Download

1 / 14

140 likes | 260 Views

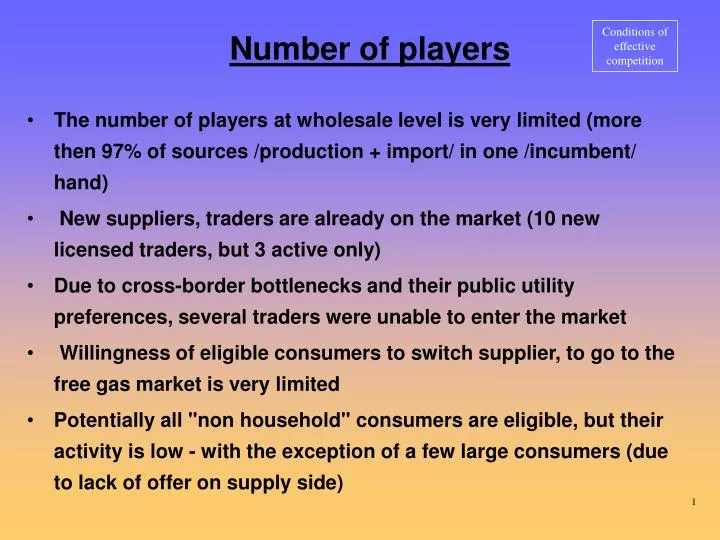

Conditions of effective competition. Number of players. The number of players at wholesale level is very limited (more then 9 7 % of sources /production + import/ in one /incumbent/ hand) New suppliers, traders are already on the market (10 new licensed traders, but 3 active only)

E N D

Conditions of effective competition Number of players • The number of playersat wholesale level is very limited (more then 97% of sources /production + import/ in one /incumbent/ hand) • New suppliers, traders are already on the market (10 new licensed traders, but 3 active only) • Due to cross-border bottlenecks and their public utility preferences, several traders were unable to enter the market • Willingness of eligible consumers to switch supplier, to go to the free gas market is very limited • Potentially all "non household" consumers are eligible, but their activity is low - with the exception of a few large consumers (due to lack of offer on supply side) 1

Eligible customers with willingness to switchsupplier • 6% of gas consumption traded on the free market (through bilateral contracts) in the first year • 23 eligible customers changed supplier through 3 active traders • 1 eligible customer (only) changed supplier without trader • Limited available cross border capacity for the free market segment at the eastern border • The local production is mostly at the incumbent wholesaler • Weak financial incentive of the eligible consumers: • Regulated end-user prices in public segment (compared to market price) • Relative higher risk on the free market (non-stable /continuously developing/ market rules; non-liquid national market; at congestion priority of regulated segment) 4

Conditions of effective competition Market structure, which notfacilitates efficient competition • Some specialties of the Hungarian market structure; • Hybrid Model where the Public Service Supply Segment (with regulated wholesale andend-user prices) and the Free Market Segment operate parallel • Public Service Wholesaleras dominant player on the free market as well (eligible customers could „come back” to the regulated market) • No power exchange • No indicative market prices • Administered balancing market pricing (no liquid market) 5

Conditions of effective competition Market size, possibility of regional markets • Small national market (14 - 15 billion m3/year, ~100 m m3/day peak demand) • The current size of competitive market (~6%) is even smaller! • Common EU energy market as real (medium/long term) possibility • Regional markets - borders of the regions? (similar to electricity Mini Fora?, SEEEM ?, harmonized rules in the region: strict or loose? ) 6

Conditions of effective competition Supply market - reserves, import • Limited and decreasing local production • Limited cross border capacityat eastern border • The regulated Public Service Supply Market (Wholesaler) „owns”95% of capacities • Limited and not flexible storage facilities (for seasonal • storage only) 7

Challenges (1) • What are consumers expecting of the competitive market? • more freedom of choice → this expectation is only realistic in case there are several players on the market and sufficient supply • better quality of service → generally a network issue, what is left at monopoly + better supplier/trader service (generally satisfied) • simple switch of supplier/trader, low barriers of entering the market → a market (and consumer) friendly regulatory environment is needed, as well as network and system operation activity well unbundled from commercial interests (we are before and during the formulation of requirements and implementation) • dropping prices and offers of a structure in line with consumption habits → this can only be expected in an efficient wholesale and retail competition 8

Challenges (2) • Create the right incentives; • for market players to utilise the existing cross border capacities and storage: • Entry – Exit capacity allocation and network charges; • transparent, non-discriminative congestion management rules • for investors to develop the infrastructure (new transmission network, gas storage) • increase supply quality, enhance continuity of supply „Gas release" program could help 9

Challenges (3) • Medium and long term Security of Supply (research on the necessary comfort of investors) • Regional market • Analysing, understanding and implementing some of the new elements of the EU Directives (PSO, universal services, regulatory functions, „real” management separation of activities): • PSO as it is in the Hybrid Model? Or new model without Wholesaler? Universal Service • More regulatory functions (forcing competition, dispute settlement, network and storage charges)? • HEO draft Guideline on Management Separation • Some amendment of the legal framework is necessary 10

Hungarian approach of regulatory process • Mixture of different basic regulatory approaches • Continental law - detailed legislation but on the other hand very detailed licenses issued by HEO • Lack of regulatory autonomy, freedom, set by law (no price setting) HEO cannot set rules • High informal regulatory power • Licenses without pricing rules • Resolutions of HEO (like licenses) could be challenged • Regulatory practices picked up from other countries with different regulatory approaches (public hearing, price cap, quaranteed service, customer satisfaction measurement, …) • Multi-purpose “regulator” for gas, electricity, district heating; one person 11

Implementing regulatory methods, • practice applied by other regulators • OFFER, OFGEM(British Know How Fund); • •• GUARANTEED SERVICES • •• MEASURE OF SERVICE LEVEL • •• ANALYSIS OF OUTAGES • CEC, CPUC(USAID); • •• MEASURE OF CUSTOMER SATISFACTION • •• DATA AND INFORMATION BASE, LAN • •• LICENSE CONDITIONS - COMPLIANCE MONITORING SYSTEM • VICTORIA /AUSTRALIA/; • •• BENCHMARKING PERFORMANCES OF LICENSEES • PUC OF MAIN (USAID); • •• STABILITY, CONTINUITY AND PREDICTABILITY IN DECISIONS • •• GUIDELINES • •• PUBLIC INVOLVEMENT IN DECISIONS • ELEMENTS OF ANALYSIS OF SECURITY OF SUPPLY • CNSE /SPAIN/ + ERSE /PORTUGAL/ (EU-Phare, bilateral cooperation); • •• CLEAR RESPONSIBILITIES ; REGIONAL MARKET, HARMONIZED RULES • POTENTIAL FUTURE OF PPA-SYSTEM • CEER ; excellent possibility for exchange of regulatory practices 12

New regulatory priorities(competition, new directives) • Interconnection capacity allocation (transparent rules) • Congestion management rules and practice • Network availability (outages) (supply quality) • New connection to the networks • Level of transparency • Level of competition (monitoring, forcing competition) • Separation of activities (unbundling) • Ex ante network charges (non-discrimination) • Network access conditions • Complaint settlement (dispute settlement)13 • Monitoring security of supply • Special consumer protection measures (vulnerable consumers) 13

THANK YOU FOR YOUR ATTENTION ! szorenyig@eh.gov.hu www.eh.gov.hu