Download

1 / 33

330 likes | 341 Views

Diocese of Johannesburg Parish Council Workshop May 2015. AGENDA Introduction and Welcome Vision Management vs Leadership Leadership in a Christian Environment Principles of Good Governance 8 Characteristics as defined by the United Nations

E N D

Diocese of Johannesburg Parish Council Workshop May 2015

AGENDA • Introduction and Welcome • Vision • Management vs Leadership • Leadership in a Christian Environment • Principles of Good Governance • 8 Characteristics as defined by the United Nations • Application of above characteristics to Church Councils and Parishes • Tea • Church Wardens – Functions • Parish Council – Functions • Checklist for Wardens and Parish Council • Property • Acquisition, Alterations and Disposal • Maintenance • Insurance • Close

Biblical Quotes on Vision • Where there is no vision the people perish - Proverbs 29 v18 • If the blind lead the blind, both shall fall into the ditch - Matthew 15 v14

Servant Leadership defined • Is servant, rather than leader first • Servant leadership has vision • Has trustees to maintain vision and to ensure accountability

Characteristics of Servant Leadership • Listening • Accepting and empathising • Tolerance of weakness and imperfection • Foresight, anticipation and intuition • Awareness and perception • Persuasion and example • Persistence and determination • Courage to venture and risk • Creates autonomy through opportunity

The institution as servant • Most caring is mediated through institutions today – hospitals, churches, NGOs • Institutions can be impersonal and self-serving • Energy must be directed to be effective • Leaders must care for institution and all the people it touches • Trustees are symbol of institutional quality

Good Governance – what is it? • Leadership and management of an institution, including a parish • Applies to business and government • King Commission Report gives guidance • Requires commitment to the spirit and not the letter of the guidelines

Key steps for any institution Values, vision, goals and strategy Proactive organisation and planning Day-to-day oversight Coherent leadership - empowering

Planning and Budgeting Organising and Staffing Controlling and Problem Solving Predictability and Order Establishing Direction Aligning People Motivating, Inspiring Produces Change Management vs Leadership LEADERSHIP MANAGEMENT • Creating an Agenda • Developing a human network for achieving agendas • Execution • Outcome John P Kotter

General Principles of Leadership Five general principles can be deduced from the New Testament teaching as a whole: All authority is derived from Christ and exercised in His name and Spirit Christ’s humility provides the pattern for Christian service (Mat Ch 20 v 26 – 28) Government is collegiate rather than hierarchical (Mat Ch 18 v 19 & Ch 23 v8; Acts Ch 15 v 28) Teaching and managing are closely associated functions (1 Thes Ch 5 v 12) Administrative assistants are required to help the Teachers of the word (Acts C6 v 2 -3)

Source: United Nations paper, What is Good Governance?, www.unescap.org/huset/gg/governance.htm (24 December 2006). CHARACTERISTIC DEFINITION Accountability Consensus-oriented Accountability is a key requirement of good governance. Good governance requires mediation of the different interests in society to reach a broad consensus on what is in the best interest of the whole community and how this can be achieved.

CHARACTERISTIC DEFINITION Effectiveness and efficiency Equity and inclusiveness Good governance means that processes and institutions produce results that meet the needs of society while making the best use of the resources at their disposal. A society’s well being depends on ensuring that all its members feel that they have a stake in it and do not feel excluded from the mainstream of society

CHARACTERISTIC DEFINITION Participation Responsiveness Rule of law Participation by all is a cornerstone of good governance. Good governance requires that institutions and processes try to serve all stakeholders within a reasonable timeframe. Good governance requires fair legal frameworks that are enforced impartially.

CHARACTERISTIC DEFINITION Transparency Transparency means that decisions made and their enforcement are achieved in a manner that follows rules and regulations.

King III and Church • King III has broadened the scope of corporate governance in South Africa with its core philosophy revolving around leadership, sustainability and corporate citizenship.These key principles are given prominence: • Good governance is essentially about effective leadership. Leaders need to define strategy, provide direction and establish the ethics and values that will influence and guide practices and behaviour with regard to sustainability performance. • Sustainability is now the primary moral and economic imperative and it is one of the most important sources of both opportunities and risks for institutions. Nature, society, and institutions are interconnected in complex ways that need to be understood by decision makers. Incremental changes towards sustainability are not sufficient – we need a fundamental shift in the way institutions act and organise themselves. • Innovation, fairness, and collaboration are key aspects of any transition to sustainability – innovation provides new ways of doing things, including meaningful responses to sustainability. Fairness is vital because social injustice is unsustainable and collaboration is often a prerequisite for change.

King III and Church • Social transformation and redress is important and needs to be integrated within the broader transition to sustainability. Integrating sustainability and social transformation in a strategic and coherent manner will give rise to greater opportunities, efficiencies, and benefits, for both the institution and society. • King II required companies to implement sustainability reporting as a core aspect of corporate governance. Since 2002, sustainability reporting has become a widely accepted practice and South Africa is an emerging market leader in the field. • However, sustainability reporting has not been embraced by non-commercial institutions, and this is to be encouraged..

TEA 15 Minutes

Parish Council (Canon 28) The functions of the Council shall be: to consider matters affecting worship, stewardship, evangelism, education, social responsibility and pastoral care, to examine the needs of the community , and to initiate such action as shall be determined in any of these concerns to consider the general welfare and accommodation of all licensed clergy and, where applicable, their families and dependents, and to take such action as they deem necessary to seek at all levels such contact with other Christians as shall strengthen Christian witness and promote Christian unity to have direction and control of the properties and revenue and expenditure of the Parish, subject to Articles XVIII and XIX of the Constitution, the Canons of the Province, and the Rules of the Diocese in which the parish is situate to receive, consider and approve the estimates in respect of each financial year to receive and act upon all matters referred to it by the Bishop, the Diocesan Synod and other competent bodies

Church Wardens (Canon 29) • Churchwardens are the officers of the Bishop and the principal representatives of the congregation • Together with the Incumbent they constitute the executive of the Parish Council and have special responsibility in the following matters: • To ensure that a register is kept of all parishioners • To keep an inventory of all goods, ornaments and furniture belonging to the church and to deliver the same to their successors on ceasing to hold office • To provide for the safety and preservation of registers • To execute the policy of the Parish Council relating to property and parochial finance and to be responsible for the preparation of annual estimates of revenue and expenditure and the presentation of accounts to the Vestry • To see to the seating of the congregation, without respect of persons • To aid the Incumbent with information and counsel in all matters relating to the Parish, and particularly in cases contemplated in the rubrics before the service of Holy Communion. • It is their duty to complain (in writing) to the Bishop or Archdeacon if there should be anything plainly amiss or reprehensible in the life or doctrine of the Incumbent and also if there be anything contrary to order or decorum in the administration of Divine Service

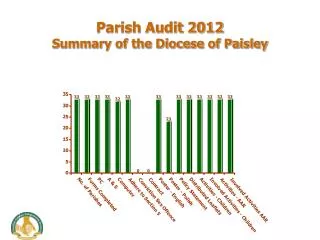

G6: CHECKLIST FOR CHURCHWARDENS AND COUNCIL • This checklist is intended as a guide to good governance and stewardship over the assets and activities of the Parish. It provides for appropriate accountability and transparency both to Parishioners and the Diocese and should form the basis of the first meeting of a Parish Council after election by Vestry. • 1. Organisation • Have responsibilities for the various activities of the Parish been allocated to portfolios of Council and committed to in writing so that the scope of responsibility and authority is clear? • No separate Bank accounts may be opened for subsections but all finances must be accounted for on one General ledger. • Where necessary are there policies and/or procedures in place to guide the actions of the portfolios? • Are those portfolios required to report regularly to Council on progress, including performance against their budget?

Does Council meet monthly and conduct business in accordance with a carefully prepared agenda? • Are minutes kept of all Council and Executive meetings which record all decisions taken? • Does Council receive copies of all Executive committee minutes? • 2 Budgetary control • Has an annual budget been prepared and approved by Council and Vestry? • Are monthly accounts prepared which measure performance against budget? • Are variances from budget explained to Council and approved by it?

Controls over income • Are there clear procedures in place to record all income, particularly Sunday collections, as soon as possible after receipt and for regular banking? • Is any expenditure made from cash income before banking properly recorded and approved? • Are these procedures working effectively?

Controls over expenditure • Are there clear procedures for requesting expenditure eg a requisition form which must be supported by vouchers and approved by the responsible portfolio? • Are cheques signed by two signatories only after the approved vouchers have been presented? Electronic payments released by two authorized persons. • Is a list of cheque and cash payments made, and to be made, presented to Council for approval at each meeting? • Only abnormal payments should be explained at council meetings all others must be in terms of the approved budget. • Are all vouchers properly filed by month for easy reference and safe-keeping? • Where electronic banking is done, both releasers should sign the audit trail provided by the bank which should be attached to the accounts or invoices.

5 Accounting records • Are suitable books or other forms of accounting record kept which enable monthly accounts to be prepared and will meet the needs of the auditors or Independent Verifier? • Do you have an auditor or Independent Verifier? • If not, have you discussed the matter with the Diocesan Office? • 6. Human resource matters • Do you maintain a file for each clergy person, lay staff member and volunteer which contains all the information required by law, including a contract of service or employment letter? • You must use the services of the Diocesan office for all your staff’s monthly payroll process. • Are you satisfied that no emoluments (Stipends or allowances) of any kind have been paid to clergy, lay staff or volunteers without the deduction of taxes in accordance with our tax laws? This includes Easter Offering and gifts etc. • Is there an employment contract for each staff member.

7 Controls over assets, registers and record • Is a proper record of all Parish moveable assets maintained and kept on the Parish premises? • Do all these assets exist, are they maintained in good order and are they adequately insured? • Are Parish buildings being properly maintained? • Are the parish buildings and contents adequately covered by insurance, bearing in mind the replacement costs of these assets. (Advice may be sought from the Independent Verifier or from a local builder or estate agent.) • Are proper registers of all Parishioners, Services, Baptisms, Funerals and Marriages being maintained? • Are back-up copies of computer files made regularly and kept off the premises? • Are the parish registers kept in fire-proof Safe.

8 Reporting to the Parish • Is there regular reporting to the Parishioners on the financial and other performance of the Parish? • Are the Financial Statements displayed monthly on the Notice board? • Are the DG lists displayed on Notice board every six months without names to confirm accuracy and awareness? • Is this guided by the Parish Vision and related strategies? • How frequently does it happen? • Are both oral and written reports provided? • Are written reports sent to all Parishioners or are they only seen by those attending services? • Are there suitable forums for Parishioners to discuss progress with members of Council?

IMMOVABLE PROPERTY MATTERS A: CANONS AND RULES Canon 31 Rules: Schedule I and Schedule M B: INTRODUCTION Ownership of all immovable property is vested in the Diocesan Trustees on behalf of a parish. No property may be purchased or altered without first obtaining their permission. Details of the procedure to be followed are outlined below. No consecrated ground or building shall be sold without authorisation from Synod. The Revocation of Consecration may only be given by the Bishop of the Diocese. It is essential to ensure that all buildings are insured at replacement cost. When any alterations or additions are complete it is the duty of the parish to inform the Diocesan Office so that insurance can be arranged.

C:PROCEDURE • There has to be a Special Vestry meeting called with the only item on the agenda being the proposed building (New; Alterations; Sale) • The following has to be presented to Vestry: • Reason why the parish council believe that the (new / alterations / sale) building is necessary • Plans drawn by a professional architect (Where applicable) • The architect should also prepare all other documentation that might be necessary in terms of municipal bylaws. • Three quotations for the cost of construction of the building • The quotations must, where possible, be from reputable building concerns • if the cost is estimated to exceed R250,000 then there must a report from a certified Quantity Surveyor • Where necessary funding will be obtained • Funding can only be from existing parish savings or from borrowings from the Diocesan Trustees. • No funding outside of the Diocese is permitted unless specific permission is obtained from the Diocesan Trustees. • In some instances a Bishop’s Faculty (permission) is required. (Canon 31.2) • Once Vestry has approved the proposed building the above documents have to be submitted to the Diocesan Trustees for approval. • Only once the building has been approved by the Diocesan Trustees can • building operations begin.

E: INSURANCE: It is essential to ensure that all buildings are insured at replacement cost. When any alterations or additions are complete it is the duty of the parish to inform the Diocesan Office so that insurance can be arranged.

Who to Contact in the Diocesan Office • Finance • Terry Chamberlain terry.chamberlain@anglicanjoburg.org.za • George Boyce george.boyce@anglicanjoburg.org.za • Property • Diana Modumo diana.modumo@anglicanjoburg.org.za • Insurance • Diana Modumo • Banking • Ivy Matthews ivy.matthews@anglicanjoburg.org.za • Medical Aid / Pension • Ivy Matthews • St Joseph’s • Nico Palmer nico.palmer@anglicanjoburg.org.za • 011 375 2700 • www.anglicanjoburg.org.za