get total income (Y) Macroeconomic equilibrium requires that Y = E.

“Market clearing” in the microeconomic sense is consistent with—and allows for—the natural rate of unemployment.

The equality here of Y and E does not deny the possibility of saving—which can get spent, too, by someone else.

E = Y = 3000 is just for illustration. For actual data, check the Federal Reserve Economic Data (FRED).

PART II: The Macroeconomics of Depression

PART II: The Macroeconomics of Depression Suppose the economy suffers a weakening of demand for output. Prices do not adjust--at least not immediately. Output adjusts, as do expenditures: PQ becomes PQ’ With E less than Y, excess inventories accumulate. The demand for labor (and other resources) falls. Wages do not adjust--at least not immediately. The level of employment adjusts: WN becomes WN’ Y is brought into line with E through adjustments in N.

MID-SHOW QUIZ: According to microeconomists, equilibrium (in the market for a particular good) is a balance between quantity supplied and quantity demanded and is achieved by the appropriate change in the good’s price.

MID-SHOW QUIZ: According to microeconomists, equilibrium (in the market for a particular good) is a balance between quantity supplied and quantity demanded and is achieved by the appropriate change in the good’s price.

MID-SHOW QUIZ: According to microeconomists, equilibrium (in the market for a particular good) is a balance between quantity supplied and quantity demanded and is achieved by the appropriate change in the good’s price.

MID-SHOW QUIZ: According to macroeconomists, equilibrium (for the economy as a whole) is a balance between income and expenditures and is achieved by a change in the level of employment.

MID-SHOW QUIZ: According to macroeconomists, equilibrium (for the economy as a whole) is a balance between income and expenditures and is achieved by a change in the level of employment.

MID-SHOW QUIZ: According to macroeconomists, equilibrium (for the economy as a whole) is a balance between income and expenditures and is achieved by a change in the level of employment.

PART III: The Macroeconomics of Inflation

PART III The Macroeconomics of Inflation Suppose the economy experiences a strengthening of demand for output. Output cannot rise (except temporarily) above the full-employment level. Prices begin to rise The demand for labor increases Wages begin to rise. The supply of labor shifts as workers demand cost of living adjustments. The supply of output shifts to reflect the increased labor costs. Y and E are finally brought into balance through adjustments in P and W.