Download

1 / 50

500 likes | 503 Views

Learn about Medicare Part D, the prescription drug program that provides coverage for prescription drugs. Discover the different options available for supplementing Medicare and how to choose the right coverage.

E N D

Medicare • For people 65+ and under 65 with a disability • 4 parts of Medicare • Part A: Hospital Insurance • Part B: Medical Insurance • Part C: Medicare Advantage Plans • Part D: Prescription Drug Coverage • Part A & B called Original Medicare • Automatic enrollment if getting SS benefits, must enroll if not • Premiums always for Part B, only for A if not enough credits • Not comprehensive coverage, has coverage gaps • Out-of-pocket costs for A & B change yearly- see chart

Medicare • Pays for reasonable and medically necessary services • There are coverage gaps in Medicare including: • Part A in-patient hospital deductible • Part A daily co-payment for in-patient hospital days 61-90 • Part A daily co-payment for in-patient hospital days 91-150 • Part A daily co-payment for SNF days 21-100 • Part B annual deductible • Part B co-insurance (usually 20%) • First three pints of blood • Coverage outside the United States

Medicare Advantage • Option for supplementing Original Medicare • Offered by a private company that contracts with Medicare to provide a beneficiary with their Part A & B benefits • One way for a beneficiary to get additional Medicare coverage to cover the gaps in Original Medicare • The plan must offer Part D drug coverage – members who want drug coverage may onlytake drug plan offered by the Medicare Advantage plan • If enroll in stand alone PDP, will be dis-enrolled from Part C and returned to Original Medicare • Different plan types available • HMO, HMO-POS, PPO, SNP, PFFS

Medigap • Option for supplementing Original Medicare • Offers coverage to fill gaps in Original Medicare • Offered by private insurance companies, not the federal government • Prescription coverage NOT included; if a beneficiary wants prescription drug coverage, they must join a Medicare Prescription Drug Plan • A Medigap policy is different from a MA plan; MA plans are ways to get Medicare benefits. A Medigap policy acts as a secondary policy to cover the costs of Original Medicare benefits

Two Options For Supplementing Medicare Step 1: Decide how you want to get your coverage ORIGINAL MEDICARE MEDICARE ADVANTAGE PLAN OR PART B Medical Insurance PART A Hospital Insurance PART C Combines Part A, Part B and usually Part D & Step 2: Decide if you need a Prescription Drug Plan PART D Stand Alone PDP PART D Included in Part C Step 3: Decide if you need to add supplemental medical coverage END If you join a Medicare Advantage Plan with drug coverage (MAPD), you cannot join another drug plan and you don’t need and cannot be sold a Medigap policy MEDIGAP Supplement Core or Supplement 1 plan

Part D Overview • Medicare offers prescription drug coverage to everyone with Medicare • Provides outpatient prescription drug coverage • Beneficiaries with Part A and/or Part B are eligible • 2 ways to get prescription coverage: 1.Medicare Prescription Drug Plans (PDPs); also known as stand alone plans 2. Medicare Advantage (Part C) Plans with drug coverage • Part D is voluntary, but eligible beneficiaries who do not enroll may be subject to a penalty

Part D Plans • May differ on many levels but must meet both pharmacy access and formulary standards set by CMS • PDPs and MA-PDs may vary based on: • Benefit Design • Monthly Premium • Co-payments • Formulary • Drug Prices • Pharmacy Network • All plans must offer the standard prescription drug benefit or its equivalent. The plans may choose to offer supplemental benefits for an extra premium

Formulary The prescription benefit includes a list of “covered drugs” and this list is called the “formulary” If the insurer is very selective about which drugs are to be covered, then it is sometimes referred to as a “closed formulary”. If the formulary is open to all drugs but places drugs into different cost sharing categories or “tiers”, it is referred to as an “open formulary” Each plan must meet formulary standards. The formulary must include and cover certain drugs or certain classes of drugs. Medicare has established a category of excluded drugs

Examples of Part D Excluded Drugs Drugs for anorexia, weight loss or weight gain Drugs for the symptomatic relief of cough and colds Prescription vitamins and mineral products, except prenatal vitamins and fluoride preparations Non-prescription drugs (over the counter) Drugs that could be covered under Medicare Part A and/or Medicare Part B

Appeals to Formulary • Beneficiaries can take the following steps when a drug they are taking is not covered under the formulary • Ask prescriber if she/he meets prior authorization or step therapy requirements or if there are generic, over-the-counter or less expensive brand name drugs • Request a coverage determination (including an “exception”) that the plan cover the drug • Try to find a SEP in order to switch Part D plans to one that has a formulary that covers all of the drugs

Prior Authorization Many insurers will provide access to a particular drug only after the physician requests approval explicitly for that drug for the patient One reason for requiring prior authorization is that it is a means to make sure the doctor has considered the use of less expensive alternatives before requesting the particular drug that requires prior approval This is a very popular cost management technique used with many drugs on many Medicare Part D plans

Generic Vs. Brand Name Drugs Massachusetts is a generic-mandated state in which all pharmacists have to dispense generic if available unless the physician indicates: no substitution Generic drugs contain the same active ingredients, have the same strength and dosage as the brand name drug and must meet the same government quality control standards

Four Enrollments Periods • Initial Enrollment Period (IEP) • Open Enrollment Period (OEP) • Special Enrollment Period (SEP) • Medicare Advantage Disenrollment Period (MADP)

Initial Enrollment Period 65+: Mimics that of Medicare Part B (7 month period) Under 65: Mimics that of Medicare Part B; beneficiaries who become eligible for Medicare due to a disability can join during period 3 months before through 3 months after 25th month of cash disability payments MassHealth members: When eligible for Medicare, primary prescription coverage under MassHealth ends. MassHealth notifies Medicare of member’s dual status and individual has 60 days to enroll in Part D plan or will be auto-enrolled in a plan chosen at random

Open Enrollment Period • October 15th- December 7th, coverage effective January 1st • During this period beneficiaries can: • Join a plan for the first time (If late enrollee, would be subject to late enrollment penalty) • Switch plans (including changing MA plans) • Drop a plan • To switch a plan: • Simply enroll in new plan. No need to cancel old Medicare drug plan as the coverage will end when the new drug plan begins

Special Enrollment Period • Certain conditions make beneficiaries eligible for a SEP during which they can enroll in a Part D plan outside of the initial enrollment period. They include: • Moving out of their plan’s service area • Loss of creditable coverage • Having dual eligible status (enrolled in MassHealth & Medicare or enrolled in a Medicare Savings program) • Being a member of Prescription Advantage (a State Prescription Assistance Program known as a SPAP) • Switching to a 5-star rated plan – beneficiary can make one switch at any time during the year to a 5-star rated plan

Medicare Advantage Disenrollment Period • January 1st – February 14th • During this period, beneficiary CAN: • Dis-enroll from a MA plan and return to original Medicare and enroll in a stand-alone Medicare Prescription Drug Plan (PDP) • Dis-enroll from a MA plan without drug coverage and enroll in a PDP. May be subject to a late enrollment penalty • During this period, beneficiary CANNOT: • Switch from Original Medicare to a MA plan • Switch from one MA plan to another • Switch from one Medicare Prescription Drug plan to another

Late Enrollment If a Medicare beneficiary does not join a Medicare Prescription Drug Plan when first eligible and didn’t have other creditable prescription drug coverage that met Medicare’s minimum standards, they could incur a late enrollment penalty All Medicare beneficiaries (including those who are still working) must have creditable coverage to avoid the late enrollment penalty

Creditable Coverage • Coverage that is at least as good as Medicare Part D • Protects a beneficiary from the Part D penalty • Employer or retiree coverage, union coverage, VA coverage: Need proof of coverage to avoid penalty • Beneficiaries still working: • Benefits administrator has information about whether the employer coverage is creditable • Beneficiaries should be encouraged to ask the benefits administrator about their creditable coverage status if they have not been notified

Late Enrollment Penalty • Penalty is 1% of the national base beneficiary premium for EACH MONTH the beneficiary: • Did not enroll in a Medicare PDP when they were first eligible AND: • Had no prescription drug coverage OR • Had coverage that was not considered “creditable” OR • Had a lapse in creditable coverage of 2 full months (63 days)

Late Enrollment Penalty • The penalty is added to the premium at the time of enrollment and is a lifetime penalty except for: • A beneficiary under age 65 who is enrolled in Part D and subject to a late enrollment penalty will have the penalty waived at age 65 • This waiver mirrors the “clean slate” provided to Medicare enrollees subject to a Part B penalty prior to turning age 65 • Beneficiaries enrolled in Extra Help will have the penalty paid for by Extra Help. If the beneficiary loses her/his Extra Help, she/he would need to pay the Part D penalty

Supplement 2 (aka Medex Gold) • Considered creditable coverage • No penalty if beneficiary eventually joins a Part D plan • Beneficiary can join during a Part D plan during the Open Enrollment Period or if they qualify for a Special Enrollment Period • Dis-enrolling from the plan is NOT in of itself a SEP

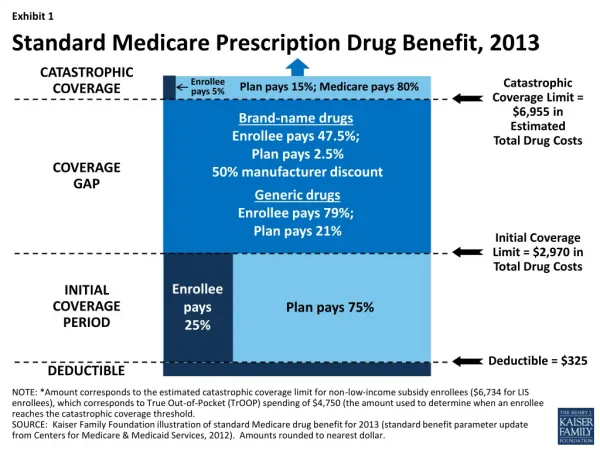

Part D Costs • Must pay monthly premium to the plan which includes an annual deductible that may change annually • Those with a Medicare Advantage Pan with drug coverage pay a monthly premium to the plan that includes the premium for their health care coverage and their Part D coverage • Premiums indexed according to income (same as Part B) • Premium can be deducted directly from Social Security check • Deductible amount changes yearly and varies from plan to plan

Co-payment VS. Co-insurance Co-payments: Set dollar amount that is paid at the pharmacy, e.g., $8 for a 30-day supply at a retail pharmacy. Usually, generic drugs have lower co-pays than brand drugs Co-insurance: Percentage of the retail cost, e.g., 25% for a 30-day supply. This is the amount the beneficiary would be required to pay

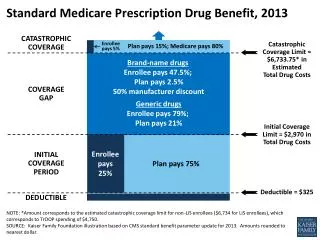

ACA Closing the Coverage Gap • The Affordable Care Act reduces the costs to beneficiaries who reach the coverage gap. Effective January 2011 beneficiaries receive discounts on both brand and generic drugs in the gap. These discounts will increase each year until the coverage gap is eliminated in 2020

Enrolling into Part D Review plan options Plan Finder Tool on www.medicare.gov Determine PDP plan vs. MA-PD plan Consider cost, coverage, quality, and convenience Try to avoid drug restrictions using: Step Therapy Prior Authorizations Quantity Limitations Contact plan directly or call 1-800-Medicare Enrollment can take place on the phone, online, or through a mailed in paper application

Extra Help/Low Income Subsidy (LIS) • Extra Help is a federal assistance program to help low-income and low-asset Medicare beneficiaries with costs related to Medicare Part D • Extra Help subsidizes: • Premiums • Deductibles • Copayments • Coverage Gap “Donut Hole” • Late Enrollment Penalty • Does NOT subsidize non-formulary or excluded medications • Apply through Social Security Administration

2 Levels of Extra Help • Full Extra Help • 135% of the Federal Poverty Level (FPL) and asset limits • Full premium assistance with no deductible • Low, capped co-payments. Could be $0 for some generics at any level • Partial Extra Help • 150% of the FPL and asset limits • Reduced premiums (sliding scale – between 25% -75% assistance dependent upon income) • Reduced deductible and 15% co-payments

Extra Help Eligibility • Resources counted: • Bank accounts (checking, savings, CDs) • Stock, bonds, savings bonds, mutual funds, IRAs • Real estate other than a primary home • Resources NOT counted: • Primary home, car • Property one needs for self-support, such as a rental property (rent payments are considered as income) • Burial spaces owned by a beneficiary • Personal belongings

Dual Eligibles Medicare beneficiaries who are also enrolled in Medicaid/MassHealth, Supplemental Security Income (SSI) or a Medicare Savings Program/MassHealth Buy-in) are known as dual eligibles These beneficiaries do not have to apply for Extra Help as they are “deemed eligible” and will be enrolled automatically

Extra Help Coverage Period • If an individual loses their Extra Help coverage due to no longer meeting the eligibility requirement, the end of the benefit coverage will depend upon when the individual loses their Extra Help coverage • If the Extra Help benefit is lost PRIOR to July: Coverage will end by December 31st of that SAME year • If the Extra Help benefit is lost AFTER July: Coverage will end by December 31st of the FOLLOWING year

Prescription Advantage Massachusetts’ State Pharmacy Assistance Program (SPAP) Provides secondary coverage for those with Medicare or other “creditable” drug coverage (i.e. retiree plan) Benefits are based on a sliding income scale only – no asset limit! Level of assistance provided is determined by gross income Different income limits for under 65 and 65 and over

Benefits for Individuals on Medicare or With Creditable Coverage • Helps pay for drugs in the gap (for most members) • May help pay all or part of the Medicare prescription drug plan's drug co-pays (All medications must be covered by primary plan) • Those in top income category (S5) must pay $200 annual fee for limited benefits • Members are provided a SEP (one extra time each year outside of open enrollment to enroll or switch plans) • Prescription Advantage does NOT pay the late enrollment penalty fee

Benefits for Individuals NOT on Medicare • Offers members who do not qualify for Medicare, primary prescription drug coverage • Coverage has no monthly premium • Depending on income, members will pay a co-pay for prescription drugs and will have an annual out-of-pocket spending limit and quarterly deductible. Once annual out-of-pocket limit is reached, Prescription Advantage will cover drug co-pays for the remainder of the plan year • Members are provided a SEP (one extra time each year outside of open enrollment to enroll or switch plans)

Part D Review • Review • What is Medicare Part D and how is it offered? • Who is eligible? • What is creditable coverage? • How is the late enrollment penalty calculated? • When is the Open Enrollment Period? • When does the coverage gap or “donut hole” begin? • What programs are available to reduce drug costs?

Part D Quiz 1. Late enrollees in Part D will face a penalty of: a) 10% per year c) 1% per month b) 5% per year d) l0% per month 2. To meet the out-of-pocket requirement for catastrophic coverage Part D enrollees can (select all that are correct): a) Pay for their drugs themselves c) Buy drugs from Canada b) Use Prescription Advantage d) Get family members to help 3. Define “creditable coverage” 4. Why is it important that a beneficiary know if she/he has creditable coverage?

Part D Quiz, cont. 5. What does the Low Income Subsidy (LIS) help pay for? 6. Who is eligible to receive LIS? 7. Who must apply and who is “deemed eligible”? 8. Minnie Sota meets with you at the SHINE office. She read about Part D and is not sure if she needs it. She will be retiring and will have a retiree plan from her employer with prescription coverage. How would you assist Minnie with her decision? 9. Pat E. Cake meets with you on November 20th. She says she belongs to a Medicare Advantage Plan. She tells you the prescription drug plan with her MA costs more than she wants to pay, so she has decided to take the Part D plan offered by the agent she met at CVS. How would you assist her?

Case Study 1:Ann Apolis • Ann is very distraught about the Medicare Part D program. She currently has Medicare A & B and a retiree Medicare supplement plan through her former employer. She is very happy with her retiree plan. It provides coverage for all the deductibles and copays under Medicare and also provides unlimited drug coverage with $5-$15 co-pays for a 90-day supply of her medications. Her monthly premium for the retiree plan is $145.00. Her friend told her that she should have joined the Medicare Part D program during the initial open enrollment. The friend also told her she will face a penalty if the retiree plan should stop providing coverage and she wants to join Part D in the future. • How would you help her?

Case Study 2:Mel O. Dee • Mel is assisting his mom who has finally decided to retire at age 72. His mom visited her local Social Security office and signed up for Medicare B. (She signed up for A when she turned 65.) He understands that she also needs to sign up for a Part D plan. His mom takes few meds and he thinks her drug costs are not more than a few hundred dollars/year. Mel heard that Part D plans are expensive and don’t cover many meds. He has no idea how to go about helping her to choose a plan or whether she really needs one. He is concerned about the costs for Part D along with any other insurance/ care costs since her only income will be SS of $15,000/year. She owns her own home and has about $15,000 in assets and a $10,000 life insurance policy. • How would you help him?

Case Study 3:Manny Phestacion • Manny meets with you at the SHINE office. He is 66 years old and still working full-time. Manny is covered by his group health plan. He enrolled in Medicare Part A when he turned 65. Manny understands that he does not need to enroll in Medicare Part B or a Medicare Prescription Drug Plan (Part D) until he stops working. He thinks he can enroll when he retires and will not have to pay a late penalty. • Is he correct?

Case Study 4:Jean E. Ology • Jean comes to see you at the SHINE office after previously reviewing her options with you over the phone. She is retiring in 2 months and wants to get your assurance that the options she chose will work. Jean takes 3 medications — two are generic and relatively inexpensive and one is an expensive brand. After hearing about the Part D program, she has decided to go with a Medicare Advantage (Medicare HMO) plan and join a Medicare Prescription Drug Plan (Part D) that provides coverage for generics during the gap (donut hole). • How would you help her?

Case Study 5:Bud Jet • Bud meets with you at the SHINE office. Bud just retired last month. He has Medicare A & B and a retiree Medicare supplement plan from his former employer. He received a notice from his former employer that his drug plan coverage is not as good as the Medicare Part D drug coverage. His understanding is that he can stay with his employer plan or join Medicare Part D. After comparing the cost of his retiree plan with the Medicare Part D plan, he decided to stay with his employer plan as it fully meets his prescription needs and is less expensive. • How would you help him?

Case Study 6: Phil S. Steen • Phil meets with you at the SHINE office. He tells you he has Blue Cross/Blue Shield Supplement 1. He is also a member of Prescription Advantage. He has a Part D plan which had been working fine. However, his doctor just gave him a new medication that he discovered is not on the formulary of his plan. It’s an expensive medication, and he can’t afford to continue filling it. • How would you help him?

Case Study 7:Will U. Help • Mr. Help will be eligible for Medicare in 2 months and has already visited his local SS office to sign up for Medicare. The woman he met with at SS told him about Medicare A and B and also told him he must sign up for a Medicare Prescription Drug plan. He explained to her that he is a veteran and gets his prescriptions through the VA. She said that didn’t matter. He still needs to sign up or face a penalty. He tells you his income is a Social Security check for $1100/month and a pension of $200/month. He thought Medicare A+B and the VA would be all that he would need. He is worried about the Part D penalty and wants to know if you can help him figure out what Part D plan to join. • How would you help Mr. Help?

Question for Medicare: • I will be turning 65 this November. I plan to continue working until age 67 and will be covered by my employer health insurance. I will enroll in Medicare A when I turn 65 but won’t pick up B & D until I retire. I know that I have 8 months from termination of coverage under my active employment to pick up Part B. Is this also true for D? I will not face a penalty for not joining Part D as long as I’m covered under my employer plan while still actively working. Is that correct?