Download

1 / 19

190 likes | 298 Views

Foreclosure and Access to Mortgage Credit in Communities of Color. Cleveland State University June 15, 2012 | Cleveland, Ohio. Tom Feltner | Vice President Woodstock Institute | Chicago, Illinois P 312.3680310 x2028 | F 312.368.0316 tfeltner@woodstockinst.org. @ tfeltner @ woodstockinst.

E N D

Foreclosure and Access to Mortgage Credit in Communities of Color Cleveland State University June 15, 2012 | Cleveland, Ohio • Tom Feltner | Vice President • Woodstock Institute | Chicago, Illinois • P 312.3680310 x2028 | F 312.368.0316 • tfeltner@woodstockinst.org • @tfeltner • @woodstockinst WOODSTOCK INSTITUTE | June 2012

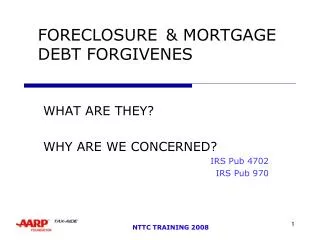

In Chicago region and across the country, foreclosure filings have stabilized at new, higher levels • .@tfeltner to @csuengage: with robosigning settlement in place, we should see increase in completed #foreclosure auctions in 2012 • New Foreclosure Filings • Completed Foreclosure Auctions WOODSTOCK INSTITUTE | MONTH YEAR

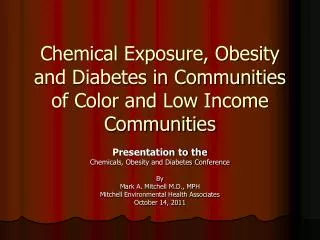

Local Impact of Foreclosure during the Economic Crisis is clear, communities of color disproportionately impacted • .@tfeltner to @csuengage: with robosigning settlement in place, we should see increase in completed #foreclosure auctions in 2012 2006 2007 2008 2009 Source: Woodstock analysis of data provided by Record Information Services WOODSTOCK INSTITUTE | June 2012

Local Impact of Foreclosure during the Economic Crisis is clear, communities of color disproportionately impacted • .@tfeltner to @csuengage: with robosigning settlement in place, we should see increase in completed #foreclosure auctions in 2012 2006 2007 2008 2009 Source: Woodstock analysis of data provided by Record Information Services WOODSTOCK INSTITUTE | June 2012

Local Impact of Foreclosure during the Economic Crisis is clear, communities of color disproportionately impacted • .@tfeltner to @csuengage: with robosigning settlement in place, we should see increase in completed #foreclosure auctions in 2012 2006 2007 2008 2009 Source: Woodstock analysis of data provided by Record Information Services WOODSTOCK INSTITUTE | June 2012

Local Impact of Foreclosure during the Economic Crisis is clear, communities of color disproportionately impacted • .@tfeltner to @csuengage: with robosigning settlement in place, we should see increase in completed #foreclosure auctions in 2012 2006 2007 2008 2009 WOODSTOCK INSTITUTE | June 2012

Single-family Mortgages Entering Foreclosure in the Six County Chicago Region, by Period of Origination, 2008-2011 @tfeltner to @csuengage: mortgages from the boom years of ‘05-07 continue to be overrepresented in new filings Source: Woodstock analysis of data provided by Record Information Services WOODSTOCK INSTITUTE | June 2012

Single Family Foreclosure in the Six County Chicago Region by Type of Mortgage, 2008-2011 • .@tfeltner to @csuengage: % of #foreclosure filings on conv and FHA mortgages increased from ‘08-11 Source: Woodstock analysis of data provided by Record Information Services WOODSTOCK INSTITUTE | June 2012

Accumulation of Foreclosure Activityin Communities of Color, 2006 to 2010 • .@tfeltner to @csuengage: foreclosure accumulation exceeds share of properties in communities of color Source: Woodstock analysis of data provided by Record Information Services WOODSTOCK INSTITUTE | June 2012

Change in Prime Home Purchase and Refinance Lending in Communities of Color, 2006 to 2008 • .@tfeltner to @csuengage: From ‘06-08, white communities saw a 43% decline in prime lending-communities of color saw a 69% decline Source: Home Mortgage Disclosure Act WOODSTOCK INSTITUTE | June 2012

Loan-to-value ratios of properties with mortgages in Chicago six county region, fourth quarter of 2011 • .@tfeltner to @csuengage: Chicago WOODSTOCK INSTITUTE | June 2012

Average home equity and outstanding mortgage debt per property in the Chicago six county region, fourth quarter 2011 • .@tfeltner to @csuengage: avg home equity in #chicago white communities is $108k, in African Am communities-just $7k #racialwealthgap Source: June 30, 2009 sample of national credit bureau data WOODSTOCK INSTITUTE | June 2012

Title • .@tfeltner to @csuengage: In #Chicago, 82% of mortgage lending in communities of color is FHA/VA, in #cleveland – 85% WOODSTOCK INSTITUTE | June 2012

Low Credit Scores Concentrated in Communities of Color • .@tfeltner of @woodstockinst at @csuengage: In Chicago, 54% of people in African Am communities have #creditscore < 620 #racialwealthgap Source: June 30, 2009 sample of national credit bureau data WOODSTOCK INSTITUTE | June 2012

There is Tremendous Polarization in Credit Score Distributions • .@tfeltner at @suffolk_U: In African Am communities just 18% have #creditscores > 740, in white communities 57% do #racialwealthgap WOODSTOCK INSTITUTE | June 2012

Examples of Credit Tightening • Increasing cutoffs for #creditscores impacts access to mortgage and small business credit in communities of color Federal Housing Administration (FHA) has implemented tighter credit score standards for FHA loans Under the proposed rules, borrowers with less than a 500 credit score would no longer qualify for an FHA loan Borrowers with credit scores between 500 and 579 would be required to make a minimum 10 percent down payment. This policy change would impact 43 percent of people in African American communities, 23 percent in Hispanic communities Borrowers with a credit score of 580 or better would be required to have only a 3.5 percent down payment. Conventional mortgage lending In September 2009, Fannie Mae announced it was increasing its minimum credit score requirement from 580 to 620. Eliminates conventional financing for 11 percent of African American communities and 8.5 percent of Hispanic communities. This was in conjunction with other credit tightening changes designed to reduce the risk in Fannie Mae’s lending portfolio going forward. WOODSTOCK INSTITUTE | June 2012

Credit scores take years to recover after foreclosure • .@tfeltner to @csuengage: subprime borrowers #creditscore recovers in ~5 years after #foreclosure-prime borrowers take up to 10 Source: Kenneth Brevoort, and Cheryl Cooper. Foreclosure’s Wake: The Credit Experiences of Individuals Following Foreclosure. Federal Reserve Board and the Urban Institute, 2012. Web. 13 June 2012. WOODSTOCK INSTITUTE | June 2012

Reducing the Impact of Low Credit Scores on Communities of Color • .@tfeltner to @csuengage: accumulated #foreclosures, limited credit options, low #creditscores contribute to financial distress Support efforts to build credit for credit-underserved populations. Resources and standard curriculum should be made available to credit counselors to help them reach individuals with low credit scores and help them build their credit. Use additional data to build credit. Alternative data on repayment patterns can be utilized to capture the true default risk for individuals who have limited histories with traditional credit. Such variables might include on-time payments for utilities, cell phone bills, insurance premiums, rent, consumer loans, or health care. Utilize manual, relationship-based underwriting. Some borrowers with low credit scores could benefit from manual underwriting in certain mortgage and small business lending transactions. Many community banks, credit unions, and community development financial institutions have, for years, worked closely with customers to make sure that borrowers who are good credit risks can still obtain responsible loans. WOODSTOCK INSTITUTE | June 2012

Foreclosure and Access to Mortgage Credit in Communities of Color Cleveland State University June 15, 2012 | Cleveland, Ohio • Tom Feltner | Vice President • Woodstock Institute | Chicago, Illinois • P 312.3680310 x2028 | F 312.368.0316 • tfeltner@woodstockinst.org • @tfeltner • @woodstockinst WOODSTOCK INSTITUTE | June 2012