Download

1 / 28

290 likes | 429 Views

The European VAT System And The German Application. Andrea Gebauer German Federal Ministry of Finance. European Aspects. The European VAT Harmonization. First and Second Directive on turnover taxes ( April 1967): Europe-wide introduction of VAT with input tax deduction

E N D

The European VAT System AndThe German Application Andrea Gebauer German Federal Ministry of Finance EUROsociAL – Workshop Brasilia

European Aspects EUROsociAL – Workshop Brasilia

The European VAT Harmonization • First and Second Directive on turnover taxes (April 1967): • Europe-wide introduction of VAT with input tax deduction until 1th of January 1972 • Sixth Directive on the Harmonization of the Law of the Member States relating to turnover taxes (incl. several directives of amendment) (1977) • General conditions of the European VAT system EUROsociAL – Workshop Brasilia

The Sixth Directive I Regulations and definitions: • Scope • Territoriality • Taxable person • Taxable goods and services • Place of taxable transaction • Chargeable event and chargeability of tax • Basis of assessment • Tax rates, e.g. • Minimum normal rate 15% (since January 2001) • 1-2 reduced rates • minimum 5% • only special items (Annex H) • One tax rate for import and domestic transactions EUROsociAL – Workshop Brasilia

VAT Standard Rates in the European Union 2006 EUROsociAL – Workshop Brasilia

VAT Reduced Rates in the European Union 2006 EUROsociAL – Workshop Brasilia

The Sixth Directive II Regulations and definitions: • … • Tax rates • Tax exemptions • Deduction • Liability for payment of tax • Obligations for taxable persons • Special regulations, e.g. • Small traders regulations • Average rates for agriculture and forestry enterprises • Simplifications • Transitional arrangements EUROsociAL – Workshop Brasilia

The Sixth Directive III • Regulations and definitions: • … • Simplifications • Transitional arrangements • So-called transitional regime for turnover taxation in the European Community (1993) • Abolition of border controls for tax reasons within the EC • Introduction of a tax-free intra-Community supply of goods • Origin regime for tourist traffic • European decision mechanism EUROsociAL – Workshop Brasilia

Turnover Taxation in Germany- VAT System - EUROsociAL – Workshop Brasilia

German VAT System • VAT introduction: 1.1.1968 • VAT: common tax • Legislation: Federation • German legal base: • Turnover Tax Law (UStG) • Turnover Tax Implementing Order (UStDV) • Administration: Länder EUROsociAL – Workshop Brasilia

German VAT System • Legislation: Federation • German legal base • Administration: Länder • Design of the German VAT system: • 2 tax rates: • Standard rate • Reduced rate (in particular to food, printed matter and other cultural supply of goods or services for public benefit, certain health services and local public transport) EUROsociAL – Workshop Brasilia

Development of the German VAT Standard Rate and the Reduced Rate EUROsociAL – Workshop Brasilia

German VAT System • Legislation: Federation • German legal base: • Administration: Länder • Design of the German VAT system: • 2 tax rates: • Standard rate • Reduced rate (in particular to food, printed matter and other cultural supply of goods or services for public benefit, certain health services and local public transport) • Exempt transactions, e.g. • Exports and intra-Community supply of goods • Financial transactions • Renting and leasing • Treatments EUROsociAL – Workshop Brasilia

Design of The German VAT System • 2 tax rates • Exempt transactions • Tax payers: • Traders who carry out taxable transactions and make taxable acquisitions • Persons liable for customs duties (on imports) EUROsociAL – Workshop Brasilia

Design of The German VAT System • 2 tax rates • Tax payers • Tax payable on: • Supplies of goods and services made for consideration by a trader in Germany in the course of his business • Intra-Community acquisition made for consideration in Germany • Importation of goods into Germany EUROsociAL – Workshop Brasilia

Design of The German VAT System • 2 tax rates • Tax payers • Tax payable on: • Supplies of goods and services made for consideration by a trader in Germany in the course of his business • Intra-Community acquisition made for consideration in Germany • Importation of goods into Germany • Deduction of input tax EUROsociAL – Workshop Brasilia

Input Tax Deduction Requirements Requirements in principle: • A trader received • from another trader • a taxable supply of goods and services • for entrepreneurial purposes and • is endued with an invoice (§§ 14, 14a UStG) and • the tax payment is obligatory. EUROsociAL – Workshop Brasilia

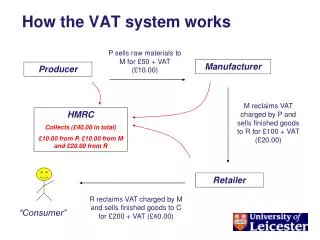

The German VAT System Company A Company B Company C Final consumption Purchase10.000 1.600 Purchase20.000 3.200 Buying30.000 4.800 Sale10.000 1.600 Sale20.000 3.200 Sale 30.000 4.800 Tax 1.600 -0 =1.600 Tax 4.800 -3.200 =1.600 Tax 3.200 -1.600 =1.600 • Tax charged at every stage of production and sale • Fractioned payment of VAT by companies in the company-chain • VAT and input tax are autonomous claims which arise in principle from service provision (so called Soll-Prinzip) EUROsociAL – Workshop Brasilia

Design of The German VAT System • 2 tax rates • Tax payers • Tax payable on: • Supplies of goods and services made for consideration by a trader in Germany in the course of his business • Intra-Community acquisition made for consideration in Germany • Importation of goods into Germany • Deduction of input tax • VAT declaration and Collection, Special Announcement Duties EUROsociAL – Workshop Brasilia

VAT Declaration And Collection, Special Announcement Duties • Declaration of VAT • Advance announcement (Umsatzsteuervoranmeldung) • VAT previous year > € 6.136: monthly announcement • € 512 < VAT previous year < 6.136 €: quarterly announcement • Startups: for 2 years monthly announcement • Annual tax declaration • VAT previous year < € 512: only annual tax declaration • Others: annual tax declaration in addition to advance announcements • Charge of VAT • Tax returns and advance payments on a monthly or quarterly basis • Annual final settlement • Summary Statementquarterly (yearly), e.g. • Intra-Community supply of goods • Triangulation EUROsociAL – Workshop Brasilia

Design of The German VAT System • … • Deduction of input tax • VAT declaration and Collection, Special Announcement Duties • Special Features EUROsociAL – Workshop Brasilia

Special Features • Small traders regulations • Average rates for agriculture and forestry enterprises • Liability • Tax audit • „Umsatzsteuernachschau“ • Umsatzsteuersonderprüfung, Betriebsprüfung EUROsociAL – Workshop Brasilia

Turnover Taxation in Germany- Fiscal Aspects - EUROsociAL – Workshop Brasilia

Development of Direct and Indirect Taxes as Share in German Tax Revenue EUROsociAL – Workshop Brasilia

Development of Excise Duties and VAT as Share in Revenue of Excise Taxes EUROsociAL – Workshop Brasilia

Development and Division of German Turnover Taxes VAT introduction 01.01.1968 EUROsociAL – Workshop Brasilia

Division of German Tax Revenue 2005 EUROsociAL – Workshop Brasilia

The End EUROsociAL – Workshop Brasilia