Download

1 / 0

0 likes | 174 Views

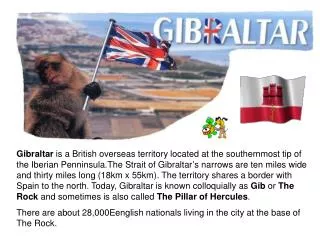

GIBRALTAR PHILANTHROPY FORUM. Tax and legal issues relating to international giving Owen clutton. 19 November 2013. Issues for international donors. Legal structure Flexibility Objectives Activities Taxation benefits for donors Taxation benefits for charities Monitoring use of funds.

E N D