Download

1 / 27

290 likes | 314 Views

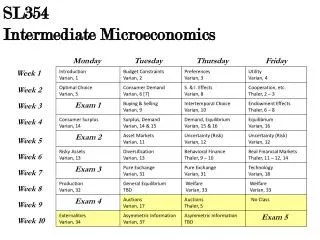

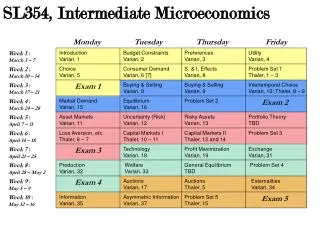

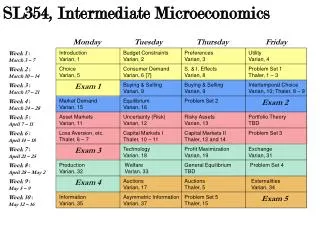

SL354, Intermediate Microeconomics. Monday. Tuesday. Thursday. Friday. Week 1 : March 3 – 7. Introduction Varian, 1. Budget Constraints Varian, 2. Preferences Varian, 3. Utility Varian, 4. Week 2 : March 10 – 14. Choice Varian, 5. Consumer Demand Varian, 6 [7].

E N D

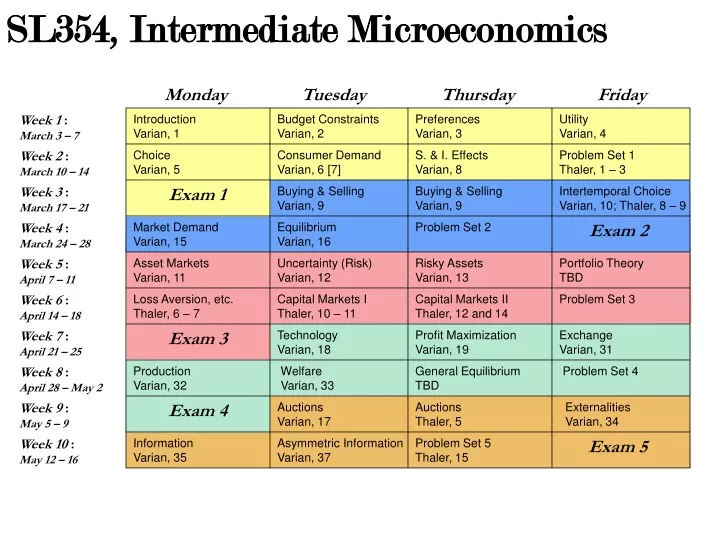

SL354, Intermediate Microeconomics Monday Tuesday Thursday Friday Week 1 : March 3 – 7 Introduction Varian, 1 Budget Constraints Varian, 2 Preferences Varian, 3 Utility Varian, 4 Week 2 : March 10 – 14 Choice Varian, 5 Consumer Demand Varian, 6 [7] S. & I. Effects Varian, 8 Problem Set 1 Thaler, 1 – 3 Week 3 : March 17 – 21 Exam 1 Buying & Selling Varian, 9 Buying & Selling Varian, 9 Intertemporal Choice Varian, 10; Thaler, 8 – 9 Week 4 : March 24 – 28 Market Demand Varian, 15 Equilibrium Varian, 16 Problem Set 2 Exam 2 Week 5 : April 7 – 11 Asset Markets Varian, 11 Uncertainty (Risk) Varian, 12 Risky Assets Varian, 13 Portfolio Theory TBD Week 6 : April 14 – 18 Loss Aversion, etc. Thaler, 6 – 7 Capital Markets I Thaler, 10 – 11 Capital Markets II Thaler, 12 and 14 Problem Set 3 Week 7 : April 21 – 25 Exam 3 Technology Varian, 18 Profit Maximization Varian, 19 Exchange Varian, 31 Week 8 : April 28 – May 2 Production Varian, 32 Welfare Varian, 33 General Equilibrium TBD Problem Set 4 Week 9 : May 5 – 9 Exam 4 Auctions Varian, 17 Auctions Thaler, 5 Externalities Varian, 34 Week 10 : May 12 – 16 Information Varian, 35 Asymmetric Information Varian, 37 Problem Set 5 Thaler, 15 Exam 5

Intertemporal Trades • • Borrowing in period 1

Intertemporal Trades Patient preferences (Negative time preference) Impatient preferences (Positive time preference)

Asset Markets: Equity GE Average 1982-2005 24% SP500 Average 1982-2005 12.3% *Calculated from a value-weighted index of all publicly traded stocks using CRSP data. *Calculated as compounded annual return on average monthly returns from preceding 12 months.

Present Valuation Techniques and Asset Valuation • The present value (PV) of an amount to be received at time t (FV) when the per-period discount rate is r: • The present value (PV) of a stream of future values, when the per-period discount rate is r: • Bond pricing. The price of a bond will be the net present value of interest payments and the maturity date and value. • Stock valuation. The current value of a firm (PVFirm) is the present value of the stream of future profits that the firm will generate -- and shareholders are “residual claimants” of those profits:

Optimal Holding Period for an Asset Rate of return from holding asset t*

Risk and Uncertainty: “Contingent Consumption Plans” Outcome A: If Pr(Lucky) = 0.025): Outcome B: Case 2: A person with an endowment of $35,000 faces a 1% probability of losing $10,000. He is considering the purchase of full insurance against the loss for $100. Case 1: A person with an endowment of $100 is considering the purchase of a lottery ticket that costs $5. The winning ticket in the lottery gets $200. $100 $35,000 Lucky day Do not purchase Do not purchase Unlucky day $25,000 Lucky day Lucky day $295 $34,900 Purchase Purchase Unlucky day Unlucky day $95 $34,900

Risk and Uncertainty: “Contingent Consumption Plans” $35,000 Lucky day Do not purchase Unlucky day $25,000 Lucky day $34,900 • Purchase Unlucky day $34,900 • K = the “expected loss” ($10,000), and gK is the insurance premium.

Economic Treatment of Risk The Meaning of Risk Aversion 1. Risk aversion is defined through peoples’ choices: 2. Non-linearity in the utility of wealth. Given a choice between two options with equal expected values and different standard deviations, a risk averse person will choose the option with the lower standard deviation: Given a choice between two options with equal standard deviations and different expected values, a risk-averse person will choose the option with the higher expected value:

Dealing With Risk: Insurance $100,000 Pr(xA) = .990 E[X] = $99,500 s = $4,975 cv = 0.0500 Pr(xB) = .010 $50,000

Dealing With Risk: Insurance $100,000 - $500 $99,500 Pr(xA) = .990 E[X] = $99,500 s = $0 cv = 0 $100,000 Pr(xB) = .010 • $100,000 • $500 • - $50,000 • + $50,000 • $99,500

Dealing With Risk: Insurance For a risk-averse person . . . Is Preferable to E[X] = $99,500 s = $0 cv = 0 E[X] = $99,500 s = $4,975 cv = 0.0500 Can we find another option, keeping s = $0, but with a lower E[X], that will be considered equal to the original? For example, suppose that for this risk-averse person . . . Is Equivalent to E[X] = $99,415 s = $0 cv = 0 E[X] = $99,500 s = $4,975 cv = 0.0500

Dealing With Risk: Insurance If, for a risk-averse person . . . Is Equivalent to E[X] = $99,500 s = $4,975 cv = 0.0500 $99,415 Then $99,415 is called a certainty equivalent. Furthermore, we will be able to sell an insurance policy to this person for $585. The $85 difference between the amount the person will pay and the expected loss is called a risk premium.

Economic Treatment of Risk Utility The Meaning of Risk Aversion A U($) U3 l U2 l l B D U1 l C Risk Premium $ $0 $99,415 $99,500 $100,000 $50,000

Economic Treatment of Risk Utility U($) Risk Aversion and Risk Neutrality U($) U($) Risk Aversion Risk Neutral Risk Seeking $

Economic Treatment of Risk Utility Risk Tolerance U1($) U2($) Risk Premium 1 Risk Premium 2 $ Risk Premium 1 > Risk Premium 2 : Agent 1 is more risk averse than Agent 2 Agent 2 is more risk tolerant than Agent 1

Modeling Risk and Expected Utility in Insurance Problems Expected Utility: Certainty Equivalent: Risk Premium:

Dealing With Risk: Diversification (Portfolio Theory) Expected Return of a Portfolio (2 investments): Expected Variance of a Portfolio (2 investments):

Dealing With Risk: Diversification (Portfolio Theory) Portfolio Example

Capital Asset Pricing Model Capital Market Line Security Market Line 1

Economic Analysis of Market Opportunities Efficient Markets and Economic Profits – Total Market Returns, Selected Time Periods

Loss Aversion “Most respondents in a sample of undergraduates refused to stake $10 on the toss of a coin if they stood to win less than $30.” Value = V($) + v - $10 + (Loss) + (Gain) + $30 - v You are offered the following bet: A coin will be tossed. If it is heads you win x; if it is tails, you lose y.