Download

1 / 20

210 likes | 394 Views

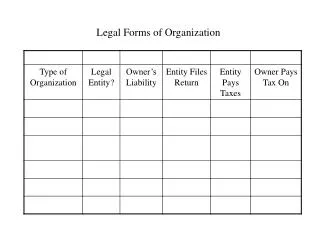

The legal forms of organisation. Chapter 12. © Luby & O’Donoghue (2005). Legal form affects a business. Taxation requirements Legal requirements Audit and financial requirements Sources of finance available. Legal forms. Sole proprietorships (trader) Partnerships

E N D

The legal forms of organisation Chapter 12 © Luby & O’Donoghue (2005)

Legal form affects a business • Taxation requirements • Legal requirements • Audit and financial requirements • Sources of finance available

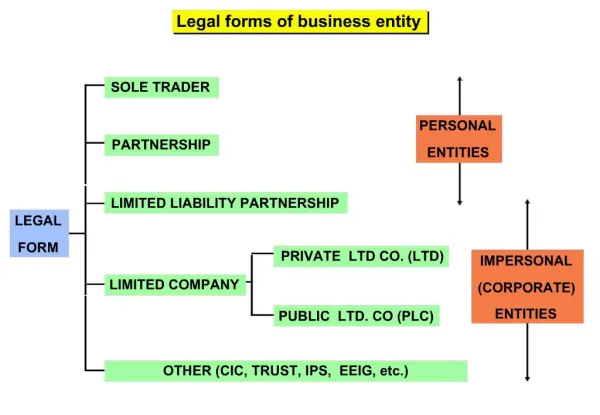

Legal forms • Sole proprietorships (trader) • Partnerships • Limited liability companies • Not for profit organisations

Sole-traders • The sole trader legal form of organisation comes into being when an individual sets up in business and starts to trade in his or her own name. • The individual is the sole owner of the business. • A sole trader can also register a business name such as John Ryan trading as "Ryan & Sons".

Sole-traders • Advantages • The simplicity and ease in setting up in business. • The lack of legal controls and constraints (need records for Revenue Commissioners). • Privacy as the accounts of sole proprietorships are not required to be published unlike the accounts of companies. Disadvantages • Not protected by limited liability. • Sourcing finance can be difficult. • The rates of tax on profits for sole traders for are higher than for companies.

Partnerships • A partnership can be described as an association of persons carrying on business in common with a view to making a profit. The agreement between the persons can be in a verbal or written format. • Advantages • Simplicity and ease in setting up business. • The general lack of legal controls and restrictions compared to limited liability companies. • Partners often have a blend of skills and experience, which help to create a more effective organisation. • Partnerships have greater access to capital due to the fact that there is a greater pooling of capital and borrowing capacity. • Privacy as the accounts of partnerships are not required to be published to the general public but are required for tax purposes.

Partnerships • Disadvantages • Not protected by limited liability. • Sourcing finance can be difficult. • The rates of tax on profits are higher than for companies. • Partnerships can be quite unstable and break-up over relatively minor issues. • The life of the partnership can be limited by agreement or by the life of the partners.

Companies • A company is a corporate body, which has a legal existence quite apart from the owners (shareholders). Limited liability companies can have a perpetual life since ownership is represented by shares that are transferable. This ensures that companies can exist beyond the lives of their original owners. This is unlike sole traders or partnerships where the business ceases to exist on the death of the owners or partners.

Formation of a limited company • The formation of a limited company is handled by solicitors who draft the necessary legal documents that form its make-up. These documents are then registered with the company’s registrar where upon a certificate of incorporation is issued to the company. The company is now registered and can commence trading. • The main legal documents required are: • memorandum of association. • Articles of association. • Statement of nominal share capital. • Statutory declaration of compliance with all the requirements of the relevant companies acts. • List of persons who have consented to be directors. • Form of consent to act as directors from those who have agreed to be directors.

A private limited company is a company that has between two and fifty shareholders that have restrictions on the transfer of shares but are protected by limited liability. Key characteristics: Between 2 and 50 shareholders (min of 2 ). Business can commence immediately on incorporation. The right of transfer of shares is restricted as there is no market to actively trade in the shares. The company is prohibited from inviting the public to subscribe for its shares or debentures. Accounts must be audited each year. All companies must file their annual accounts whether audited or not with the companies registrar. Generally private companies are formed to ensure their owners benefit from limited liability. A private limited company

A public limited company • A public limited company is a company that has a minimum of seven shareholders that are protected by limited liability. Shares are freely transferable as they can be traded publicly and are quoted on a stock exchange. • Key characteristics • A min of 7 shareholders and no maximum limit. • Shares are freely transferable, a market exists to buy and sell the shares. • Shares of Plc’s may be quoted on the stock exchange (subject to permission by the stock exchange authorities). • Though incorporated a Plc cannot commence business until the registrar of company’s issues a Trading Certificate to commence business. This cannot happen until €38,092 of share capital has been subscribed. • Accounts must be audited each year and a copy filed with the companies registration office. • Generally public companies are significantly larger than private (although this is not always the case) and they tend to have more of an international dimension. • Generally public companies are formed to raise capital from the public.

Companies limited by guarantee • This is a company where the members usually do not provide money/capital on its formation but guarantee to pay its debts up to a certain limit in the event that the company goes into liquidation. Usually the sum is a nominal amount. This method of incorporation is used by non-profit making organisations such as clubs, charities and societies.

Unlimited companies • An unlimited company is one which ensures its member can be personally liable for the debts and liabilities of the business. This liability can be totally unlimited or limited to a certain figure. This is a big disadvantage, unlimited companies have the following advantages. • The right to reduce issued capital without court permission. • Exemption from filing accounts (privacy advantage).

Limited liability status • Advantages of Limited liability company status • Investor’s liability is limited. • Companies tend to have greater access to capital. • The business continues despite the death or incapacity of the investors. • Profits are taxed at the corporation tax rate of 12.5% (2004). • Disadvantages of Limited liability company status • Limited companies are more regulated than either partnerships or sole traders. • It is more difficult to withdraw money from a company than it is for a sole trader or partnership. • Once incorporated, companies must file their accounts with the companies registrar and hence there is a lack of privacy compared to sole proprietorship and partnership legal forms of organisation.

Legal requirements for limited companies • The Companies Acts 1963 • The Companies (Amendment) Act 1983 • The Companies (Amendment) Act 1986 • The Companies Act 1990 • Company Law Enforcement Act 2001 • Companies (Auditing and Accounting) Act 2003

Companies are legally required to • Keep proper books of accounts. • Accounts must be audited by an independent auditor. • All limited companies must register with the company’s registrar in Dublin Castle. • The company’s registration office keeps a file on each company which includes its annual accounts, names of directors, location of business, business name etc. Anyone can issue a search to get details of all companies both public and private. • Must hold an AGM once in every calendar year.

Administration of limited liability companies • An annual general (AGM) meeting should be held. • At the AGM shareholders can vote and appoint directors to run the company on their behalf. • An annual report should be provided. • An audit is a legal requirement under the Companies Act 1963 • The company must legally keep what are called statutory books which include the following • Register of shareholders. • Register of debenture holders. • Register of assets given as security. • Register of directors and secretaries. • Register of director’s interests in ordinary shares and debentures. • Minute books of directors’ meetings and general meetings. • Record of declarations by directors of interests in company contracts.

Not for profit organisations • A ‘not for profit’ organisation is established to achieve goals other than making a profit. • Making a profit is not their primary goal. • Examples would include the following: • Co-operatives • State sponsored enterprises • Charities