Download

1 / 13

130 likes | 270 Views

CCMI/057 Competitiveness of the Metals Industries Shipbuilding Industry Brussels, 30 Sept. 2008. New orders, completions and orderbook. New orders, completions and orderbook. Turnover of main shipbuilding areas. Steel Price Evolution. European Index. World Index. Asian Index.

E N D

CCMI/057 Competitiveness of the Metals Industries Shipbuilding Industry Brussels, 30 Sept. 2008

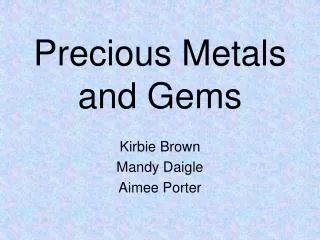

Steel Price Evolution European Index World Index Asian Index

European Market Share by Ship Types Less steel-intensive Ships Steel-intensive Ships

Conclusions • Shipbuilding sees a clear impact of price differences in the steel market • Due to time-gap between contract signature and delivery, yards take the full inflation risk • Level playing field for raw material is essential for steel consumers acting in a global environment • Effective contribution of down-stream users to climate change jeopardised

Comments on the Draft Opinion • Importance of Sectoral action; iron&steel direct employment is 1/30 of the 23 million jobs mentioned • Climate change: additional costs for steel producers will harm also down-stream users and their ability to contribute to the climate change challenge • “Global agreements” must not move the costs to the down-stream markets (e.g. by trade restrictions) • R&D: effective research done in sub-segments

+++ Thank you for your attention +++more info athttp://www.cesa.eu

Shipbuilding Requirement vs. CapacitySource: SAJ, September 2006 Mill.CGT 50.0 Newbuilding Capacity Europe (6.9) Expected Completion 35.7 China (14.7) 29.5 CHINA 23.7 23.5 EUROPE Newbuilding Requirement Korea (15.8) KOREA Japan (10.0) JAPAN Source: SAJ

Shipbuilding Requirement vs. CapacitySource: SAJ, September 2008 Mill.CGT 70 CAPACITY 57 Estimated COMPLETION GAP SHIPBUILDING COMPLITION CHINA NEWBUILDING REQUIREMENT KOREA KOREA JAPAN JAPAN