Download

1 / 29

290 likes | 496 Views

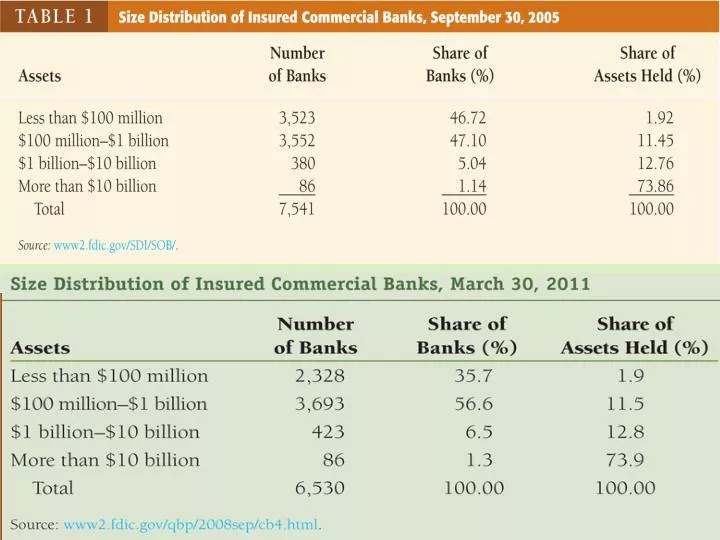

Size Distribution of Insured Commercial Banks, September 30, 2008 and update. 3,046 4,039 486 86 7,640. 39.9 52.9 6.1 1.1. 1.3 9.7 10.0 79.0. Bank Failures in the United States, 1934–2010. Source: www.fdic.gov/bank/historical/bank/index.html .

E N D

Size Distribution of Insured Commercial Banks, September 30, 2008 and update 3,046 4,039 486 86 7,640 39.9 52.9 6.1 1.1 1.3 9.7 10.0 79.0

Bank Failures in the United States, 1934–2010 Source: www.fdic.gov/bank/historical/bank/index.html.

Subsidiary of BofA Subsidiary of Toronto-Dominion

Ten Largest Foreign Banks, 2008 Ten Largest Foreign Banks, December 30, 2008

Decline of Traditional Banking • Decline in cost advantages in acquiring funds (liabilities) • Rising inflation rise in interest rates and disintermediation • Low-cost source of funds, checkable deposits, declined in importance • Decline in income advantages on uses of funds (assets) • Information technology less need for banks to finance short-term credit • and issue loans • IT lower transaction costs for other financial institutions • Bank Responses: • Riskier Lending … Commercial real estate, leveraged buyouts, takeovers • Off balance sheet activities

Bank Consolidation Interstate Banking and Branching Efficiency Act, 1994 • Skirting branch restrictions • ATMs, Bank Holding Cos. Geographic deregulation • Pre-Crisis Findings: • Net interest margin up • ROA, ROE up for big • banks • Intrastate deregulation • more positive for all but • big banks • Interstate deregulation • helps big banks most • Non-performing loans • down for biggest banks • but up for smaller banks • State of economy has • stronger impact on bank • performance than • branching deregulation • Skirting branch restrictions • ATMs, Bank Holding Cos. • Benefits of bank consolidation • Increased competition close inefficient banks • Efficiencies from economies of scale and scope • Lower chance of failure -- diversified portfolios • Costs • Fewer community banks less lending to small business • Banks in new areas increased risks/failures

December, 2008) 8% 6% 10% 37% 12% 16% 31% 10% 13% 31% 7% 3% 7% 9% http://www2.fdic.gov/sdi/main.asp

General Principles of Bank Management Liquidity Management Asset Management Liability Management Capital Adequacy Management Credit Risk Interest-rate Risk

Liquidity Management: Ample Excess Reserves Suppose required reserves are 10% of deposits Excess reserves are insurance against the costs associated with deposit outflows Cost incurred is the interest rate paid on the borrowed funds

Liquidity Management: Other Alternatives and Their Costs The cost of selling securities is the brokerage and other transaction costs and forgone interest Borrowing from the Fed also incurs interest payments based on the discount rate

Liquidity ManagementA Last Alternative: Reduce Loans Reduction of loans is the most costly way of acquiring reserves Calling in loans antagonizes customers Other banks may only agree to purchase loans at a substantial discount

Asset Management: Goals and Tools Goals 1. Seek the highest possible returns on loans and securities 2. Reduce risk 3. Have adequate liquidity Tools 1. Find borrowers who will pay high interest rates and have low possibility of defaulting 2. Purchase securities with high returns and low risk 3. Lower risk by diversifying 4. Balance need for liquidity against increased returns from less liquid assets

Liability Management Recent phenomenon due to innovation by money center banks Expansion of overnight loan markets and new financial instruments Negotiable CDs, Federal Funds Checkable deposits are now a less important source of funds Capital Adequacy Management Bank capital helps prevent bank failure The amount of capital affects return for the owners (equity holders) of the bank Low return on assets can be high return on equity Regulatory requirement Skin-in-the-game Benefits bank owners: a cushion that makes their investment safe Costly to owners: low debt:equity ratio low return on equity Choice depends on the state of the economy and levels of confidence

Application: How a Capital Crunch Caused a Credit Crunch During the Global Financial Crisis Huge losses on holdings of Mortgage Backed Securities Losses reduced bank capital Banks could not raise much capital in weak economy Tightened lending standards and reduced lending.

Managing Credit Risk: The Usual Suspects Screening Specialization in lending Monitoring and enforcement of restrictive covenants Long-term customer relationships Loan commitments Collateral and compensating balances Credit rationing deny loan counter adverse selection limit loan amount counter moral hazard

Managing Interest-Rate Risk If a bank has more rate-sensitive liabilities than assets, a rise in interest rates will reduce bank profits and a decline in interest rates will raise bank profits Basic gap analysis: (rate sensitive assets - rate sensitive liabilities) x interest rates = bank profit

Off Balance Sheet Assets/Activities Structured investment vehicles (SIVs) Loan sales (secondary loan participation) Fees for Foreign exchange trades for customers Servicing mortgage backed security Backup lines of credit/overdraft privileges Standby lines of credit guaranteeing securities/commercial paper Trading activities Principal-agent problem—trade against own client? Bond markets Foreign exchange markets Financial derivatives Internal controls: reduce principal-agent problem from trading Separation of trading activities and bookkeeping Limits on exposure Value-at-risk maximum daily loss with 1% chance Stress testing doomsday scenario impacts

Innovations: Response to Interest Rate Volatility • Adjustable-rate mortgages • Financial Derivatives Innovations: Response to Information Technology • Bank credit cards and debit cards • Electronic banking • ATM/Home banking/ABM/Virtual banking • Junk bonds • Commercial paper market … backed by banks • Securitization Innovations: Avoiding Regulation/Loophole Mining • Sweep accounts … reserve requirements • Money Market Mutual Funds … Regulation Q

Shadow Banking System • Financial intermediaries that conduct maturity, credit, and liquidity transformation without access to central bank liquidity or public sector credit guarantees. • Finance companies • Asset backed commercial paper (ABCP) conduits • Limited purpose finance companies • Structured investment vehicles (SIVs) • Credit hedge funds • Money market mutual funds (MMMFs) • Securities lenders • Government sponsored enterprises (GSEs) • Interconnections with each other and traditional banking system • ABCP • Asset backed securities • Collateralized debt obligations (CDOs) • Repurchase agreements • Liabilities of shadow banking system = $16 trillion vs. $13 trillion for banks. http://www.ny.frb.org/research/staff_reports/sr458.pdf

Possible Reforms • Increase/tighten capital requirements • Trade derivatives only on public exchanges transparency • “Mark – to – funding” accounting • Value assets relative to date their funding must be repaid • Rapid “resolution” of TBTF institutions • Make bankruptcy credible • Put creditors at risk eliminate moral hazard of TBTF

McFadden Act (1927) and Douglas Amendment (1956) limit interstate branching • Interstate Banking and Branching Efficiency Act (1994) deregulates branching • Gramm-Leach-Biley Financial Services Modernization Act (1999) repeals • Glass-Steagall

Regulating Finance: Regulation and Its Discontents • Lots of bases to cover Cover a base by regulation or by deregulation Unintended Consequences • Reactions to regulatory policies frustrate regulator intent Regulate bank balance sheets off-balance sheet activities Emplace a safety net bankers become skydivers • Regulation spreads to cover innovations complexity ineffectiveness Win by gaming the system

Asymmetric Information and Bank Regulation Government safety net • Deposit insurance and FDIC • Short circuits bank failures and contagion effect • Payoff method • Purchase and assumption method • Fed as lender of last resort: Too BIG to Fail • Financial consolidation Exacerbates Too Big to Fail • Safety net extended to non-bank financial institutions Safety Net Moral Hazard Problems • Depositors don’t impose discipline of marketplace • Banks have an incentive to take on greater risk Safety Net Adverse Selection Problems • Risk-lovers find banking attractive • Depositors have little reason to monitor bank

Attempted solutions: Constrain banks from taking too much risk • Promote diversification • Prohibit holdings of common stock • Set capital requirements … Capital as cushion • Minimum leverage ratio • Basel Accord: risk-based capital requirements … but there’s regulatory arbitrage Prompt corrective action: Close ‘em down when capital inadequate

http://www.fdic.gov/regulations/resources/directors_college/sfcb/capital.pdfhttp://www.fdic.gov/regulations/resources/directors_college/sfcb/capital.pdf

Attempted solutions: Constrain banks from taking too much risk • Promote diversification • Prohibit holdings of common stock • Set capital requirements … Capital as cushion • Minimum leverage ratio • Basel Accord: risk-based capital requirements … but there’s regulatory arbitrage Prompt corrective action: Close ‘em down when capital inadequate • Monitor … CAMELS • Capital adequacy • Asset quality • Management • Earnings • Liquidity • Sensitivity to market risk • Disclosure requirements … mark-to-market issue • Restrictions on competition … make banking boring

Primary Supervisory Responsibility of Bank Regulatory Agencies • Comptroller of the Currency—national banks chartered by Federal government since 1863 • Federal Reserve and state banking authorities—state banks that are members of the Federal Reserve System • Fed also regulates bank holding companies (BHCs) • JPM, BoA, Citi,… • FDIC—insured state banks that are not Fed members • State banking authorities—state banks without FDIC insurance

The U.S. regulatory regime: In need of reform? Sources: Financial Services Roundtable (2007), Milken Institute.