Download

1 / 4

50 likes | 193 Views

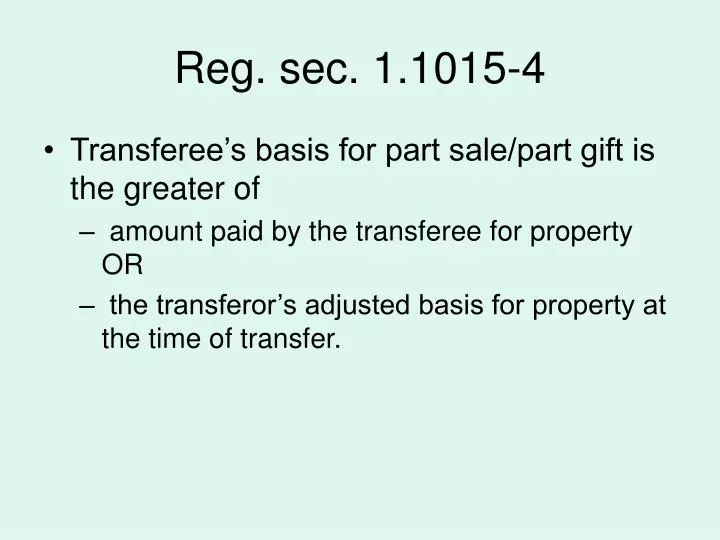

Reg. sec. 1.1015-4. Transferee’s basis for part sale/part gift is the greater of amount paid by the transferee for property OR the transferor’s adjusted basis for property at the time of transfer. Example 1 . Property with FMV of $50; G’s basis is $5 and G’s debt, which H will pay, is $1.

E N D

Reg. sec. 1.1015-4 • Transferee’s basis for part sale/part gift is the greater of • amount paid by the transferee for property OR • the transferor’s adjusted basis for property at the time of transfer.

Example 1 • Property with FMV of $50; G’s basis is $5 and G’s debt, which H will pay, is $1. • The rule tells us that H’s basis will be $5. Why? • H assumes debt and has $1 basis in “sale” portion; $1 of G’s basis allocated to sale portion. (Thus, G will have no gain on the sale portion.) • G has $4 of basis left; H takes her $4 basis for gift portion. • H has total basis of $5 ($1 plus $4), same as G’s, which is greater than amount paid.

Example 2 • Property with FMV of $50; G’s basis is $5; G’s debt, which H will pay, is $4. • The rule tell us H’s basis will be $5. Why? • H assumes debt and has $4 basis in “sale” portion; $4 of G’s basis allocated to sale portion. (Thus G will have no gain on the sale portion.) • G has $1 basis left; H takes her $1 basis for gift potion. • H has total basis of $5 ($4 plus $1), same as G’s basis, which is greater than what H paid.

Example 3 • Property with FMV of $50; G’s basis is $5; G’s debt, which H will pay, is $25. • The rule tells us that H’s basis will be $25. Why? • H assumes debt and has $25 basis in “sale” portion; all of G’s basis allocated to sale portion. (G will have $20 of gain on the sale portion.) • No basis left to be allocated to gift portion. • H has total basis of $25 ($25 plus $0), the amount he paid, which is greater than G’s basis.