Download

1 / 26

260 likes | 378 Views

DIAMOND JUBILEE CONFERENCE ON FEMA,WT &INTERNATIONAL TAXATION CASE STUDY ON IMPORTANT DECISIONS MR. T. P. OSTWAL. CONTENTS. Vodafone International holdings B V vs Union of India & Anr – Bombay HC (329 ITR 126) & SC Ruling

E N D

DIAMOND JUBILEE CONFERENCE ON FEMA,WT &INTERNATIONAL TAXATIONCASE STUDY ON IMPORTANT DECISIONS MR. T. P. OSTWAL T.P.Ostwal & Associates

CONTENTS • Vodafone International holdings B V vs Union of India • & Anr – Bombay HC (329 ITR 126) & SC Ruling • Sanofi – AAR Ruling AAR No. 846 & 847 • AT&T Birla Nuvo – Bombay HC Ruling 242 CTR 561 T.P.Ostwal & Associates

Vodafone International holdings B V vs.Union of India Bombay HC & SC Ruling T.P.Ostwal & Associates

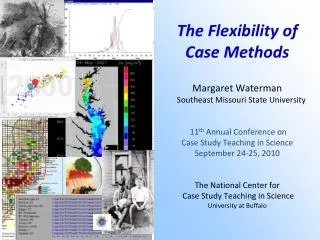

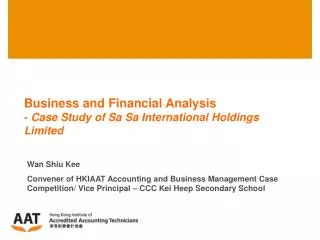

HTIL (Cayman Islands) HTI (BVI) Holdings Ltd CGP Vodafone NL 8 Entities Vodafone ruling (Bombay High Court) 329 ITR 126– facts of the case Shareholders Listed in Hong Kong Vodafone plc Sale Purchase Agreement UK British Virgin Islands Netherlands Transfer of CGP share to Vodafone NL Cayman Islands India VEL Mauritius IND SUBS T.P.Ostwal & Associates

Issues under consideration • Tax authorities jurisdiction to tax the transaction • Extra-territorial application of the withholding tax provisions (WHT) in an offshore transaction involving two non-residents (NRs) • High Court observations • Tax planning is legitimate unless arrangement is sham with objective of tax evasion • Controlling interest is not a separate asset – Shares represent interest of shareholder made up of bundle of rights • Situs of capital assets is the crucial jurisdictional condition to attract chargeability • Jurisdiction of a State to tax NRs based on existence of nexus – either based on presence or origin/source • Application on WHT provision not restricted to residents only – no limitation of extra territoriality; WHT obligation limited to the appropriate portion taxable in India • Comments on Bby HC decision on Birla AT&T AND TATA. • Also say about GVK Industries SC Decision. Vodafone ruling (Bombay High Court) T.P.Ostwal & Associates

Vodafone ruling (Bombay High Court) • High Court ruling • Acquisition of a panoply of entitlements including control premium, use and rights to Hutch brand, non-compete agreement, etc • Essence of the transaction was a change in the controlling interest • Parties were aware of the composite nature of transaction, not a transfer simpliciter of a single share in CGP • Rights and entitlements constitute in themselves capital assets • Apportionment of income to the extent taxable in India - Manner of apportionment to be determined by Tax Authority • Chargeability and enforceability are distinct legal conceptions - Mere difficulty in compliance or in enforcement is not a ground to avoid observance T.P.Ostwal & Associates

UPDATES • The tax department on March 23 sought to penalise Vodafone International, the holding company of Vodafone Essar, for its failure to present Cayman Island income tax returns and certain other documents. The I-T department had asked for these documents between January and October 2009. • In January 2009 the Supreme Court had rejected a writ petition by Vodafone challenging the original notice from the I-T department. The apex court referred the case back to the Bombay HC while asking the I-T department to decide if it had the jurisdiction to tax the transaction in which Hongkong-based Hutchison sold its Indian telecom unit to Vodafone in 2007. The Bombay HC started hearing the case from October 2009 and ruled against Vodafone in September last year. The company has appealed this decision in the Supreme Court. • The tax department already has a pending case against the Vodafone group seeking up to 11,000 crore. The Indian tax department contends that Vodafone should have withheld capital gains tax from Hutchison in 2007, when the UK-based telecom operator bought 67% voting rights in Vodafone Essar for $11 billion. Vodafone purchased the stake through Cayman Islands-based CPG, a unit of Hutchison Telecommunications International. T.P.Ostwal & Associates

Vodafone submitted a deposit of 2,500 crore and also provided a bank guarantee worth 8,500 crore with a state owned bank. Vodafone filed a petition to block the tax department’s latest penalty contending that “It is difficult to understand the rationale behind the tax authorities seeking to impose penalties on a matter which the tax authorities have themselves described as a ‘test case’.” • The Supreme Court on 15.4.2011 waived one per cent court fee on the Income Tax Department , on the Rs 2,500 crore deposited by the Vodafone International Holdings , after the government gave an undertaking that it would not make claim of “unjust enrichments”. • The apex court bench headed by Chief Justice SH Kapadia directed Vodafone to appear before the Income Tax department to explain its position on the department’s notice seeking imposition of penalty for its alleged failure to deduct tax at source on its stake purchase in Hutchison-Essar. “They (the I-T department) are asking you (Vodafone) to appear only. You go and appear and put your representation there. Let them pass the order,” the court said. • Meanwhile, the court also made it clear that if the IT Department passes any order for penalty, it would not be enforced till Supreme Court’s further order as the main matter of tax dispute is still pending in the apex court.“No steps would be taken to enforce a penalty if imposed on the petitioner,” the court said. T.P.Ostwal & Associates

SEQUENCE OF EVENTS • Feb 07 – Vodafone bids for acquiring the telecom business USD 11.08 billion based on an enterprise value of USD 18.8 billion • Feb 07 – Vodafone enters into an arrangement/agreements with Hutch relating to purchase of more than 50% controlling stake in VEL • May 07 – FIPB consents to the Vodafone- Hutch deal under FDI regulations subject to compliance with inter alia Indian tax laws • Effective holding by Vodafone NL of 52%; Indian partners agree to retain 15% shareholding with full control including voting and dividend rights, Vodafone NL has an entitlement to acquire this 15% indirect interest in VEL • May 07 – Agreement consummated and payment made post FIPB approval • Aug 07 – Show cause notice (SCN) to VEL seeking to treat it as “representative assessee” • Sep 07 – SCN also issued to Vodafone NL (buyer entity) for failure to withhold tax as an Assessee in Default (AID) • Sep 07 – VEL and Vodafone NL challenge the notice & file writ petitions before the Bombay HC • Dec 08 – Bombay HC dismisses writ petition by Vodafone NL; grants 8 weeks to enable appeal before Supreme Court (SC) • Jan 09 – Special leave petition filed by Vodafone NL before the SC also dismissed with a direction to Tax Authority • Jurisdiction issue to be examined as a preliminary issue and if this issue is decided against Vodafone NL, Vodafone NL can challenge it before the Bombay HC as a question of law T.P.Ostwal & Associates

SEQUENCE OF EVENTS • Oct 09 – Second SCN issued to Vodafone NL • May 2010 – Order passed by Tax Authority asserting jurisdiction to tax the transaction in the hands of Vodafone NL as an AID • Aug 2010 – Vodafone NL‟s and Tax Authority‟s arguments heard on the second writ petition filed by Vodafone NL before the Bombay HC, decision kept on hold • Sep 2010 – Bombay HC dismisses the second writ petition in a detailed order, Jurisdiction of Tax Authority to tax the transaction upheld • Oct 2010- Vodafone seeks cover from the Bombay High Court on after the income tax (I-T) department initiated action against the telecom operator, describing it as an ‘agent’ for tax collection on behalf of Hutchison. IT department raises demand of 11000 crore on Vodafone International Holdings BV. • Nov 2010 – The Supreme court asks Vodafone to deposit 2,500 crore in 3 weeks and furnish bank guarantee worth 8,500 crore in 8 weeks • Mar 2011 – IT department seeks to penalise Vodafone – penalty to tune of • April 2011 – SC waived 1% court fee on the IT Department, on the Rs 2,500 crore • No steps would be enforced by the IT dept for penalty till Supreme Court’s further order • August 2011 – SC starts the proceeding – Hearing begins , judges ponder over situs vs. control • Till date - Various issues discussed at length … judgement awaited… T.P.Ostwal & Associates

ADITYA BIRLA NUVO LTD BOMBAY HC RULING - 242 CTR 561 T.P.Ostwal & Associates

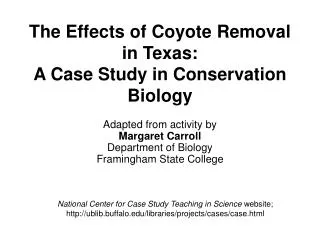

ADITYA BIRLA NUVO New Cingular Wireless Services Inc. (Earlier known as AT&T Inc)/ MMM Holdings LLC 4. Sale of shares of AT&T Mauritius on 28 Sep 2005 1. JV Agreement entered between AT&T US and AB Nuvo on 5 December, 1995. 2. Allotment of shares to AT&T Mauritius as a ‘permitted transferee’ as per the JVA (1996-2003). 100% AT &T Mauritius Ltd. (Mauritius) 4. Sale of ICL shares on 28 Sep 2005 Overseas 32.9% India Idea Cellular Ltd (Earlier known as Birla Communications/ Birla Tata AT&T Communications Ltd 33.7% 32.7% AB Nuvo Ltd Tata Industries Ltd 3. Shareholders Agreement between AT&T Inc, AB Nuvo and Tata Industries on 15 December 2000. T.P.Ostwal & Associates

Facts • JV Agreement entered into between AT&T US and Grasim Ind (now AB Nuvo) in December 1995 for carrying on telecom business. AT&T US & the Birla Group, as Founders to jointly own & operate the JV Co i.e. BCL (now ICL). AT&T US was under obligation to subscribe & pay for shares towards 49% stake in ICL. • Shares in ICL were to be held by Founders in their own name or through a "permitted transferee" (being a 100% subsidiary of the Founder) - AT&T Mauritius appointed as permitted transferee to be bound by the terms of JVA. • Tata Industries was added to the JV - new Shareholders Agreement entered into on 15 December 2000 . Under the Shareholders Agreement, AT&T Mauritius designated AT&T USA as its representative to exercise all rights and obligations attached to shares except the obligation to pay for the shares. • In October 2004, pursuant to takeover of AT&T US by Cingular Wireless group, it was renamed as New Cingular Wireless Services Inc ('NCWS'). • In September 2005, AT&T Mauritius sold 50% of its stake in ICL to AB Nuvo. NCWS also a party to the SPA . AB Nuvo deposited funds in bank account of AT&T Mauritius; on same day funds transferred to NCWS . NCWS & MMMH sold shares of AT&T Mauritius to Tata Industries T.P.Ostwal & Associates

Issues before the High Court • Who would be treated as the beneficial owner of shares of ICL i.e. NCWS or AT&T Mauritius? • Whether transaction for sale of shares by AT&T Mauritius to AB Nuvo would be liable to capital gains tax in India? • Whether AB Nuvo would be deemed to be the representative assessee of NCWS u/s 163 of the ITA. T.P.Ostwal & Associates

Applicant’s Contentions • The shares of ICL were acquired & sold by AT&T Mauritius and thus AT&T Mauritius was not liable to tax in respect of capital gains under India-Mauritius treaty. Also the gains are exempt u/s 10(23G) of the ITA. Perusal of SPA shows that AT&T Mauritius was the beneficial owner of shares. NCWS had become party to the SPA because it had provided certain warranties under the Agreement. • The shares were issued to AT&T Mauritius after obtaining RBI approval. As per Circular No. 682 & 789 AT&T Mauritius qualifies as the beneficial owner of shares of ICL . It is not open to the tax authorities to lift the corporate veil to find out who is the real owner of shares. • AB Nuvo had filed an application under Section 195 to make payment to AT&T Mauritius for purchase of shares of ICL claiming nil withholding on the basis of capital gains tax exemption under the India Mauritius tax treaty and nil withholding order was issued by the tax office against the above application. • AB Nuvo cannot be treated as agent of NCWS under Section 160 of the ITA. Once certificate was issued u/s 195, tax cannot be recovered from AB Nuvo as non-resident’s agent. T.P.Ostwal & Associates

High Court’s Observation & Ruling • NCWS offered to sell the shares of ICL to the Birla Group. If AT&T was the beneficial owner of shares, NCWS need not be a party to the SPA. As per the clauses in the JVA and the shareholders agreement, shares allotted to AT&T Mauritius could not be sold by it without the consent of NCWS. Hence the argument that NCWS was a party to the SPA only because of warranties cannot be accepted. • RBI approval does not make AT&T Mauritius the legal owner of the shares. • Circular 789 and 682 and Azadi Bachao Supreme Court decision has no relevance to the facts of the present case . The Circulars and decision apply where investments are made by Mauritius companies. Here, AT&T US subscribed and owned the shares of ICL . Hence, the investments in this case were made by AT&T US and not by any Mauritius company o Payment by / allotment to AT&T Mauritius does not mean that investments were made by AT&T Mauritius . • The argument that the JVA comes to an end on execution of the Shareholders Agreement is without merit. Shareholders Agreement seeks to supersede the terms of the JVA only to the extent they are in conflict with the Shareholders Agreement. T.P.Ostwal & Associates

Revenue’s Contentions High Court’s Observation & Ruling • AT&T Mauritius not the legal owner of shares because the allotment of shares to AT&T Mauritius was on behalf of AT&T US as per the JVA. Hence, AT&T USA was the legal owner of the shares of ICL sold under the SPA and capital gains prima facie accrued to AT&T US . Lifting of corporate veil of AT&T Mauritius not relevant as investment in shares was made by AT&T US. • Transfer of ICL shares constitutes transfer of a capital asset situated in India. Income from such transfer of capital asset would be deemed to accrue or arise in India. Under Section 9 r.w. Section 5 of the ITA. • Under Section 163 of the Act, a resident may be regarded as an agent of the non-resident if the resident has acquired by means of a transfer, a capital asset in India, from the non-resident. In the present case, AB Nuvo has acquired shares of ICL from AT&T US . Income can be assessed in the hands of AT&T US or in the hands of AB Nuvo as agent of AT&T US under Section 163 of the Act . • The fact that AB Nuvo was purchasing the shares under the right of first refusal option given by NCWS was suppressed by AB Nuvo in obtaining the withholding certificate. AB Nuvo further represented to the tax office that shares were allotted by ICL to AT&T Mauritius without any specific agreement relating to such allotment. T.P.Ostwal & Associates

High Court’s Observation & Ruling • The proceedings under Section 163 and 195 operate in different fields. Liability of an assessee under Section 195 in his capacity as a payer, whereas, the liability under Section 163 is as a representative assessee. Representative assessee cannot escape liability on the ground that the assessee as a payer was not required to withhold tax in terms of the withholding certificate. The withholding certificate obtained by AB Nuvo by furnishing incorrect facts / misleading statements would not preclude the Revenue from initiating proceedings under Section 163 of the Act. • Though Section 166 contemplates assessment either in the hands of the non-resident or in the hands of the representative assessee, the Section does not specify that once the assessment proceedings are initiated against the non-resident, representative assessee proceedings must be dropped. However where complex issues are involved and the AO is unable to make up his mind on account of suppression of material facts then it would be open to the AO to continue with the assessment against the representative assessee and the non-resident simultaneously till he decides to assess either of them. • The HC observed that in case of purchase of shares of AT&T Mauritius by TIL, it cannot be unaware of the fact that shares of ICL did not belong to AT&T Mauritius . Prima facie opinion of the Revenue that the transaction was a colourable device not devoid of merit. T.P.Ostwal & Associates

SANOFI – AAR RULING AAR No. 846 & 847 of 2009 T.P.Ostwal & Associates

Sanofi – AAR Ruling – AAR No. 846 & 847 of 2009 Indirect transfer of Indian Shares is taxable Murieux Alliance (‘MA’) France Groupe Industrial Marcel Dassault, (‘GIMD’) France Sanofi Pasteur Holding (‘Sanofi’) France Individual Transfer of shares of ShanH by MA and GIMD ShanH France ShanthaBiotechnics Ltd (‘Shantha’) India T.P.Ostwal & Associates

Facts • Groupe Industrial Marcel Dassault (“GIMD”) and Marieux Alliance (“MA”) (collectively referred to as “the applicants”) were tax residents of France holding a valid Tax Residency Certificate (“TRC”). MA formed a wholly owned subsidiary (“WOS”) in France, ‘ShanH’ and entered into a share purchase agreement for acquiring up to 80 percent equity shares of an Indian company, Shantha Biotechnics Ltd. (“Shantha”). Though the consideration and stamp duty were paid for by MA, the shares were acquired in the name of ShanH. • Thereafter, GIMD purchased 20 percent of the shares of ShanH from MA and subsequently, an individual purchased part of the shares of ShanH from MA and GIMD. Finally, the applicants sold their shares in ShanH to another French company, Sanofi Pasteur Holding (“Sanofi”). The applicants applied to the AAR seeking a ruling on the Indian tax implications arising from the sale of shares of ShanH to Sanofi. T.P.Ostwal & Associates

Issues before AAR • Whether capital gains arising from sale of shares of ShanH to Sanofiwould be chargeable to tax in India or France under the provisions of the DTAA between India and France? • If controlling interest in a company could be treated as a separate asset, whether gain from transferring such controlling interest could be taxed only in France as per Article 14(6) of the DTAA between India and France? T.P.Ostwal & Associates

Applicant’s Contentions • The transfer of shares of a ShanH to Sanofi is a transfer between two French companies, of shares in a French company and cannot be regarded as chargeable to tax in India as per Article 14 of the DTAA between India and France; • Setting up of a ShanH for acquisitions of Shantha was a legal, permissible and known method of transacting and there was nothing illegal in this step of holding the shares of Shantha through ShanH; • It must be understood based on the SC ruling in the ABA case that theRevenue cannot proceed on an inquiry of ascertaining the real nature of a transaction when the cases are governed by the provisions of the DTAA; • Since the applicants have undertaken the transaction in a legally permissible manner and since all the companies involved legally existed under the relevant laws of France and were tax residents of France, there was no scheme to avoid tax; and • In the absence of any specific provision under the Act, the taxing statute has to be construed strictly and cannot be interpreted to cover transactions through concepts of underlying assets and controlling interest. T.P.Ostwal & Associates

Revenue’s Contentions • ShanH was only a shell company without any office or employees or assets and merely held the investment in Shantha. ShanH was incorporated merely for dealing with the shares of Shantha and it was designed for avoidance of tax, which would have arisen on account of a direct transfer of shares of Shantha; • The applicants were virtually handing over the controlling interest in Shantha to Sanofi by sale of shares of ShanH. The transaction should be treated as a device for avoidance of tax in India and hence, the AAR should dismiss the application as not maintainable [the provisions related to Advance Rulings under the Income-Tax Act, 1961 (“the Act”) state that an application on a transaction that is prima facie designed for the avoidance of income-tax should not be considered by the AAR]; and • Section 9 of the Act and the DTAA permit a see-through provision to determine true purpose of a transaction. Hence, the AAR should hold that the transfer of shares of ShanH results in transfer of interest in Shantha, which would be taxable in India. T.P.Ostwal & Associates

AAR’s Ruling • The AAR has made a significant departure from the SC decision in ABA on the principles of tax avoidance by holding that: • The SC, in the case of McDowell and Co, held that colourable devices cannot be considered as part of tax planning and that such planning may be legitimate if it is within the framework of law. All the judges of the SC had accorded their approval for this view; • The SC in ABA seems to have proceeded on the basis that the above view was expressed by only one of the Judges and that it did not represent the view of the Court as a whole. This does not appear to be correct as elsewhere in the McDowell ruling, all the Judges have concurred with the above view; • If the purpose of a transaction was to create a legal smoke screen to avoid the payment of tax, which would legitimately arise, the legal effect of the transaction has to be considered in the context of the taxing statute; • The incidence of capital gains in India related to transfer of shares of Shantha could be perpetually avoided by transferring the shares of ShanH; • The series of transactions starting from the formation of ShanH to transfer of shares in ShanH appears to be a preordained to avoid dealing with the shares of Shantha, which would have created an incidence of tax in India; T.P.Ostwal & Associates

AAR’s Ruling • The word ‘alienation’ used in the Article 14.5 of the DTAA between India and France is of wide import and it includes within its ambit, transfer of the right of participation in an Indian company and therefore, the transfer of shares of ShanH should be regarded as taxable in India as per Article 14 of the DTAA; and • The transfer of shares of ShanH involves alienation of assets and controlling interest of an Indian company and consequently, the transactions should be regarded as part of scheme for avoidance of tax, which has to be ignored. Even then, it is not alienation of shares of an Indian company on a literal interpretation of Article 14(5) of the DTAA, but on a purposive interpretation of the Article and the gain arising from the transaction should be treated as chargeable to tax in India. T.P.Ostwal & Associates